Hey there, frugal hackers! Let us talk about a topic that usually makes people want to run for the hills: estate planning. I know exactly what you are thinking. ‘Do you need a will? I am a broke millennial! My net worth consists of a 2012 Honda Civic, a half-eaten box of pizza, and a thriving collection of house plants.’ It sounds like something only billionaires with trust funds and yachts need to worry about, right? Wrong. Welcome to the ultimate broke millennial’s guide to estate planning. The truth is, having a will is not about how much money you have in the bank; it is about taking control, protecting your loved ones, and making sure the state does not get to decide what happens to your hard-earned stuff. Even if you are meticulously budgeting just to save $50 a week, you have an estate. Yes, you! Your bank accounts, your digital footprint, your beloved pets, and even your social media accounts all make up your estate. And if you kick the bucket without a plan, things get messy, expensive, and stressful for the people you leave behind. Today, we are going to break down exactly why you need a will, how to get it done without spending a fortune, and the street-smart strategies to hack your way to peace of mind. Grab a cup of your favorite homemade coffee, and let us dive into the ultimate strategy guide for frugal estate planning!

The ‘I Am Too Broke for a Will’ Myth

Let us bust the biggest myth right out of the gate: you do not need to be rich to need a will. In the legal world, dying without a will is called dying ‘intestate.’ When that happens, the laws of your state completely take over. They will appoint an administrator, dig through your finances, and distribute your assets based on a rigid legal formula. Spoiler alert: the state does not care that you promised your vintage record collection to your best friend or that you want your sister to take care of your dog. They just follow the flowchart.

What Exactly Is an Estate?

If you are breathing and own literally anything, you have an estate. Here is what is included in a typical broke millennial estate:

- Your Bank Accounts: Checking, savings, and that random high-yield savings account where you stash $20 a month.

- Digital Assets: Your cryptocurrency, your PayPal balance, and even your social media accounts.

- Vehicles: That reliable 2012 Honda Civic is a major asset!

- Personal Property: Your laptop, gaming console, jewelry, and yes, your houseplants.

- Pets: In the eyes of the law, pets are considered property. A will ensures they go to a loving home, not a shelter.

By spending just a little bit of time now, you can save your family a massive headache and thousands of dollars in probate court fees later. It is the ultimate frugal move: investing a tiny amount of effort today to prevent a massive financial drain tomorrow.

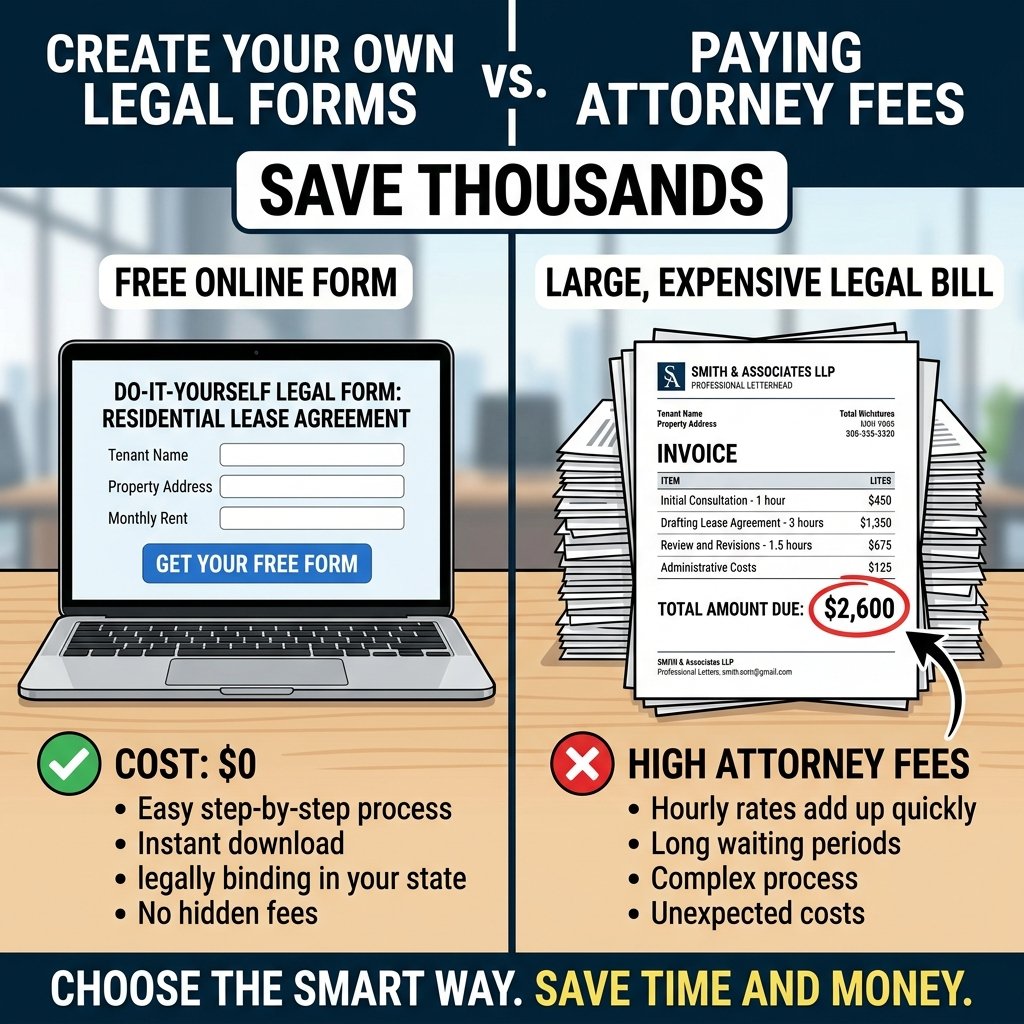

Cost Breakdown: DIY vs. Lawyer

Now, let us talk numbers. As frugal living enthusiasts, we do not want to spend $1,500 on a lawyer if we do not have to. The good news? You probably do not have to! If your financial situation is relatively simple—meaning you do not own multiple properties, have a complex business structure, or possess a multi-million dollar portfolio—you can absolutely hack this process for cheap or even free. Let us look at the math.

| Method | Estimated Cost | Best For |

|---|---|---|

| 100% Free Online Tools (e.g., FreeWill) | $0 | Simple estates, single folks, basic asset distribution |

| Budget Legal Services (e.g., LegalZoom, Trust & Will) | $89 – $159 | Those who want basic templates with a bit more customization |

| Traditional Estate Attorney | $1,000 – $3,000+ | High net worth, complex family dynamics, business owners |

Look at those savings! By choosing a free or low-cost online tool, you are keeping at least $1,000 in your pocket. That is money you could be investing, using to pay off student loans, or adding to your emergency fund. The internet has democratized legal documents, and as a street-smart millennial, you should absolutely take advantage of it.

The Holy Trinity of Estate Planning

A will is just one piece of the puzzle. To truly protect yourself and be a master of adulting, you need the ‘Holy Trinity’ of estate planning documents. Do not worry, you can usually get all of these done at the same time using the frugal tools we just discussed.

1. The Last Will and Testament

This is the big one. It dictates who gets your stuff, who takes care of your pets, and who is in charge of carrying out your wishes (your executor). Choose an executor who is responsible, organized, and will not crumble under pressure.

2. Advance Healthcare Directive (Living Will)

If you are in an accident and cannot make medical decisions for yourself, this document speaks for you. It outlines your preferences for life support, organ donation, and other critical medical interventions. It takes the emotional burden off your family so they do not have to guess what you would have wanted.

3. Durable Power of Attorney

This gives someone you trust the legal authority to handle your finances if you are incapacitated. Imagine being in a coma and no one can access your checking account to pay your rent or keep your car from being repossessed. A Power of Attorney ensures your bills get paid and your finances do not fall apart while you are recovering.

How to Start: Your Frugal Action Plan

Ready to get this done? Here is your step-by-step frugal tutorial to creating your estate plan without spending a dime.

- Take Inventory: Sit down with a notebook and list everything you own. Bank accounts, retirement accounts (like your 401k or Roth IRA), physical items of value, and digital assets.

- Choose Your People: Decide who will be your executor, who will get your assets (your beneficiaries), and who will take your pets. Pro Tip: Always have a backup person for each role just in case!

- Use a Free Platform: Head over to a reputable free site like FreeWill.com. They partner with nonprofits and allow you to generate legally binding wills for exactly $0. It takes about 20 minutes.

- Print and Sign: A will is not valid just because it is on your computer. You must print a physical copy.

- Get It Witnessed and Notarized: This is crucial! Most states require two witnesses who are NOT in the will to watch you sign it. To make it ‘self-proving’ (which speeds up the legal process later), get it notarized. Frugal Hack: Many local banks or credit unions offer free notary services to their account holders!

- Store It Safely: Keep the original in a fireproof safe or a safe deposit box, and tell your executor exactly where it is.

By following these steps, you are taking complete control of your financial legacy for literally zero dollars. That is the ultimate frugal win!

Scam Warnings and Key Rules

As the Ultimate Frugal Hacker, it is my duty to keep you safe from predatory practices. The legal and financial industries are full of traps designed to separate you from your hard-earned cash.

Scam Warning: Do not fall for ‘free’ will kits advertised on sketchy websites that require your credit card information just to download the final PDF. If they ask for your card details for a ‘free trial’ to access your document, run! Stick to verified platforms like FreeWill or use highly rated, transparently priced services like Trust & Will.

Also, beware of predatory lawyers who try to convince you that your simple checking account and used car require a complex, expensive trust. Trusts are fantastic tools for the wealthy or those with property, but they are usually overkill for a broke millennial.

The ‘Payable on Death’ Hack

Here is a massive frugal secret: you can bypass the will and probate process entirely for your bank accounts! Go to your bank and ask to set up a ‘Payable on Death’ (POD) or ‘Transfer on Death’ (TOD) beneficiary.

Script: ‘Hi, I would like to add a Payable on Death beneficiary to my checking and savings accounts. Can you provide me with the necessary forms?’

When you pass away, that money goes instantly to the person you named, completely bypassing the court system. It is fast, it is free, and it is incredibly efficient.

Conclusion

Wrap Up and Next Steps

So, do you need a will? Absolutely. Being a broke millennial is not an excuse to leave your digital and physical life in chaos. Estate planning is one of the most responsible, empowering, and surprisingly frugal things you can do for yourself and your loved ones. By utilizing free online tools, leveraging Payable on Death accounts, and understanding exactly what your estate entails, you are protecting your assets without blowing your budget. You just saved yourself over $1,000 in legal fees and secured your legacy. Now that is what I call a massive frugal victory! Get out there, take 20 minutes this weekend, and get your documents in order. You will sleep so much better knowing it is handled.

Disclaimer: I am the Ultimate Frugal Hacker, not a licensed attorney, financial advisor, or tax professional. This article is for informational and educational purposes only and does not constitute legal or financial advice. Laws vary by state, so if your situation is complex, please consult with a certified professional!

Makenzie is the founder and lead writer at MoneyHackTips.com — a personal finance blog dedicated to delivering street-smart financial wisdom for real people on real budgets. With 300+ published articles covering everything from debt management to investing fundamentals, Makenzie’s mission is to make every dollar work harder. When not writing about money hacks, Makenzie is testing frugal living strategies, optimizing side hustles, and helping readers build financial freedom from scratch.