Welcome to the Frugal Hacker’s Guide to Side Hustle Taxes

Hey there, frugal friends! Let us talk about the one thing that makes every side hustler break out in a cold sweat: taxes. You have been working incredibly hard, clipping coupons, negotiating your internet bills, and hustling on the weekends to build that emergency fund. But if you do not understand how the IRS views your side income, you could end up handing a massive chunk of your hard-earned cash right back to the government. We are here to stop that from happening. Whether you are delivering groceries, selling vintage clothes online, or picking up freelance writing gigs, understanding the difference between W2 and 1099 income is the ultimate frugal hack. It is not just about legal compliance; it is about keeping more of your money in your pocket where it belongs. The gig economy is booming, and while making extra money is fantastic for your budget, the tax implications can be a nasty surprise if you are not prepared. Many first-time side hustlers experience the dreaded ‘tax time shock’ when they realize they owe thousands of dollars they did not save for. Let us break down the confusing tax jargon into plain, street-smart English so you can hustle smarter, not harder. By the end of this guide, you will know exactly how to legally minimize your tax burden and maximize your take-home pay.

The Hack: Decoding W2 vs 1099 Income

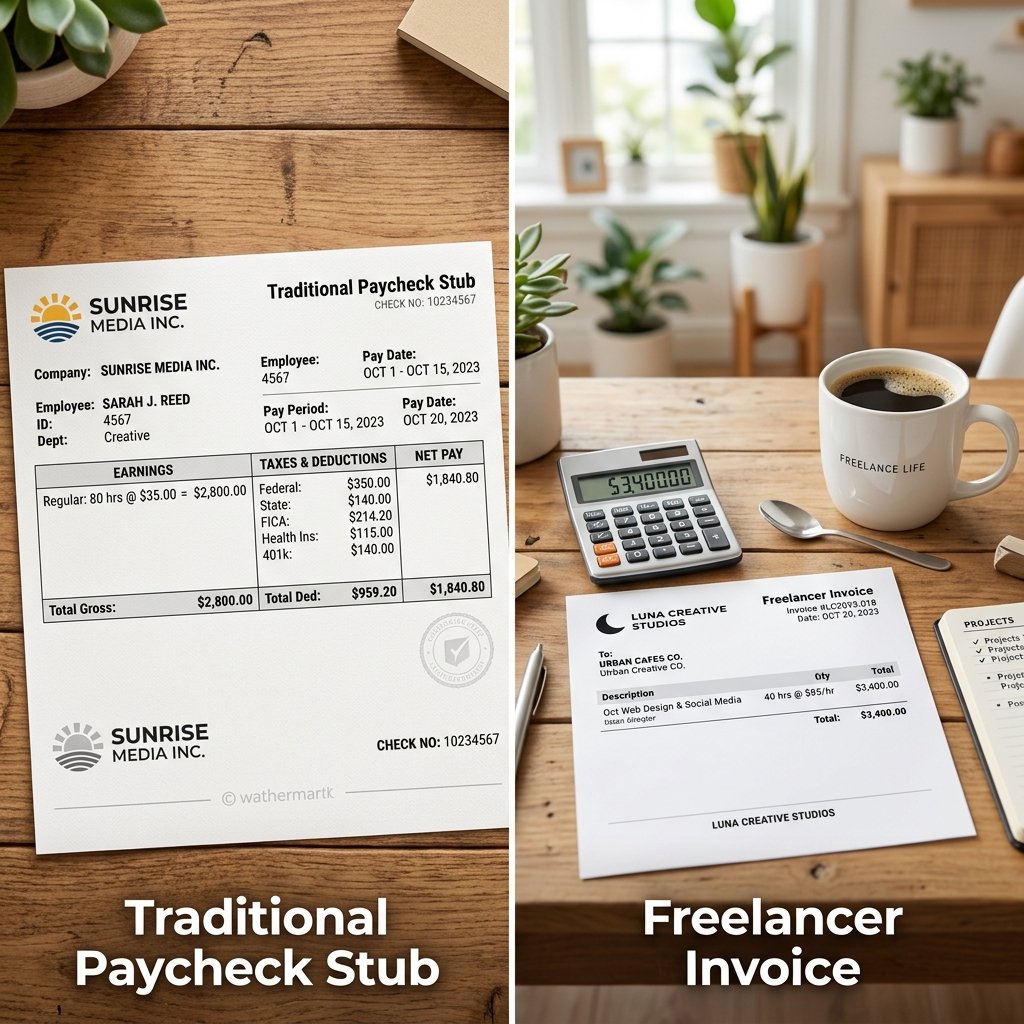

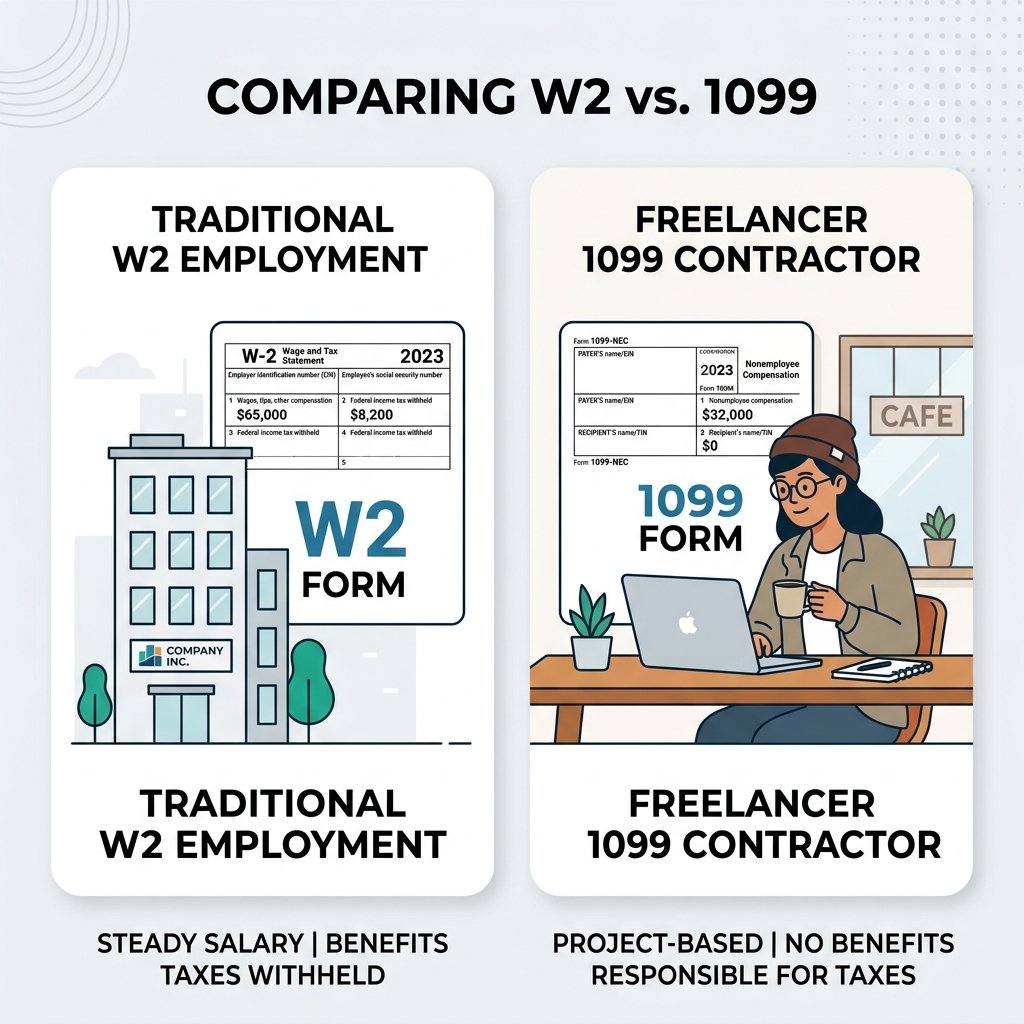

The first step to mastering your side hustle taxes is knowing your exact classification. When you get a side job, you are generally classified as either an employee (W2) or an independent contractor (1099). If you are a W2 employee, your employer takes taxes out of your paycheck before you even see the money. You fill out a W-4 form when you are hired, and it is relatively easy because the math is done for you. However, you have much less control over your work and your deductions. If you are a 1099 contractor—like an Uber driver, a freelance graphic designer, or a dog walker on Rover—you get the full amount of your earnings paid upfront. You fill out a W-9 form to start. Sounds great to get all that cash at once, right? But wait! You are now responsible for paying your own taxes later. You are essentially running your own mini-business. Here is the ultimate breakdown of what that means for your daily hustle.

| Feature | W2 Employee | 1099 Contractor |

|---|---|---|

| Tax Withholding | Taxes taken out automatically by employer | You must save and pay taxes yourself |

| Self-Employment Tax | Employer pays half, you pay half (7.65%) | You pay the full 15.3% yourself |

| Work Control | Employer sets your hours, tools, and rules | You are your own boss, set your own hours |

| Tax Write-Offs | Very limited, standard deduction mostly | You can deduct business expenses to save money! |

As a 1099 worker, you have the incredible power to lower your tax bill by claiming expenses, which is a massive win for the frugal hacker. But with great power comes great responsibility. You must track everything.

The Math: What Does This Mean for Your Wallet?

Realistic Earning Potential and Tax Realities

Let us look at the real numbers, because frugal living is all about the math. If you make $10,000 a year from your side hustle, how much do you actually get to keep? As a 1099 contractor, you have to worry about standard income tax PLUS self-employment tax (which covers your Medicare and Social Security contributions). The self-employment tax rate is a flat 15.3%. This is on top of whatever your normal income tax bracket dictates. Here is a realistic budget breakdown of what happens to $1,000 of side hustle income, assuming you are in a standard 22% income tax bracket.

| Income Source | Gross Pay | Estimated Taxes Owed | Net Take-Home Pay |

|---|---|---|---|

| W2 Side Job | $1,000 | $296 (withheld automatically) | $704 |

| 1099 Side Hustle (No Deductions) | $1,000 | $153 (SE Tax) + $220 (Income Tax) = $373 | Roughly $627 (paid later) |

| 1099 Hustle (With Frugal Hacks) | $1,000 | Lowered by maximizing deductions (e.g., taxes on only $600) | $776+ |

Notice that third row? That is exactly where we want you to be. By meticulously tracking your expenses, you lower your taxable income, meaning you pay taxes on a much smaller number. If you spend $400 on necessary supplies for your hustle, you only pay taxes on $600, not the full $1,000. That is how you save hundreds, if not thousands, of dollars a year! It is the ultimate frugal hack for gig workers.

The Action Plan: Maximizing Your Frugal Write-Offs

The Best Deductions for Side Hustlers

Do not leave your hard-earned money on the table! The IRS legally allows independent contractors to write off ordinary and necessary business expenses. You do not need fancy, expensive software to track this. A simple spreadsheet or a free budgeting app will do the trick perfectly. Here are some of the most common write-offs you should be tracking to lower your tax bill:

- Mileage: If you drive for DoorDash, Instacart, or drive to meet freelance clients, track your miles! The IRS gives you a standard mileage rate (around $0.67 per mile). This adds up incredibly fast.

- Home Office: If you use a dedicated space in your home exclusively for your side hustle, you can deduct a portion of your rent, mortgage interest, and utilities. The simplified method allows you to deduct $5 per square foot of your home office, up to 300 square feet (that is a $1,500 deduction!).

- Supplies and Equipment: Did you buy a $500 laptop specifically for your graphic design gig? Write it off! Did you buy insulated bags for food delivery? Write them off!

- Internet and Phone: Deduct the exact percentage of your monthly phone and internet bills that are used for your business operations.

- Education and Courses: If you paid for an online course to improve your side hustle skills, that is a deductible business expense.

The Golden Rule of Saving for Taxes

When you get paid as a 1099 contractor, the money hitting your bank account is not entirely yours. You need a rock-solid system to ensure you are not scrambling in April when the tax bill comes due.

The Frugal Hacker’s Tax Rule: Every single time you get paid from a 1099 side hustle, immediately transfer 25% to 30% of that gross paycheck into a separate, high-yield savings account. Do not touch it. Let it earn interest until tax time!

By putting that tax money into a high-yield savings account (HYSA), you are actually making a little bit of extra passive income on the money you eventually owe the IRS. If you save $3,000 for taxes in an account earning 5% APY, you will make a free $150 just for holding onto it. Now that is a brilliant frugal win!

The Strategy: Mastering Quarterly Estimated Taxes

Stop Waiting Until April to Pay

Here is a secret that trips up many new side hustlers: the United States tax system is ‘pay-as-you-go.’ If you are a W2 employee, your employer handles this by taking taxes out of every paycheck. But if you are a 1099 contractor and you expect to owe more than $1,000 in taxes for the year, the IRS requires you to make quarterly estimated tax payments. If you wait until April 15th to pay your entire bill, you could be hit with underpayment penalties and interest fees. Frugal hackers do not pay unnecessary fees!

When Are Quarterly Taxes Due?

- Q1: April 15th (for income earned Jan 1 – Mar 31)

- Q2: June 15th (for income earned Apr 1 – May 31)

- Q3: September 15th (for income earned Jun 1 – Aug 31)

- Q4: January 15th of the following year (for income earned Sep 1 – Dec 31)

Making these payments is easier than it sounds. You can use the IRS Direct Pay website to send in the money you have been diligently saving in your high-yield savings account. Think of it as paying a quarterly subscription fee to keep your business running smoothly without government penalties.

Scam Warning: Avoid Shady Tax Advice

Protecting Your Hard-Earned Side Hustle Cash

When you start making money and looking for clever tax loopholes, the scammers and bad advisors will come out of the woodwork. You will see viral videos on social media promising to erase your tax debt, or influencers claiming you can write off your family dog as a ‘business security system’ or your luxury car as a total deduction. Do not fall for it. Frugal living is about being smart, legal, and strategic, not reckless and fraudulent.

Scam Warning: Beware of ‘ghost preparers’ and viral tax hacks! Ghost preparers are unlicensed tax preparers who promise massive refunds, charge you a hefty fee (often a percentage of your refund), and refuse to sign the tax return as the preparer. If the IRS audits you, the ghost preparer disappears, and you are entirely on the hook for the penalties, back taxes, and potential legal trouble.

Always use reputable, free, or low-cost tax filing software. If your side hustle is simple, you might even qualify for the IRS Free File program, which costs absolutely nothing. Do not pay $300 to a sketchy strip-mall pop-up shop when you can file for free, or use a certified CPA if your business is genuinely complex. Trusting TikTok for tax advice is a quick way to lose all the money you worked so hard to save.

Conclusion

Wrapping Up Your Tax Strategy

Dealing with taxes does not have to be a terrifying experience that ruins the joy of making extra money. By understanding the fundamental differences between W2 and 1099 income, meticulously tracking your deductible expenses, and setting aside a percentage of your earnings into a high-yield savings account, you are taking full control of your financial destiny. You are not just a side hustler anymore; you are a savvy, strategic business owner. The frugal living journey is all about optimization, and mastering your taxes is one of the highest-ROI skills you can develop. Keep grinding, keep saving those receipts, and keep hacking your way to financial freedom! You have got this.

Disclaimer: I am the Ultimate Frugal Hacker, a content creator and personal finance enthusiast, not a certified financial advisor, CPA, or tax attorney. This article is for educational and entertainment purposes only. Tax laws change frequently and vary by location. Always consult with a licensed tax professional or CPA regarding your specific financial situation before making any major tax decisions.

Makenzie is the founder and lead writer at MoneyHackTips.com — a personal finance blog dedicated to delivering street-smart financial wisdom for real people on real budgets. With 300+ published articles covering everything from debt management to investing fundamentals, Makenzie’s mission is to make every dollar work harder. When not writing about money hacks, Makenzie is testing frugal living strategies, optimizing side hustles, and helping readers build financial freedom from scratch.