Hey there, frugal friends! It is your ultimate frugal hacker here, ready to tackle one of the absolute biggest budget-drainers in your monthly expenses: car insurance. If you are anything like me, you work incredibly hard for every single dollar you earn. So, why on earth would you let a massive, faceless insurance corporation quietly siphon away your hard-earned cash month after month? The truth is, most people set their car insurance to auto-pay and completely forget about it. They assume that because they have not gotten into an accident, they are getting the best possible rate. Spoiler alert: you are probably overpaying, and the insurance companies are banking on your complacency. But today, that stops. We are going to dive deep into the street-smart, highly effective strategies that the savvy savers use to keep more money in their pockets. By the time you finish reading this guide, you will have a rock-solid action plan to slash your premiums, optimize your coverage, and take back control of your budget. Grab a cup of coffee, pull up your current policy declaration page, and let us get to work on saving you hundreds, if not thousands, of dollars this year!

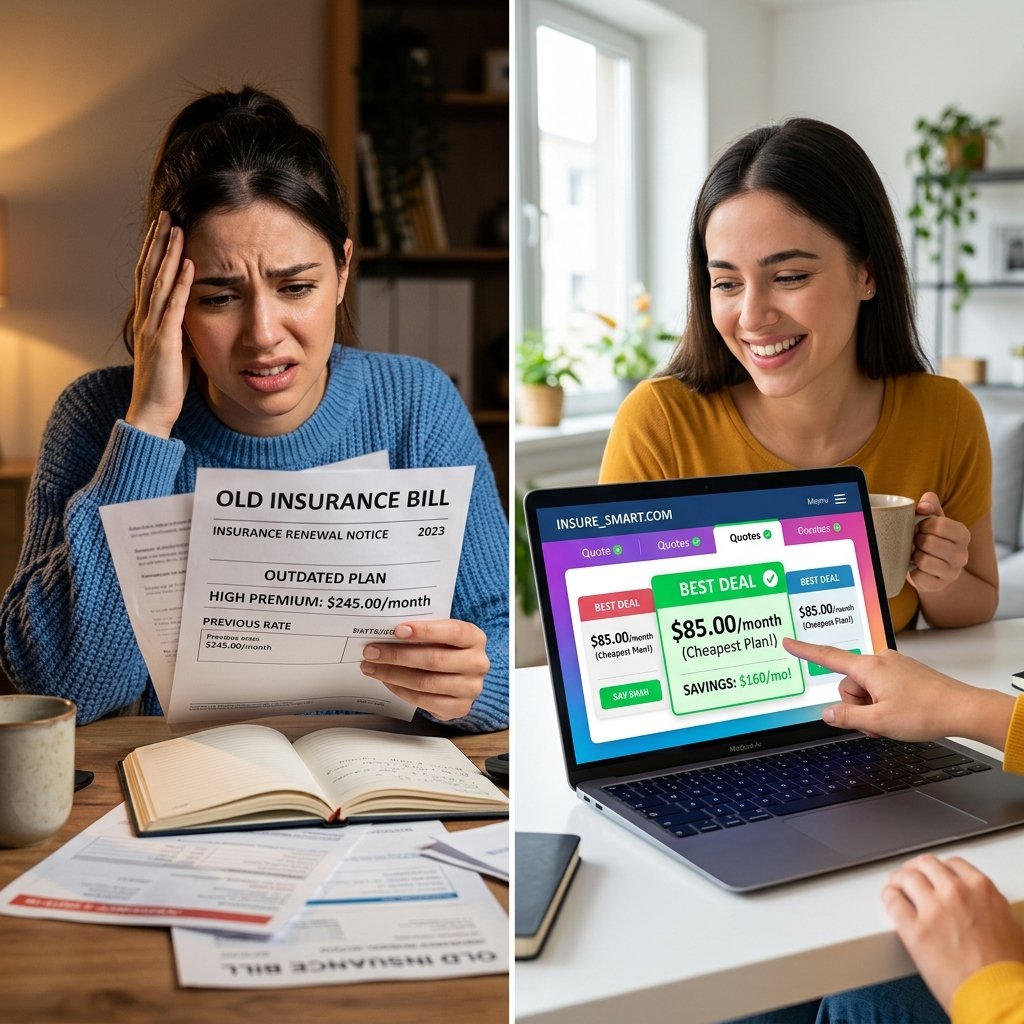

Secret 1: Shop Around Like a Pro (Defeat the Loyalty Penalty)

Let us get one thing straight right out of the gate: loyalty to your car insurance company does not pay. In fact, it actually costs you money. This is a phenomenon known in the industry as price optimization. Insurance algorithms are incredibly sophisticated; they can predict exactly how much they can raise your rates each year before you get annoyed enough to leave. If you have been with the same company for more than two years, you are almost certainly paying a loyalty penalty. The absolute best way to combat this is to aggressively shop your rate at least once a year, or ideally every six months.

How to Execute This Hack

Do not just check one or two big-name companies. You need to use independent insurance brokers who can pull quotes from dozens of smaller, highly rated regional carriers that do not spend billions on television commercials. These smaller companies often pass those advertising savings directly onto you. Set a calendar reminder every six months, right before your policy renews, to dedicate just one hour to gathering quotes.

| Strategy | Average Annual Cost | Potential Savings |

|---|---|---|

| Staying Loyal (5+ Years) | $1,850 | $0 |

| Comparing Quotes Annually | $1,200 | $650 |

Key Rule: Never let your insurance auto-renew without spending at least 30 minutes verifying that it is still the most competitive rate on the market. Your loyalty is to your own bank account, not to a mascot on a commercial.

Secret 2: Raise Your Deductible (The Calculated Risk)

This is where the math really starts working in your favor. Your deductible is the amount of money you agree to pay out of pocket before your insurance kicks in after an accident. Most people default to a $500 deductible because it feels safe. But if you are a safe driver who rarely gets into accidents, you are essentially paying extra every single month for a benefit you never use. By raising your deductible to $1,000 or even $1,500, you take on slightly more risk, but your insurance company will reward you with significantly lower monthly premiums.

The Math Example

Let us say raising your deductible from $500 to $1,000 saves you $200/year on your premium. If you go three years without an accident, you have saved $600. You have already mathematically beaten the system! The secret to making this work without causing financial stress is to take the money you save on your premium and put it directly into a dedicated emergency fund.

- Step 1: Request a quote for a higher deductible from your current provider.

- Step 2: Calculate the annual savings.

- Step 3: Transfer the difference into a high-yield savings account so the cash is there if you ever actually need to pay that deductible.

Secret 3: The Bundle Hustle (Combine and Conquer)

You have probably heard the commercials telling you to bundle your home and auto insurance, but have you actually done the math to see how much it saves? Insurance companies absolutely love customers who have multiple lines of business with them because it statistically lowers the chance of that customer leaving. They want your auto, your renters or homeowners, your motorcycle, and your umbrella policy all under one roof. Because they want it so badly, they are willing to offer massive discounts to get it.

Unlocking the Best Bundle Rates

Even if you do not own a home, you can bundle renters insurance with your auto policy. Renters insurance is incredibly cheap—often around $15 to $20 a month. Sometimes, the multi-line discount applied to your expensive auto policy is actually larger than the entire cost of the renters insurance! That means they are essentially paying you to insure your apartment.

| Policy Setup | Total Monthly Cost | Annual Savings |

|---|---|---|

| Auto and Renters (Separate) | $180 | $0 |

| Auto and Renters (Bundled) | $145 | $420 |

Always ask your agent to run the numbers both ways. Sometimes, keeping them separate with two different highly competitive companies is cheaper, but 80% of the time, the bundle hustle wins out.

Secret 4: Demand the Hidden Discounts (Ask and You Shall Receive)

Insurance companies offer dozens of discounts, but they are not going to magically apply them to your account unless you ask. They rely on the fact that you will not pick up the phone. Are you working from home now and driving less? That is a low-mileage discount. Did you recently get married? That is a discount. Did your teenager get on the honor roll? Good student discount. Are you a member of a specific alumni association, credit union, or professional organization? Affinity discount.

The Script to Use

Do not just guess what discounts you might qualify for. Pick up the phone, call your agent or customer service, and use this exact script to force them to review your file.

Hi there! I am currently doing a thorough review of my household budget, and I want to make sure I am getting the absolute best possible rate on my auto policy. Can we please do a comprehensive policy review together right now? I want to go through every single discount your company offers—from low-mileage to defensive driving courses to occupational discounts—to see what I might qualify for today. If we cannot get this rate down, I will unfortunately have to start shopping with competitors.

By being polite but firm, you signal that you are a savvy consumer who is ready to walk if they do not sharpen their pencil. You can easily shave $100 to $300 off your annual bill just by making a ten-minute phone call.

Secret 5: Drop the Dead Weight on Older Vehicles

If you are driving an older, paid-off vehicle, you might be throwing money out the window by carrying full coverage. Full coverage typically includes collision (pays to fix your car if you hit something) and comprehensive (pays if a tree falls on it, it gets stolen, etc.). But here is the frugal reality check: insurance companies will never pay out more than the actual cash value of your car. If your 15-year-old sedan is only worth $2,500, and your deductible is $1,000, the absolute maximum payout you will ever see is $1,500. Yet, you might be paying $400/year just for that specific coverage!

The 10 Percent Rule

Financial experts and frugal hackers use a simple math equation called the 10% Rule. If your annual cost for comprehensive and collision coverage is more than 10% of your car’s total payoff value, it is time to drop those coverages and stick to liability only.

- Look up the private party value of your vehicle on Kelley Blue Book or Edmunds.

- Subtract your current deductible from that value. This is your maximum potential payout.

- Look at your insurance declaration page to see exactly how much you are paying annually for just the collision and comprehensive portions.

- If the cost is higher than 10% of the potential payout, drop it, and put that premium money into your car replacement savings fund instead.

Secret 6: Hack Your Credit Score for Better Rates

This secret often catches people off guard, but in almost every US state (with a few exceptions like California, Hawaii, and Massachusetts), your credit score directly impacts your car insurance rate. Insurance companies use a credit-based insurance score to predict how likely you are to file a claim. Statistically, people with lower credit scores file more claims. Therefore, if your credit score is in the dumps, you are being penalized with significantly higher premiums—sometimes paying literally double what someone with excellent credit pays for the exact same coverage.

How to Fix It

Treating your credit score as a vital part of your frugal living strategy is non-negotiable. If you want to stop overpaying, you need to hack your credit.

- Pull your free credit report annually and dispute any errors immediately.

- Keep your credit utilization ratio below 30% (ideally below 10%).

- Set up auto-pay for all your credit cards and loans so you never miss a payment.

| Credit Tier | Average Annual Premium | The Credit Penalty |

|---|---|---|

| Excellent (800+) | $1,100 | $0 |

| Good (670-739) | $1,450 | $350 |

| Poor (Under 580) | $2,800 | $1,700 |

As your score improves, call your insurance company and ask them to recalculate your rate based on your new, higher tier. Do not wait for renewal!

Secret 7: Embrace Telematics (Let Them Track Your Good Habits)

If you are a genuinely safe driver who does not speed, does not slam on the brakes, and does not drive at 2 AM, you need to leverage telematics. Telematics, or usage-based insurance, involves using a smartphone app or a small device plugged into your car to track your driving habits. Programs like Progressive Snapshot, State Farm Drive Safe & Save, or Allstate Drivewise reward you for your actual driving behavior rather than relying solely on demographic algorithms.

The Payoff

Most companies offer an immediate discount of 5% to 10% just for signing up. But the real magic happens when you complete the evaluation period. Safe drivers can see their rates slashed by up to 30% or even 40%. Yes, there is a privacy trade-off because you are allowing the company to track your location and speed. But as a frugal hacker, you have to weigh the privacy concern against the massive financial gain. If you are comfortable with it, telematics is the closest thing to printing free money on your auto insurance.

Scam Warning: Be careful with some lesser-known third-party tracking apps that promise to shop rates for you based on your driving. Stick to the official programs offered directly by major, reputable insurance carriers to ensure your data is protected and the discounts are legitimate.

Conclusion

There you have it—seven actionable, street-smart secrets to stop overpaying and slash your car insurance bill today. Frugal living is not about depriving yourself; it is about optimizing your expenses so you can spend your hard-earned money on the things that truly matter to you. By shopping around, tweaking your deductibles, demanding hidden discounts, and optimizing your coverage, you are taking back control of your financial life. Do not let these tips just sit in your brain. Take action today. Pull out your policy, make that phone call, and start keeping your money where it belongs: in your wallet.

Disclaimer: I am your ultimate frugal hacker, not a licensed financial advisor or insurance broker. The strategies shared here are for educational and informational purposes only. Insurance laws vary wildly by state, and individual circumstances dictate coverage needs. Always read the fine print of your insurance policies and consult with a certified professional if you need personalized financial or legal advice.

Makenzie is the founder and lead writer at MoneyHackTips.com — a personal finance blog dedicated to delivering street-smart financial wisdom for real people on real budgets. With 300+ published articles covering everything from debt management to investing fundamentals, Makenzie’s mission is to make every dollar work harder. When not writing about money hacks, Makenzie is testing frugal living strategies, optimizing side hustles, and helping readers build financial freedom from scratch.