Hey there, fellow frugal hackers! Let’s have a real, street-smart talk about one of the biggest budget-drainers sitting right out there in your driveway. You guessed it—your car. More specifically, that bloated, interest-heavy auto loan you signed up for at the dealership. If you are serious about living a frugal lifestyle, keeping your hard-earned cash where it belongs (in your bank account), and outsmarting the system, you cannot afford to ignore your car payment.

When most people buy a car, they are exhausted by the time they reach the finance manager’s office. They sign the paperwork, accept whatever interest rate the dealer throws at them, and spend the next five to seven years overpaying. But not you. You are here because you know there is a better way. Refinancing your car loan is one of the ultimate financial hacks. It is not just for houses; it is a powerful tool to lower your monthly expenses, reduce the total interest you pay, and free up cash for the things that actually matter to you.

In this comprehensive, no-fluff guide, we are going to break down exactly how to refinance your car loan. We will look at the hard math, walk through the exact steps to prep your finances, give you the word-for-word scripts to negotiate with lenders, and warn you about the shady traps designed to keep you broke. Grab your favorite affordable beverage, pull up a chair, and let’s get ready to hack your car payment and save you thousands.

The Math: Why Refinancing is a Frugal Superpower

Before we dive into the “how,” we need to talk about the “why.” The secret to frugal living isn’t just clipping coupons; it’s optimizing your big fixed expenses. The interest rate (APR) on your car loan dictates how much extra money you are handing over to the bank every month. If your credit score has improved since you bought the car, or if national interest rates have dropped, you are leaving money on the table by not refinancing.

Let’s Look at the Real Numbers

Let’s say you bought a car a year ago. Your credit wasn’t stellar, so the dealership stuck you with a high interest rate. Now, you have been paying your bills on time, your credit score has jumped, and you qualify for a much better rate. Here is how the math breaks down over the remaining life of a loan.

| Loan Details | Original Dealership Loan | Refinanced Loan (The Hack) |

|---|---|---|

| Remaining Balance | $20,000 | $20,000 |

| Interest Rate (APR) | 9.5% | 4.5% |

| Remaining Term | 48 Months | 48 Months |

| Monthly Payment | $502 | $456 |

| Total Interest Paid | $4,118 | $1,889 |

By simply taking a few hours to refinance, you save $46 every single month. Over the life of the loan, you keep $2,229 in your pocket! That is money you can use to build your emergency fund, invest, or fund your next frugal adventure. The math does not lie: lowering your APR is one of the highest ROI (Return on Investment) activities you can do this weekend.

The Prep Work: Getting Your Frugal Ducks in a Row

You wouldn’t start a DIY project without gathering your tools first, right? The same goes for refinancing. To get the absolute best rates and ensure a smooth process, you need to do a little prep work. Lenders are going to look closely at your financial profile and your vehicle’s value. Here is your ultimate checklist to get ready.

1. Check Your Credit Score

Your credit score is the golden ticket to a lower interest rate. You can check this for free using your credit card’s app or a free service like Credit Karma. If your score has gone up by 50 points or more since you originally bought the car, you are in a prime position to refinance.

2. Calculate Your Loan-to-Value (LTV) Ratio

Lenders want to make sure your car is worth more than what you owe. If you owe $15,000 but the car is only worth $10,000, you are “underwater” or “upside down” on the loan. Most lenders require an LTV ratio of 125% or less to approve a refinance.

- Find your exact payoff amount by calling your current lender or checking your online portal.

- Check the current value of your car using Kelley Blue Book (KBB) or Edmunds.

- Divide the payoff amount by the car’s value to get your LTV percentage.

3. Gather Your Documents

Having everything ready will make the application process lightning fast. You will need:

- Your driver’s license and proof of insurance.

- Your vehicle’s VIN (Vehicle Identification Number), year, make, and model.

- Your current loan details (lender name, account number, 10-day payoff amount).

- Proof of income (your last two pay stubs or recent tax returns).

Once you have this arsenal of information ready, you are fully equipped to start hunting for the best deal.

The Step-By-Step Hack: How to Actually Do It

Alright, it is time for action. This is the street-smart strategy to ensure you don’t just get a new loan, but you get the *best possible* loan. Do not just go to your current bank and accept their first offer. We are going to make lenders compete for your business.

Step 1: Shop the Credit Unions First

Local credit unions are the unsung heroes of the frugal world. Because they are not-for-profit, they consistently offer lower auto loan rates than big national banks. Look up two or three credit unions in your area or ones you qualify for through your employer, and check their published auto refinance rates online.

Step 2: Apply in a 14-Day Window

When you apply for a loan, the lender does a “hard pull” on your credit, which can temporarily ding your score. However, the credit bureaus are smart. If they see you applying for multiple auto loans within a 14-to-45-day window, they count it as a single inquiry because they know you are rate shopping. So, set aside a Saturday morning and submit all your applications at once.

- Apply at your top-choice local credit union.

- Apply with an online aggregator (like Bankrate or NerdWallet) to see offers from online-only banks.

- Apply with your current bank just to see what they offer.

Step 3: Compare the True Cost

When the offers roll in, do not just look at the monthly payment. Shady lenders will lower your monthly payment by extending the life of your loan (e.g., taking you from 48 months left to 72 months). This means you pay *more* interest over time! Always compare the APR and keep the loan term the same or shorter than what you currently have.

Step 4: Execute the Payoff

Once you select the winning lender, they will guide you through signing the digital paperwork. In most cases, your new lender will send a check directly to your old lender to pay off the original loan. Keep a close eye on your old account to ensure it hits a $0.00 balance. Do not skip a payment on your old loan until you have written confirmation that it has been paid off in full!

The Scripts: Exactly What to Say to Lenders

A true frugal hacker knows that everything is negotiable. If you love your current bank but they aren’t offering the best rate, or if you want to waive a sneaky origination fee, you need to know how to talk to them. Confidence is key. Use these exact scripts to command respect and get the deals you deserve.

Script 1: Asking Your Current Lender to Match a Rate

If you found a killer rate at a credit union but want the convenience of staying with your current bank, call their loan retention department and say:

“Hi there. I have been a loyal customer for years, and I currently have an auto loan with you at an 8% APR. I have just been pre-approved for a refinance with a local credit union at 4.5%. I would prefer to keep my business with you for convenience. Can you match or beat this 4.5% rate so I don’t have to move my loan?”

If they say no, calmly thank them and move your money. Loyalty doesn’t pay the bills; low interest rates do.

Script 2: Negotiating Away Origination Fees

Some lenders try to tack on “origination fees” or “processing fees” to set up the new loan. This eats into your savings. When you are reviewing the final terms, if you see a fee, use this script:

“I am looking at the loan estimate, and I see a processing fee of $150. Since I have excellent credit and a straightforward application, I am asking that you waive this fee to earn my business. If we can remove that, I am ready to sign the paperwork today.”

Remember, the person on the other end of the phone wants to close the deal. Give them a reason to advocate for you.

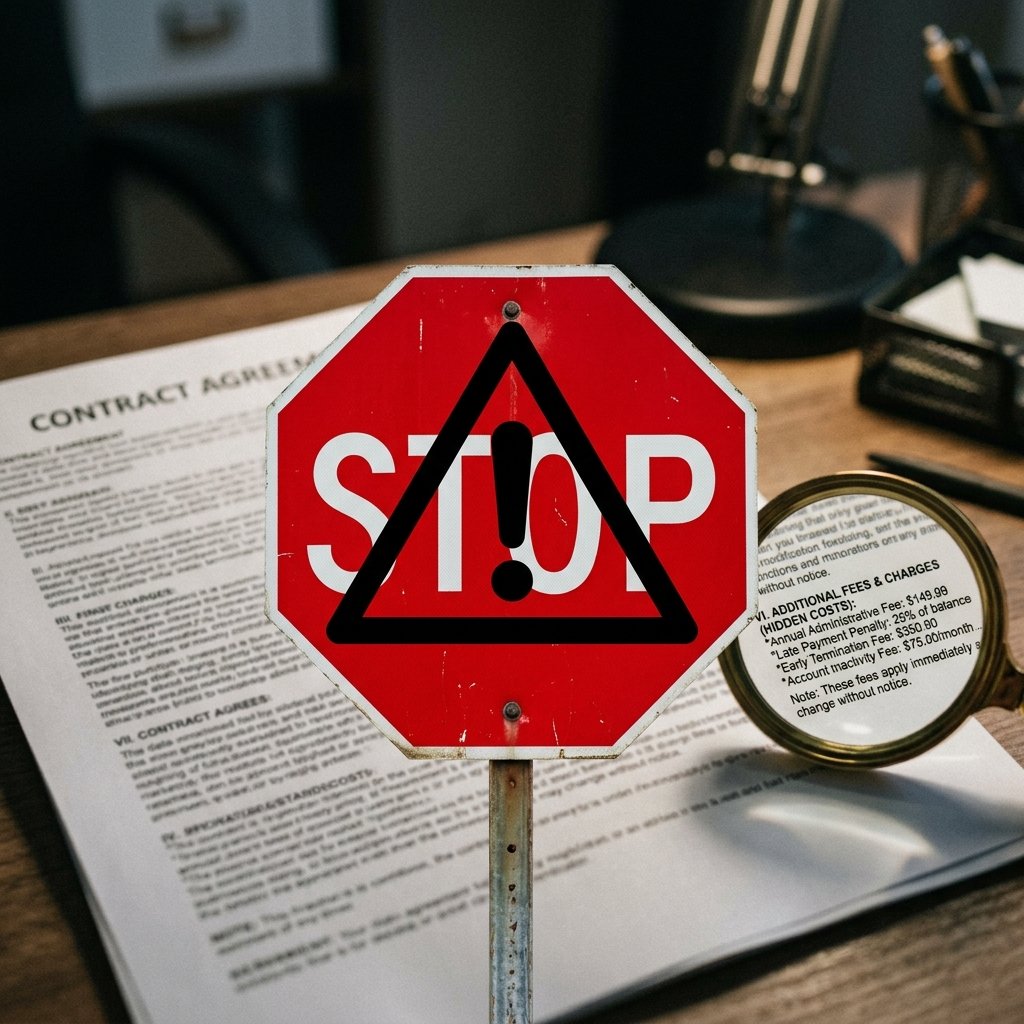

Scam Warnings and The “Gotchas” of Refinancing

While refinancing is a brilliant strategy, the financial industry is full of landmines designed to trip up the uninformed consumer. As your frugal guide, I need to make sure you protect your hard-earned cash from predatory tactics. Keep your eyes peeled for these common “gotchas” and outright scams.

The Prepayment Penalty Trap

Before you even apply to refinance, check the fine print of your *current* auto loan. Some predatory lenders include a prepayment penalty. This means they actually charge you a fee for paying off your loan early! If the penalty is $500, but refinancing only saves you $300 in interest, the math no longer works in your favor. Always calculate the net savings.

The Term-Extension Illusion

I mentioned this earlier, but it bears repeating because it is the most common trick in the book. A lender might say, “Great news! We can lower your payment from $400 to $250!” But what they don’t tell you is that they stretched your remaining 3-year loan into a brand new 6-year loan. You will end up paying thousands more in interest. Always focus on the APR, not just the monthly payment.

The Upfront Fee Scam

This is a major red flag. Legitimate lenders do not charge you money just to look at an application. If a company reaches out to you claiming they can guarantee a ridiculously low rate, but they need a deposit first, run the other way.

SCAM WARNING: Never, ever pay an upfront “application fee,” “lock-in fee,” or “consultation fee” via wire transfer, gift card, or cash app to secure an auto loan refinance. Legitimate lenders will roll any minor processing fees into the loan itself or deduct it at closing. Upfront cash demands are almost always a scam.

Conclusion

There you have it—the ultimate, step-by-step frugal hacker’s guide to refinancing your car loan. By understanding the math, gathering your documents, shopping around strategically, and using the right negotiation scripts, you can break free from the chains of a terrible auto loan. Remember, every dollar you save on interest is a dollar you get to put towards your true financial goals. Don’t let the dealership win. Take an hour this week to check your rates and see if you can give yourself a massive pay raise by simply lowering your car payment.

Stay smart, stay frugal, and keep hacking your way to financial freedom!

Disclaimer: I am “The Ultimate Frugal Hacker” and a passionate frugal living enthusiast sharing my personal strategies and hacks. I am not a certified financial advisor, tax professional, or legal expert. The information provided in this article is for educational and entertainment purposes only. Always do your own research, read the fine print, and consider consulting with a licensed financial professional before making any major financial decisions or signing legal contracts.

Makenzie is the founder and lead writer at MoneyHackTips.com — a personal finance blog dedicated to delivering street-smart financial wisdom for real people on real budgets. With 300+ published articles covering everything from debt management to investing fundamentals, Makenzie’s mission is to make every dollar work harder. When not writing about money hacks, Makenzie is testing frugal living strategies, optimizing side hustles, and helping readers build financial freedom from scratch.