Hey there, fellow frugal hackers! Let us talk about one of the biggest wealth killers sitting right in your driveway: your car. If you have ever walked into a dealership, smelled that intoxicating “new car smell,” and suddenly found yourself justifying a $500 a month payment for a car you do not even own, you are not alone. The auto industry spends billions of dollars every year to convince us that leasing is the smart, hassle-free way to drive a reliable vehicle. But today, we are ripping the band-aid off.

Welcome to the ultimate showdown of Leasing vs. Buying. As frugal living enthusiasts, we know that every dollar counts. We do not care about impressing the neighbors with a shiny new hood ornament; we care about building financial freedom, crushing our money goals, and keeping our hard-earned cash where it belongs—in our bank accounts. The shocking truth about car payments is that they are designed to keep you on a perpetual hamster wheel of debt.

In this guide, we are going to expose the dealership illusions, break down the brutal math of what a lease actually costs you over time, and give you the ultimate frugal strategy to drive for a fraction of the cost. Grab a cup of coffee, pull up a chair, and let us dive into the numbers. It is time to take back control of your wallet!

The Dealership Trap: Why Monthly Payments Are an Illusion

When you walk onto a car lot, the very first question a salesperson will ask you is usually, “What kind of monthly payment are you looking for?” This sounds like they are trying to be helpful and respect your budget, right? Wrong. This is the oldest trick in the dealership playbook. By focusing your attention entirely on the monthly payment, they can manipulate the terms of the lease or loan to squeeze maximum profit out of your pocket.

Leasing is essentially long-term renting. You are paying for the vehicle’s depreciation during the time you drive it, plus a hefty fee (the money factor, which is just interest in disguise), and dealership fees. Because you are only paying for a portion of the car’s life, the monthly payment looks incredibly attractive compared to a traditional auto loan. But that is exactly how the trap snaps shut.

Key Rule: Never, ever negotiate based on the monthly payment. Always negotiate the total out-the-door price of the vehicle. Dealerships use the monthly payment to hide the true cost of the car, extending terms to 72 or even 84 months just to make the math look friendly.

The Psychology of the Upgrade

Dealerships know that human beings love instant gratification. Leasing offers you the ability to drive a car that is technically outside of your price range. Sure, you might only be able to afford to buy a $15,000 used Honda, but with a lease, that same monthly budget suddenly puts you behind the wheel of a brand-new $35,000 luxury crossover. It is financial smoke and mirrors. You get the status symbol today, but you sacrifice your financial security tomorrow. Every time your lease is up, you are left with zero equity and are forced to start the cycle all over again.

The Brutal Math: Cost Breakdown of Leasing vs. Buying

Alright, frugal hackers, let us get down to the numbers. We are going to look at a realistic 6-year scenario. Why 6 years? Because that is the length of two standard 3-year leases, or the time it takes to comfortably pay off a used car and enjoy some payment-free driving.

In this scenario, Person A decides to lease a brand-new car, turning it in every 3 years for a new one. Person B decides to buy a reliable 3-year-old used car, finances it for 5 years, and keeps it for a total of 6 years. Let us look at how the costs stack up.

| Expense Category | Leasing (Two 3-Year Leases) | Buying (3-Year-Old Used Car) |

|---|---|---|

| Down Payments | $6,000 ($3,000 x 2) | $4,000 |

| Monthly Payments | $28,800 ($400/mo x 72 mos) | $18,000 ($300/mo x 60 mos, then $0) |

| Insurance (Estimated) | $9,000 (Higher premiums required) | $6,000 (Lower premiums) |

| Hidden Fees / Turn-in | $1,500 (Mileage, wear & tear) | $0 |

| Maintenance & Repairs | $1,000 (Mostly covered by warranty) | $4,500 (Out of pocket) |

| Total Out of Pocket | $46,300 | $32,500 |

| Asset Value at End of Year 6 | $0 (You own nothing) | $8,000 (Trade-in/Sale value) |

| TRUE NET COST | $46,300 | $24,500 |

Look at that bottom line. By choosing to buy a slightly used, reliable car instead of getting caught in the leasing cycle, Person B has a true net cost that is $21,800 lower over 6 years! That is a savings of over $3,600/year. Imagine what you could do with an extra $3,600 annually. You could max out a Roth IRA, build a massive emergency fund, or take a debt-free vacation. The math does not lie: leasing is a luxury tax you pay for the privilege of driving a new car.

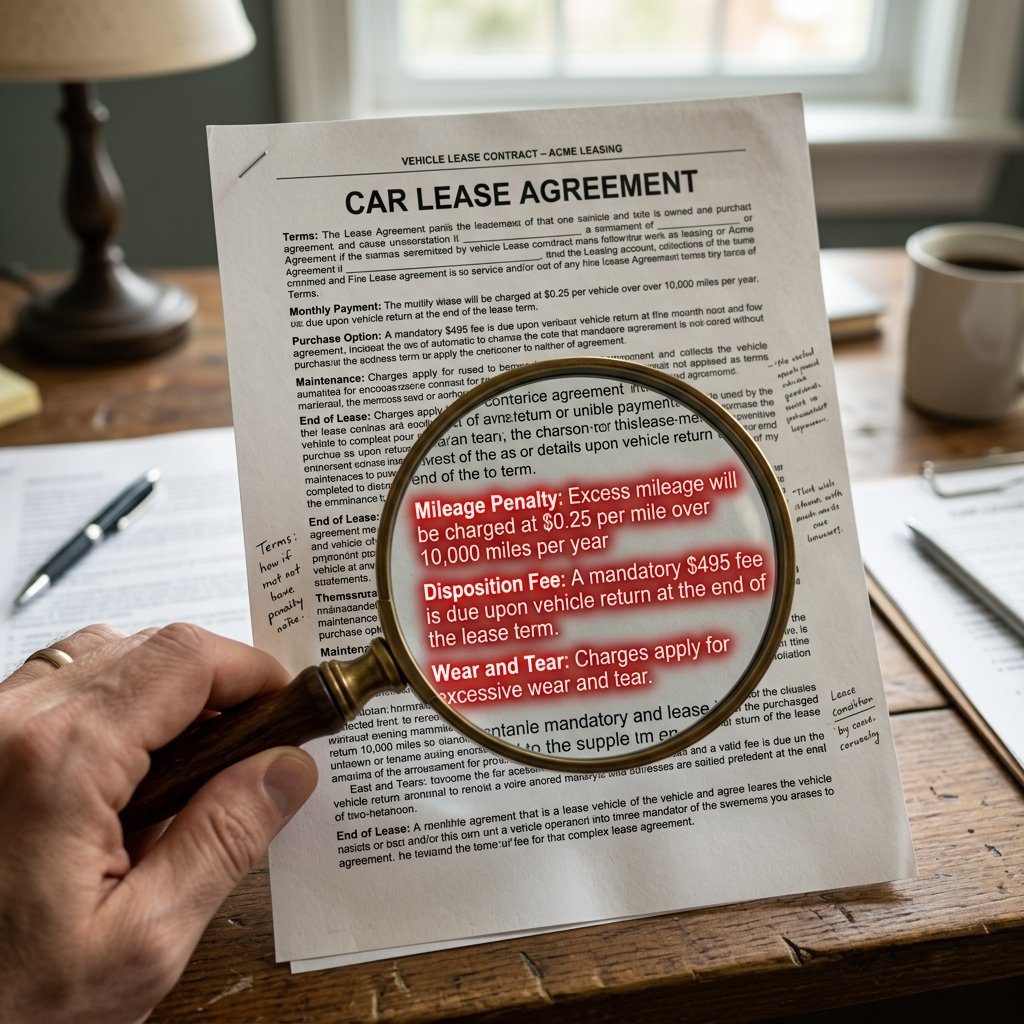

Watch Your Wallet: Hidden Fees and Lease Scams

If the baseline math of leasing wasn’t bad enough, the hidden fees will absolutely drain your wallet. When you buy a car, a scratch on the bumper is just a cosmetic annoyance. When you lease a car, that same scratch is a penalty waiting to happen. The leasing industry is notorious for nickel-and-diming consumers at the end of their lease terms.

The Mileage Trap

Most advertised lease specials come with a strict mileage limit—usually 10,000 to 12,000 miles per year. If you have a longer commute, like to take road trips, or just drive a bit more than average, you are going to get hit with a hefty per-mile penalty when you turn the car in. At $0.25 per mile over the limit, going just 5,000 miles over your contract will cost you a whopping $1,250 out of pocket!

Wear and Tear Nightmares

Dealerships expect the car back in “normal” condition. But their definition of normal and yours might be vastly different. Bald tires? You are paying for new ones. A stain on the upholstery from your morning coffee? That is a detailing fee. A ding from a rogue shopping cart? Get ready to pay dealership auto body rates.

Scam Warning: Beware the “Sign and Drive” illusion. Dealerships will heavily advertise zero-down leases to get you in the door. What they don’t tell you is that they roll the taxes, registration, and dealership fees into your monthly payment, jacking up the interest you pay on those fees. Furthermore, if you total a leased car that you put zero down on, you could be massively underwater unless you purchased expensive GAP insurance.

Finally, do not forget the “Disposition Fee.” Yes, many leasing companies charge you a fee of $300 to $500 just for the privilege of giving the car back to them at the end of the contract. It is the ultimate insult to injury.

The Frugal Hacker Strategy: How to Drive for (Almost) Free

Now that we have exposed the shocking truth about car payments and the leasing trap, what is the ultimate frugal hacker strategy? How do we get from point A to point B without setting our hard-earned cash on fire? It is time to implement the “Drive Free” method.

Step 1: Buy Reliable, Ugly, and Used

Your goal is transportation, not a status symbol. Look for vehicles known for their bulletproof reliability—think used Honda Civics, Toyota Corollas, or Mazda 3s. Let someone else take the massive 20% to 30% depreciation hit that happens in the first two years of a new car’s life. If you can, save up and pay cash. If you must finance, keep the term to 36 or 48 months maximum, and make sure your payment is no more than 10% of your take-home pay.

Step 2: The “Forever Payment” Hack

Here is where the magic happens. Let’s say you financed that used car for $300 a month, and after 4 years, it is completely paid off. Most people celebrate by going out and buying a new car to get a new payment. Not you. You are a frugal hacker.

You keep driving that paid-off car, but you continue making that $300 payment—except now, you make it to your own high-yield savings account. If you drive that paid-off car for another 5 years while paying yourself, you will have saved $18,000 in cash! When your current car finally bites the dust, you walk into the dealership, pick out a fantastic used car, and drop a stack of cash on the desk. Boom. You never have a car payment to a bank again.

The Script: How to decline dealership upsells

When you are in the finance office buying your used car, the finance manager will try to sell you extended warranties, tire protection, and paint sealant. Look them in the eye and use this exact script: “I appreciate you showing me these options, but my budget is strictly capped at the out-the-door price we agreed upon. I will be declining all additional coverages today. Let’s move forward with the paperwork as is.” Be polite, but be an absolute brick wall.

- Do your own maintenance: Learn to change your own air filters, wiper blades, and even oil. This alone can save you $200/year.

- Shop around for insurance: Never auto-renew. Check rates every 6 months to ensure you are getting the best deal on your fully-owned vehicle.

- Keep it clean: Washing and vacuuming your car regularly protects the paint and interior, preserving its resale value when you are finally ready to upgrade.

Conclusion

The shocking truth about car payments is that they are entirely optional. Society has normalized the idea that you will always have a car payment, treating it like a utility bill such as electricity or water. But as frugal living enthusiasts, we refuse to play by those rules. By rejecting the leasing trap, doing the brutal math, and committing to buying reliable used cars, you can reclaim hundreds of thousands of dollars over your lifetime.

Stop funding the dealership’s fancy espresso machines and start funding your own financial freedom. Remember, the wealthiest people on paper are often the ones driving the most unassuming cars. It is time to break the cycle, pay yourself instead of the bank, and hit the road to true financial independence!

Disclaimer: I am “The Ultimate Frugal Hacker,” not a certified financial advisor. The information provided in this article is for educational and entertainment purposes only. Always do your own research and consult with a professional before making major financial decisions, taking out loans, or altering your financial strategy.

Makenzie is the founder and lead writer at MoneyHackTips.com — a personal finance blog dedicated to delivering street-smart financial wisdom for real people on real budgets. With 300+ published articles covering everything from debt management to investing fundamentals, Makenzie’s mission is to make every dollar work harder. When not writing about money hacks, Makenzie is testing frugal living strategies, optimizing side hustles, and helping readers build financial freedom from scratch.