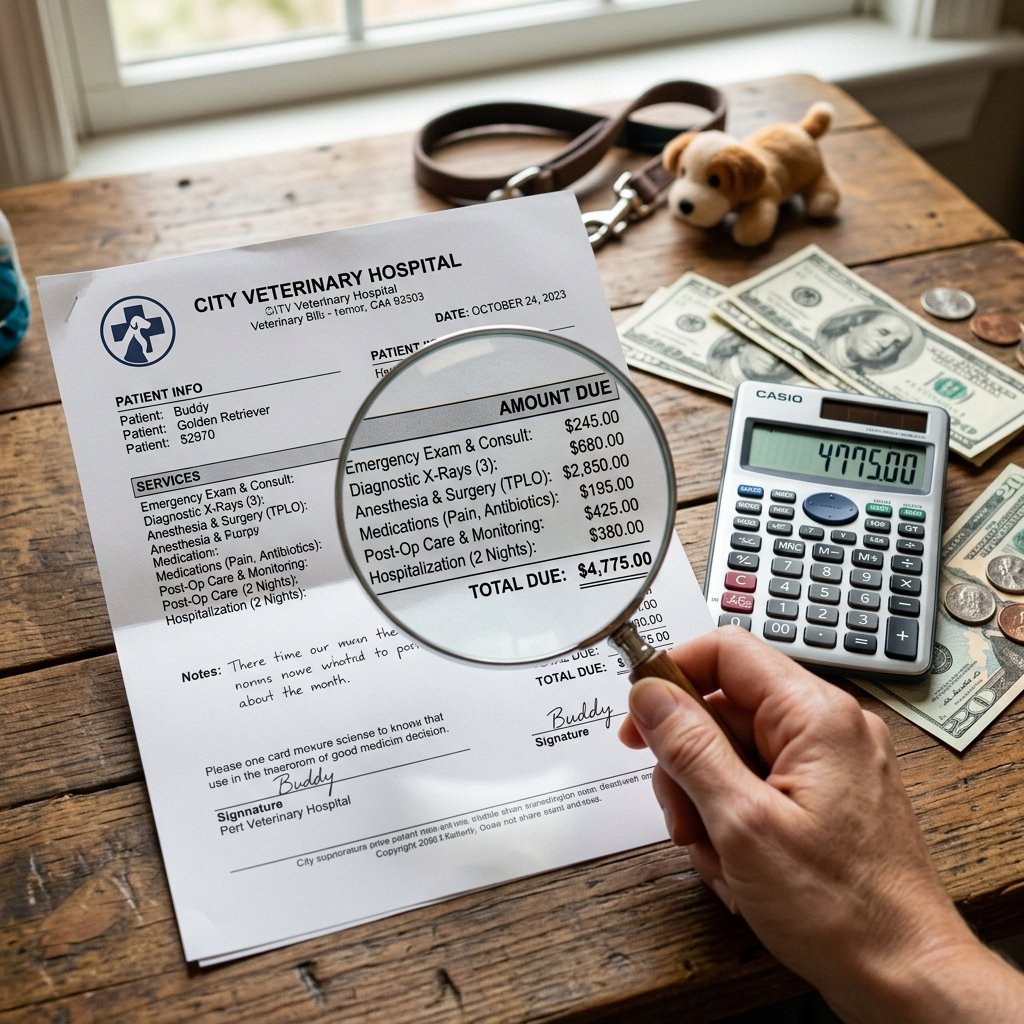

Welcome to the frugal family! If you are reading this, you probably love two things: your furry best friend and keeping your hard-earned money in your wallet. We all adore our pets, but let us talk about the elephant in the room: those terrifying, budget-busting vet bills. You are doing everything right, sticking to your budget, meal prepping, and clipping coupons, when suddenly your dog decides to eat a rogue sock. Next thing you know, you are staring at a vet bill for $3,000. Talk about a financial nightmare!

As frugal living enthusiasts, we are naturally skeptical of adding another monthly subscription or insurance premium to our expenses. Is pet insurance actually a smart financial safety net, or is it just another clever way for corporations to drain your emergency fund? Today, your Ultimate Frugal Hacker is going to break down the math, expose the hidden traps, and help you decide if pet insurance is truly worth it for your situation. Grab a cup of coffee, snuggle up with your pet, and let us dive into the ultimate beginner’s guide to stopping vet bill shock once and for all.

The Math: What Does A Vet Emergency Actually Cost?

As a frugal hacker, you know that the best way to beat an unexpected expense is to anticipate it. You cannot make an informed decision about insurance without knowing the actual financial risk you are facing. Routine care like vaccines and wellness exams are easy to budget for, but emergencies are where the real financial shock happens. Let us look at the cold, hard numbers of what a pet emergency can actually cost you in today’s economy.

| Common Pet Emergency | Estimated Vet Cost |

|---|---|

| Swallowed Foreign Object (Surgery) | $1,500 to $3,000 |

| Torn ACL (Cruciate Ligament Surgery) | $3,000 to $7,000 |

| Cancer Diagnosis and Treatment | $5,000 to $10,000+ |

| Severe Gastrointestinal Issues | $800 to $1,500 |

When you look at those numbers, it is easy to see how a single accident can wipe out months of careful saving. If you do not have at least $5,000 sitting in a dedicated pet emergency fund right now, an unexpected trip to the emergency vet could force you into high-interest credit card debt. That is exactly the scenario we want to avoid.

How Pet Insurance Works (Without The Jargon)

Insurance companies love to use confusing language to make things seem more complicated than they are. Let us strip away the jargon and look at how pet insurance actually functions. Unlike human health insurance, pet insurance does not usually have a network of approved doctors. You can go to any licensed veterinarian, which is a huge plus. However, the payment process is entirely different.

Key Rule: Pet insurance is almost always a reimbursement model. This means you MUST pay the vet upfront out of your own pocket, file a claim with your provider, and then wait for the insurance company to send you a check or direct deposit to pay you back.

Here are the three main terms you need to understand to hack the system:

- The Premium: This is the amount you pay every month just to have the policy. For dogs, this averages around $40 to $60 per month, and for cats, it is usually $20 to $30.

- The Deductible: This is the amount you must pay out of pocket before the insurance kicks in. A common deductible is $250 or $500 annually.

- The Reimbursement Rate: Once you hit your deductible, the insurance company pays a percentage of the remaining bill. Most frugal hackers opt for an 80% or 90% reimbursement rate to balance a lower monthly premium with high emergency coverage.

Cost Comparison: Paying Out of Pocket vs. Insurance

Let us get to the fun part: the math! To figure out if pet insurance is worth it, we need to compare a real-world scenario over a five-year period. Let us imagine you have a mischievous Labrador named Buster. You pay a premium of $50 a month (which equals $600 a year). Your policy has a $500 annual deductible and a 90% reimbursement rate. In year three, Buster swallows a tennis ball, resulting in a $4,000 emergency surgery.

| Expense Category | Without Insurance (Out of Pocket) | With Pet Insurance |

|---|---|---|

| 5 Years of Premiums | $0 | $3,000 |

| Emergency Vet Bill | $4,000 | $4,000 (Paid upfront) |

| Minus Deductible | Not Applicable | You pay the first $500 |

| Insurance Reimbursement (90%) | $0 | Insurance pays back $3,150 |

| Total Cost Over 5 Years | $4,000 | $3,850 (Premiums + Deductible + 10% Copay) |

In this specific scenario, having insurance saved you $150 over five years. However, if Buster never had an emergency, you would be down $3,000 in premiums. This highlights the ultimate truth of insurance: you are paying for peace of mind and protection against catastrophic, worst-case scenarios, not necessarily trying to make a profit.

The Frugal Hacker’s Checklist: When Is It Actually Worth It?

So, should you pull the trigger and buy a policy? As a frugal living enthusiast, your decision should be based on logic, not fear. Here is my street-smart checklist to help you decide if pet insurance is the right move for your household budget.

- Age of Your Pet: Insuring a puppy or kitten is usually the smartest move. Premiums are incredibly low, and they have no pre-existing conditions. If you try to insure a 10-year-old dog, your premiums might be over $100 a month, which rarely makes financial sense.

- Breed Risks: Do your research! If you own a French Bulldog or a Great Dane, they are genetically predisposed to incredibly expensive health issues. Insurance is highly recommended. If you have a mixed-breed mutt, they are generally healthier, and you might be better off self-insuring.

- Your Emergency Fund: Be honest with yourself. Do you have $5,000 in liquid cash ready to go? If yes, you might prefer to self-insure. If a $2,000 bill would force you to take out a payday loan, you need insurance immediately.

Red Flags and Scams to Avoid

The insurance industry is notorious for hidden clauses, and pet insurance is no exception. If you decide to buy a policy, you need to be fiercely protective of your money and read the fine print. Many beginners get burned because they assume everything is covered. Let me save you from a massive headache.

Scam Warning: Watch out for policies that cap payouts per incident or have hidden sub-limits for specific illnesses! For example, they might cover a $5,000 surgery but cap the payout for anesthesia at $200, leaving you holding the bag for the rest.

Furthermore, absolutely NO pet insurance covers pre-existing conditions. If your dog is already limping before you buy the policy, they will never cover that leg. Also, beware of the bilateral condition clause. If your dog tears a ligament in their left knee before you are insured, and then tears the right knee a year later, many companies will deny the second claim, arguing it is related to the first. Always demand a sample policy document before handing over your credit card!

Top Frugal Alternatives & Hacks to Lower Vet Bills

What if you run the numbers and decide traditional pet insurance is not for you? Do not worry, the Frugal Hacker has your back. There are plenty of brilliant, budget-friendly alternatives to keep your pet healthy without going broke.

- The Sinking Fund Strategy: Instead of paying a $50 premium to a corporation, set up an automatic transfer of $50 every month into a high-yield savings account dubbed the Pet Fund. If your pet stays healthy, you keep the cash!

- Discount Programs: Look into programs like Pet Assure. It is not insurance; it is a discount plan. You pay a small fee of around $10 a month, and participating vets give you an instant 25% discount on all in-house medical services, regardless of pre-existing conditions.

- Human Pharmacies for Pet Meds: Never buy common medications directly from the vet if you can avoid it. Ask for a written prescription and take it to your local pharmacy. Use apps like GoodRx to find massive discounts. You can often save up to 80% on antibiotics or anxiety meds!

- CareCredit: If you face an emergency without insurance, ask if your vet accepts CareCredit. It is a healthcare credit card that often offers 0% interest for 6 to 18 months, giving you time to hustle and pay off the bill without drowning in interest.

Script: When facing a high bill, say: I want to provide the best care, but I am working with a strict budget of [Insert Amount]. Are there alternative, more affordable treatment plans we can explore, or can we prioritize the most critical tests first?

Conclusion

At the end of the day, deciding whether to get pet insurance comes down to your personal risk tolerance and your current financial cushion. If you are just starting your frugal journey and have zero savings, pet insurance is a fantastic shield to protect you from sudden, crippling debt. However, if you are a seasoned saver with a robust emergency fund, building your own pet sinking fund might be the ultimate frugal hack. Whatever you choose, take action today. Start saving, start comparing quotes, and ensure your furry friend is protected.

Disclaimer: I am a frugal living enthusiast and content creator, not a licensed financial advisor, veterinarian, or insurance broker. This article is for informational and educational purposes only. Always do your own research, read the fine print, and consult with professionals before purchasing an insurance policy or making significant financial decisions.

Makenzie is the founder and lead writer at MoneyHackTips.com — a personal finance blog dedicated to delivering street-smart financial wisdom for real people on real budgets. With 300+ published articles covering everything from debt management to investing fundamentals, Makenzie’s mission is to make every dollar work harder. When not writing about money hacks, Makenzie is testing frugal living strategies, optimizing side hustles, and helping readers build financial freedom from scratch.