Hey there, frugal friends! If you are anything like me, you probably get a thrill out of finding the absolute best deals. You meal prep like a boss, you know exactly which days the thrift store has its 50% off sales, and you would not dare pay full price for a piece of furniture. We work incredibly hard to stretch our dollars and build a comfortable life on a budget. But here is the harsh reality that many frugal living enthusiasts overlook: all that hard work can disappear in an afternoon if you are not protecting your assets.

Today, we are talking about the ultimate financial safety net: renters insurance. I know what you might be thinking. ‘Insurance? That sounds like another monthly bill I do not need!’ But stick with me here. What if I told you that for the price of a couple of fancy coffees or a basic streaming subscription—often around $12 to $20 a month—you could protect tens of thousands of dollars worth of your personal belongings? When you are living frugally, a major loss isn’t just an inconvenience; it is a financial disaster that can derail your budget for years. Let us dive into why every renter absolutely needs insurance, how it secretly covers way more than you think, and exactly how to hack the system to get the cheapest rate possible.

The Big Myth: My Landlord’s Insurance Covers Me

Let us bust the biggest, most dangerous myth in the renting world right now: the idea that your landlord’s insurance policy has your back. I hear this all the time from smart, budget-conscious people. They think, ‘Hey, the building is insured, so if there is a fire or a break-in, I am covered, right?’ Wrong. Dead wrong.

Your landlord’s insurance policy covers the physical structure of the building—the walls, the roof, the plumbing, and the floors. It covers their liability if someone trips on the front steps of the apartment complex. It covers absolutely zero of your personal belongings. If a pipe bursts and floods your apartment, the landlord’s policy will pay to replace the drywall and the carpets, but it will not pay a single dime for your ruined laptop, your soaked mattress, or your destroyed vintage clothing collection.

The Real Cost of Starting Over

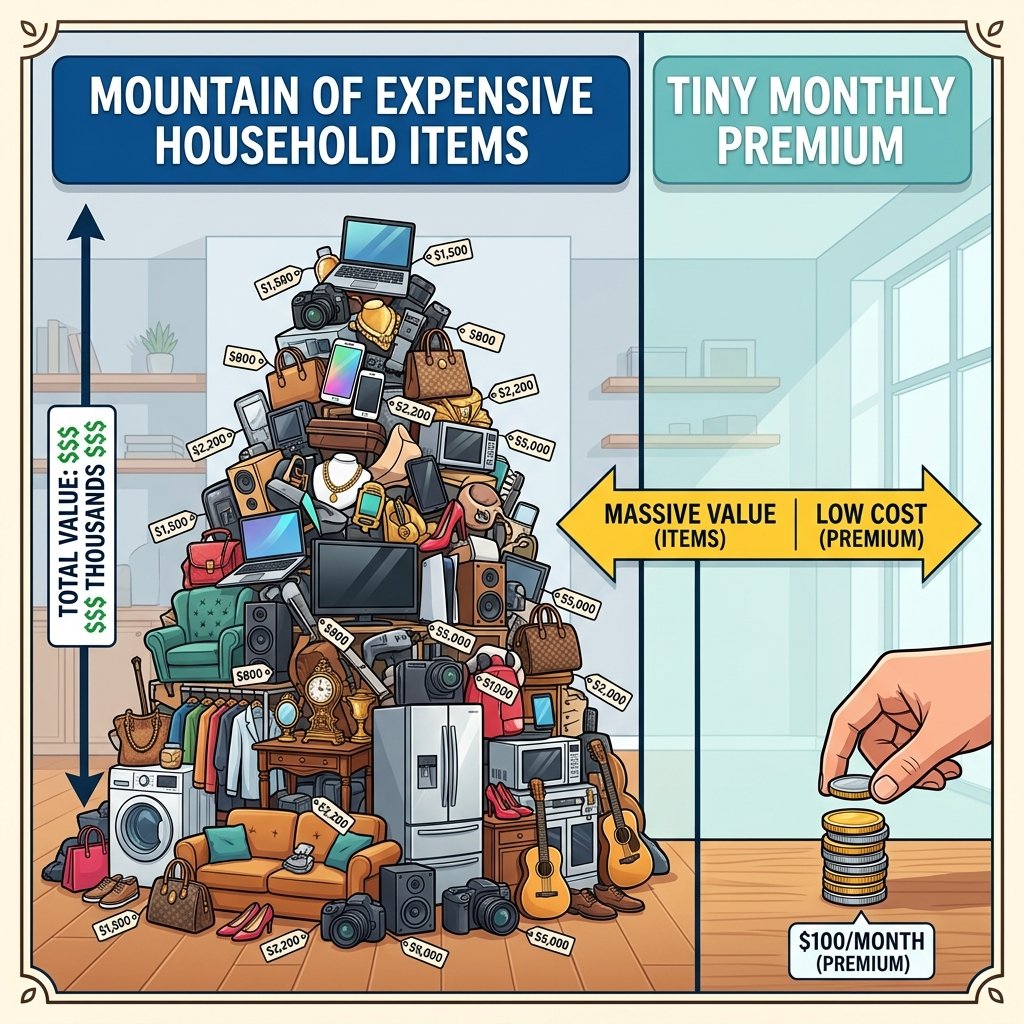

When you live frugally, you acquire things slowly over time. You might have bought your couch on Facebook Marketplace for $100, your TV on Black Friday for $200, and your kitchen gadgets at a garage sale. Because you didn’t spend a fortune all at once, you might underestimate what your stuff is actually worth. But if you had to go out tomorrow and replace everything you own at retail prices, the cost would be staggering. Renters insurance is the ultimate frugal hack because it transfers that massive financial risk away from you for pennies a day.

The Math: What You Pay vs. What You Stand to Lose

You know we love to break down the numbers here. Let us look at a realistic scenario for a budget-conscious renter. You might think your stuff isn’t worth much, but let us do a quick inventory of a basic one-bedroom apartment. The numbers add up incredibly fast.

| Item Category | Estimated Replacement Cost |

|---|---|

| Living Room (Sofa, TV, Rug, Decor) | $3,500 |

| Bedroom (Mattress, Frame, Dresser) | $2,000 |

| Clothing & Shoes (Entire Wardrobe) | $4,000 |

| Electronics (Laptop, Phone, Tablet) | $2,500 |

| Kitchen (Microwave, Pots, Dishes) | $1,000 |

| Miscellaneous (Books, Hobbies, Linens) | $1,500 |

The Frugal ROI (Return on Investment)

In this modest example, your personal property is worth $14,500. If a fire or theft wiped you out, could you easily pull $14,500 from your emergency fund to start over? For most of us, the answer is a resounding no. Now, compare that to the cost of a typical renters insurance policy, which averages about $15 per month, or $180 per year. You are paying a tiny fraction of a percent of your total asset value to guarantee you will never have to start from zero. That is not an expense; that is smart financial defense.

The Hidden Perks: Surprising Things Renters Insurance Covers

Here is where renters insurance goes from ‘good idea’ to ‘absolute necessity.’ It doesn’t just cover your stuff when it is sitting inside your apartment. A good policy is like an invisible force field that follows you around. Here are some of the incredible hidden perks that most people have no idea are included:

- Off-Premises Coverage: Did your laptop get stolen out of your car while you were grabbing groceries? Did someone swipe your bicycle from the rack outside the coffee shop? Renters insurance usually covers your belongings anywhere in the world.

- Personal Liability: If a guest trips over your rug and breaks their wrist, or if your normally sweet rescue dog gets spooked and bites a neighbor, you could be sued for medical bills. Renters insurance includes liability coverage, often up to $100,000, to pay for legal fees and medical costs.

- Loss of Use: If your apartment becomes uninhabitable due to a covered disaster (like a fire in the unit next door), your policy will pay for your hotel bills, extra food costs, and other living expenses while your place is being repaired.

- Spoiled Food: If a massive power outage hits your city and everything in your fully stocked freezer goes bad, many policies will reimburse you for the cost of the groceries. For a frugal meal-prepper, that can easily be $200 to $300 saved!

How to Hack Your Premium for the Lowest Rate

Alright, frugal hackers, let us talk strategy. Just because renters insurance is already cheap doesn’t mean we cannot make it cheaper. Insurance companies offer dozens of discounts, and if you know how to ask, you can slash your premium even further.

The Top Discount Hacks

- Bundle and Save: If you own a car, buy your renters insurance from the same company that provides your auto insurance. The multi-policy discount on your car insurance is often so large that it completely pays for the renters policy. You might literally get renters insurance for free!

- Increase Your Deductible: The deductible is the amount you pay out of pocket before insurance kicks in. If you raise your deductible from $250 to $500 or $1,000, your monthly premium will drop significantly. Since we are frugal and have an emergency fund, keeping a higher deductible is a smart calculated risk.

- Safety Features: Does your apartment have deadbolts, a burglar alarm, smoke detectors, or fire sprinklers? Tell your agent! Each of these safety features can shave a few percentage points off your bill.

- Pay in Full: Avoid the monthly convenience fee by paying your annual premium upfront in one lump sum. This can save you anywhere from $10 to $30 a year.

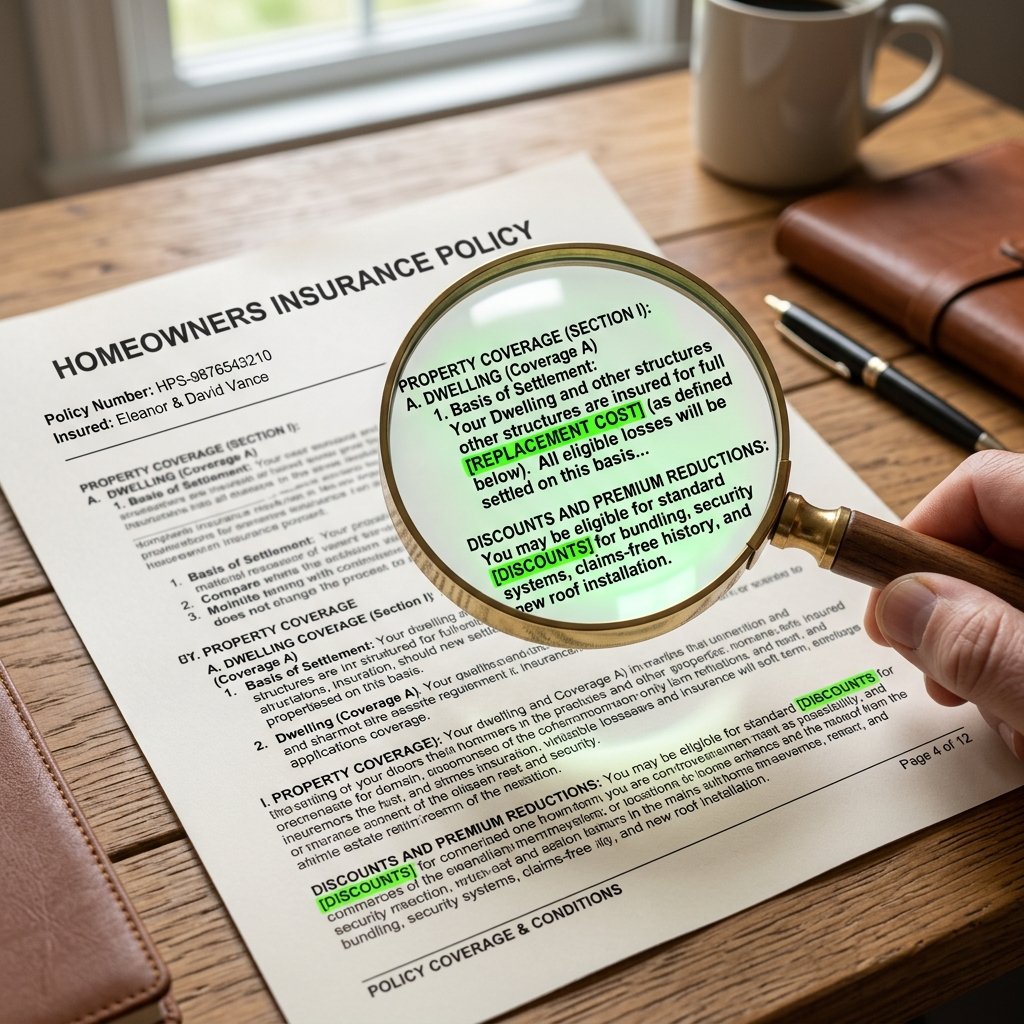

SCAM WARNING: Actual Cash Value vs. Replacement Cost

When buying a policy, you will be offered two choices: Actual Cash Value (ACV) or Replacement Cost. Never, ever choose ACV. ACV pays you what your item is worth today (e.g., $50 for a 5-year-old TV). Replacement Cost pays you what it costs to buy a brand new version of that item today (e.g., $400 for a new TV). Always pay the extra dollar or two a month for Replacement Cost coverage!

The Script: How to Shop and What to Ask

Ready to pull the trigger? Shopping for renters insurance is incredibly easy. You can get quotes online from major providers in about five minutes. But if you prefer speaking to an agent to make sure you are getting every possible discount, here is the exact script you should use.

The Frugal Hacker’s Negotiation Script:

‘Hi there, I am currently shopping for a new renters insurance policy and I am looking for the most competitive rate. I need a quote for a policy with $20,000 in personal property coverage and $100,000 in liability. I want to make sure the quote includes Replacement Cost, not Actual Cash Value. Also, I have smoke detectors and deadbolts in my unit. Can you run the numbers with a $500 deductible, and let me know what discounts I qualify for if I bundle this with my auto insurance or pay for the entire year upfront?’

Using this script shows the agent that you are an educated consumer who knows exactly what they want. It cuts out the fluff and gets you straight to the bottom-line numbers.

Conclusion

At the end of the day, frugal living isn’t just about spending less money; it is about spending your money strategically. You hustle hard to save your cash, build your emergency fund, and create a comfortable home. Do not leave all that hard work exposed to chance. For the price of a couple of fast-food meals a month, you can buy absolute peace of mind. Get a quote today, bundle it with your car insurance, and sleep soundly knowing your stuff is fully protected.

Disclaimer: I am a frugal living enthusiast, not a licensed financial advisor or insurance agent. The information provided in this article is for educational and entertainment purposes only. Insurance policies vary widely by state and provider. Always read the fine print of your specific policy and consult with a licensed professional to ensure you have the appropriate coverage for your unique situation.

Makenzie is the founder and lead writer at MoneyHackTips.com — a personal finance blog dedicated to delivering street-smart financial wisdom for real people on real budgets. With 300+ published articles covering everything from debt management to investing fundamentals, Makenzie’s mission is to make every dollar work harder. When not writing about money hacks, Makenzie is testing frugal living strategies, optimizing side hustles, and helping readers build financial freedom from scratch.