Hey there, fellow frugal hackers! Welcome back to another deep dive into keeping your hard-earned money exactly where it belongs: in your own pocket. Today, we are tackling a massive financial trap that catches way too many smart, budget-conscious people off guard. We are talking about life insurance. More specifically, we are looking at the age-old debate of Term vs Whole Life Insurance. If you want to stop wasting money on policies you absolutely do not need, you have come to the right place.

As someone who loves living frugally, you already know the thrill of finding a great deal, negotiating a bill, or DIY-ing your way to savings. But when it comes to life insurance, the industry is designed to be confusing. It is packed with jargon, pushy salespeople, and complex charts that make it seem like you need to spend hundreds of dollars a month just to protect your family. Let me tell you a secret: you do not. In fact, falling for the whole life insurance pitch is one of the quickest ways to drain your monthly budget and sabotage your long-term wealth.

In this comprehensive guide, we are going to strip away the industry nonsense. We will look at the cold, hard math of why term life insurance is the ultimate frugal choice, how whole life policies are often just expensive illusions, and the exact strategies you can use to protect your loved ones while building serious wealth. Grab a cup of your favorite home-brewed coffee, pull up a chair, and let us start hacking your financial future!

The Basics: Decoding the Insurance Jargon (No Fluff Allowed)

Before we can start slashing your monthly budget, we need to understand exactly what we are dealing with. The insurance industry loves to use confusing terms to make you feel like you need their expensive expertise. Let us break it down into plain English.

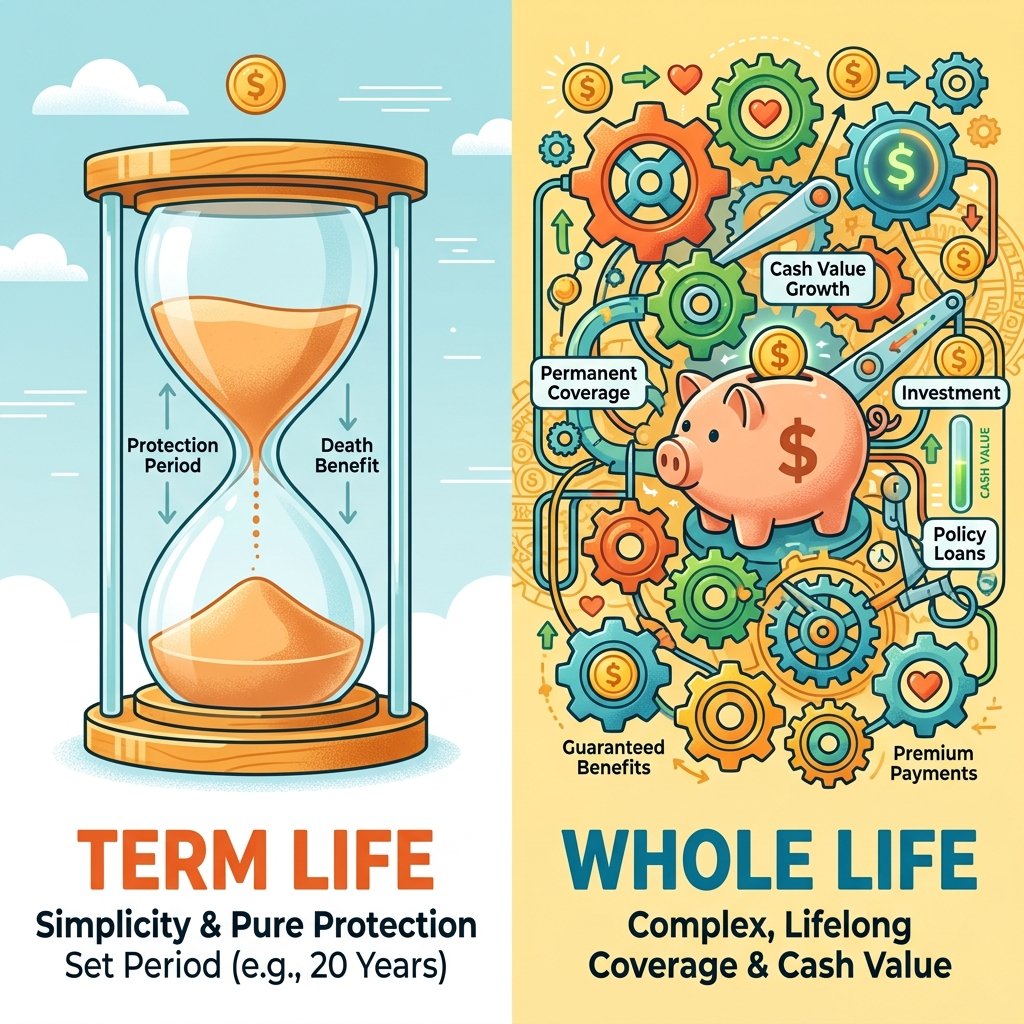

What is Term Life Insurance?

Think of term life insurance exactly like renting an apartment. You pay a set amount of money every month for a specific period of time—the term. This is usually 10, 20, or 30 years. If the worst happens and you pass away during that term, your family gets a massive, tax-free payout (the death benefit). If you outlive the term, the policy simply ends. You do not get your money back, but you also did not pay a fortune for the coverage. It is pure, straightforward protection. No bells, no whistles, no hidden fees.

What is Whole Life Insurance?

Now, imagine buying a house, but the mortgage comes with an incredibly complex, high-fee savings account attached to it, and the bank gets to keep a huge chunk of your money for the first few years. That is whole life insurance. It is designed to cover you for your entire life, not just a set term. A portion of your premium goes toward the actual insurance, and another portion goes into a cash value account that grows very slowly over time.

Key Rule: Insurance is meant to replace your income and protect your dependents if you die prematurely. It is NOT supposed to be a primary investment vehicle. Keep your insurance and your investments completely separate!

The problem with whole life is that because it guarantees a payout eventually, and because it includes this clunky savings component, the premiums are astronomically high. For a frugal living enthusiast, locking yourself into a massive monthly payment for a whole life policy is the opposite of financial freedom.

The Math: Why Whole Life is a Frugal Nightmare

You know I love to run the numbers. As frugal hackers, we do not make decisions based on emotions or fancy sales brochures; we make decisions based on math. Let us look at a realistic cost comparison between a 20-year term policy and a whole life policy for a healthy 30-year-old looking for $500,000 in coverage.

Cost Comparison: Term vs Whole Life

| Metric | Term Life (20-Year) | Whole Life |

|---|---|---|

| Coverage Amount | $500,000 | $500,000 |

| Average Monthly Premium | $30 | $300 to $500 |

| Annual Cost | $360 | $3,600 to $6,000 |

| Total Cost Over 20 Years | $7,200 | $72,000 to $120,000 |

Look at that massive gap! By choosing whole life, you are paying roughly ten times more for the exact same death benefit. That is an extra $270 to $470 leaving your bank account every single month. For someone trying to live frugally, pay off debt, or save for early retirement, that is a devastating leak in your budget.

Insurance agents will argue that the extra money is going into your cash value, which you can borrow against later. But here is the dirty little secret: the rate of return on that cash value is usually terrible (often barely beating inflation), and if you die, the insurance company keeps the cash value! Your family only gets the $500,000 death benefit. You literally lose the savings portion that you overpaid for.

The Strategy: Buy Term and Invest the Difference

So, what is the ultimate frugal hack here? It is a classic, battle-tested financial strategy called Buy Term and Invest the Difference (BTID). This is how you beat the insurance companies at their own game and build massive wealth for your family.

How the BTID Strategy Works

- Buy the Cheap Term Policy: You secure that 20-year, $500,000 term policy for just $30 a month. Your family is instantly protected.

- Calculate the Difference: If the whole life policy was going to cost you $300 a month, you now have an extra $270 in your monthly budget.

- Invest the Savings: Instead of giving that $270 to an insurance company, you set up an automatic transfer to a low-cost S&P 500 index fund in a Roth IRA or standard brokerage account.

The Wealth-Building Math

Let us see what happens when you invest that $270 every month for 20 years, assuming a conservative historical market return of about 8% annually.

| Investment Strategy | Monthly Contribution | Time Horizon | Estimated Future Value |

|---|---|---|---|

| Index Fund (8% Return) | $270 | 10 Years | $49,000+ |

| Index Fund (8% Return) | $270 | 20 Years | $158,000+ |

| Index Fund (8% Return) | $270 | 30 Years | $398,000+ |

By the time your 20-year term policy expires, you will have built an investment portfolio worth over $158,000. At that point, your house is likely paid off, your kids are grown and financially independent, and you have a massive nest egg. You are effectively self-insured! You no longer need life insurance because you have built your own wealth. This is the power of frugal living combined with smart investing. You save $3,240/year by avoiding whole life, and you turn those savings into a fortune.

Scam Warning: Surviving the Sales Pitch

If buying term and investing the difference is so mathematically superior, why do so many people buy whole life insurance? The answer is simple: commissions. Life insurance agents make massive commissions selling whole life policies. Often, they pocket 50% to 100% of your entire first year’s premium. If you are paying $3,600 a year, the agent might be walking away with a $3,000 payday just for signing you up.

Scam Warning: Beware of agents who use buzzwords like ‘Be your own bank,’ ‘Infinite banking,’ or ‘Tax-free wealth generation.’ These are aggressive marketing tactics designed to sell you an overpriced whole life or universal life policy. If an agent tells you life insurance is an investment, run the other way.

You need to be prepared when you sit down with an agent or broker. They are trained to make you feel guilty, or to make their complex charts look incredibly appealing. As a frugal hacker, you must stand your ground.

Your Anti-Scam Scripts

Here are the exact scripts you can use to shut down a pushy agent and get exactly what you need:

- When they pitch whole life as an investment:

Script: ‘I appreciate the information, but I keep my insurance and my investments strictly separate. I am only interested in term life quotes today.’

- When they say term life is throwing money away:

Script: ‘I view term life like car insurance. I am paying for protection, not a return on investment. Please show me your best 20-year term rates.’

- When they refuse to take no for an answer:

Script: ‘It sounds like we have different financial philosophies. If you cannot provide straightforward term life quotes, I will have to take my business to an online broker. Thank you for your time.’

Remember, you are the customer. You hold the power. Never let a commissioned salesperson dictate your frugal financial plan.

Action Plan: Calculating Exactly How Much Coverage You Need

Now that you are completely sold on term life insurance, you need to figure out exactly how much coverage to buy. You do not want to overpay for too much coverage, but you also do not want to leave your family shortchanged. The best way to calculate this is using the DIME method.

The DIME Method Breakdown

DIME stands for Debt, Income, Mortgage, and Education. Grab a pen and paper, and let us add it up.

- Debt: Total up all your non-mortgage debt. This includes credit cards, student loans, personal loans, and car loans. You want this wiped clean for your family.

- Income: How much do you make a year? Multiply your current annual salary by the number of years your family would need support. A good rule of thumb is 10 to 12 years. If you make $50,000 a year, that is $500,000 to $600,000.

- Mortgage: What is the remaining balance on your home? You want your family to own the house free and clear.

- Education: If you have kids, estimate the cost of sending them to college. A safe estimate is $100,000 per child.

Example Budget Breakdown for Coverage

| DIME Category | Estimated Amount |

|---|---|

| Debt (Car + Student Loans) | $45,000 |

| Income ($60k x 10 years) | $600,000 |

| Mortgage Balance | $250,000 |

| Education (2 Kids) | $200,000 |

| Total Recommended Coverage | $1,095,000 |

In this example, you would shop for a $1,000,000 or $1.1 Million term life policy. While a million dollars sounds like a lot, a 20-year term policy for that amount is shockingly affordable for a healthy young adult, often costing less than $50 to $70 a month. By calculating your exact needs, you avoid the trap of guessing and ensure every penny of your premium is doing essential work.

Conclusion

There you have it, my frugal friends! You now have the ultimate blueprint for navigating the tricky world of life insurance. By understanding the massive cost difference between term and whole life, you can stop wasting money on bloated policies that only serve to enrich insurance agents. Remember, the goal of frugal living is not just to pinch pennies; it is to optimize your spending so you can build real, lasting wealth. Buy the affordable term policy, protect your family, and aggressively invest the difference. That is how you hack the system and win with money.

Take a few minutes today to review your current life insurance situation. If you are stuck in an expensive whole life policy, it might be time to shop for term coverage and make the switch. Your future self—and your bank account—will thank you.

Disclaimer: I am the Ultimate Frugal Hacker, a passionate advocate for smart money management, but I am not a certified financial advisor or licensed insurance agent. The strategies discussed in this article are for educational and informational purposes only. Always do your own research and consider consulting with a fee-only fiduciary financial planner before making major changes to your insurance or investment portfolios.

Makenzie is the founder and lead writer at MoneyHackTips.com — a personal finance blog dedicated to delivering street-smart financial wisdom for real people on real budgets. With 300+ published articles covering everything from debt management to investing fundamentals, Makenzie’s mission is to make every dollar work harder. When not writing about money hacks, Makenzie is testing frugal living strategies, optimizing side hustles, and helping readers build financial freedom from scratch.