The Credit Score Hack: How to Use a Secured Card to Boost Your Score Fast

Let’s cut the crap. A bad credit score is like a ball and chain on your wallet. It’s the silent killer of your financial goals, forcing you to pay sky-high interest rates on everything from car loans to mortgages. It’s the reason you get rejected for that slick apartment or even a new cell phone plan. You feel stuck, like you’re being punished for past mistakes. But what if I told you there’s a legit, powerful tool that the credit bureaus actually respect? A secret weapon that most people overlook? Forget shady credit repair scams. We’re talking about the secured credit card. It’s not a sign of failure; it’s your ladder out of the credit score basement. It’s time to stop letting a three-digit number control your life. In this guide, we’ll break down exactly how to use this underdog tool to take control, build your score, and start keeping more of your hard-earned cash in your pocket.

Why Your Credit Score is Costing You Cold, Hard Cash

Think of your credit score as your financial report card. When it’s low, lenders see you as a ‘high-risk’ student and charge you a fortune for the privilege of borrowing their money. We’re not talking about a few extra bucks; we’re talking about thousands of dollars leaking from your bank account over the years. It’s a hidden tax on having bad credit.

Let’s run the numbers so you can see the damage for yourself. Imagine you need a $20,000 car loan for 60 months. Look at how much extra you’d pay just because of your score:

| Credit Score Range | Typical APR | Monthly Payment | Total Interest Paid |

|---|---|---|---|

| Excellent (781-850) | ~4.5% | ~$373 | ~$2,380 |

| Good (661-780) | ~5.8% | ~$385 | ~$3,100 |

| Fair (601-660) | ~9.5% | ~$420 | ~$5,200 |

| Poor (300-600) | ~15.0%+ | ~$476 | ~$8,560+ |

Look at that difference! Someone with a poor score could pay over $6,000 more in interest than someone with an excellent score for the exact same car. That’s $6,000 you could have invested, saved for a down payment, or used to pay off other debt. This isn’t just about getting approved; it’s about stopping the financial bleed. Improving your score is one of the highest-return investments you can make in yourself.

The Underdog Weapon: What is a Secured Card, Really?

Alright, let’s clear the air. A secured card sounds intimidating, but it’s dead simple. It’s a credit card that you ‘secure’ with your own money. You give the bank a refundable security deposit, and that amount usually becomes your credit limit. If you deposit $300, you get a $300 credit limit. Simple as that.

This isn’t a prepaid card or a debit card. It’s a real credit card. Here’s why that matters:

- It Reports to Credit Bureaus: This is the whole point. The bank reports your payments to the big three credit bureaus (Equifax, Experian, and TransUnion). Positive payment history is the single biggest factor in your credit score.

- Your Deposit is Refundable: This isn’t a fee. It’s your money held as collateral. When you use the card responsibly and eventually close it or upgrade it, you get your deposit back.

- It’s an Entry Point: Banks are hesitant to lend to people with no credit or bad credit. The secured card removes their risk. You’re using your own money as a safety net, which gives them the confidence to give you a line of credit and report your good behavior.

Myth Buster: A secured card does NOT look bad on your credit report. To anyone looking at your report, it just looks like a regular credit card. There’s no special mark that screams ‘This person has bad credit!’ It’s your secret weapon.

The Game Plan: Your Step-by-Step Secured Card Strategy

Getting a secured card is easy. Using it to actually build your score takes a strategy. Don’t just get the card and hope for the best. Follow this game plan to the letter, and you’ll see results.

- Shop for the Right Card: Don’t just grab the first offer you see. Look for a card with no annual fee or a very low one. Also, critically, confirm that the card reports to all three major credit bureaus. Some only report to one or two, which limits your progress. Major banks like Discover and Capital One often have highly-rated secured card options.

- Make Your Deposit: Most secured cards require a minimum deposit of around $200. If you can afford to deposit more, like $500, do it. A higher credit limit can make it easier to keep your credit utilization low, which we’ll cover next. Remember, this is your money; you’ll get it back.

- Use It for a Small, Regular Purchase: This is the key. Do NOT max out the card. The goal isn’t to go shopping; the goal is to build a payment history. Pick one small, recurring bill—like your Netflix subscription ($15.49) or your Spotify plan ($10.99)—and put it on the card. That’s it. Then, put the physical card away in a drawer so you’re not tempted to use it for anything else.

- Set Up Autopay for the FULL Statement Balance: This is non-negotiable. A single late payment can wreck your progress. Log in to your new card’s online portal and set up automatic payments to pay the full statement balance every single month. Not the minimum payment. The full balance. This ensures you never miss a payment and never pay a dime in interest.

- Monitor Your Progress: Sign up for a free credit monitoring service like Credit Karma or use the free tools provided by your credit card company. Watch your score climb every few months. This will keep you motivated and show you that the plan is working.

The Rules of the Hustle: How to Maximize Your Score Boost

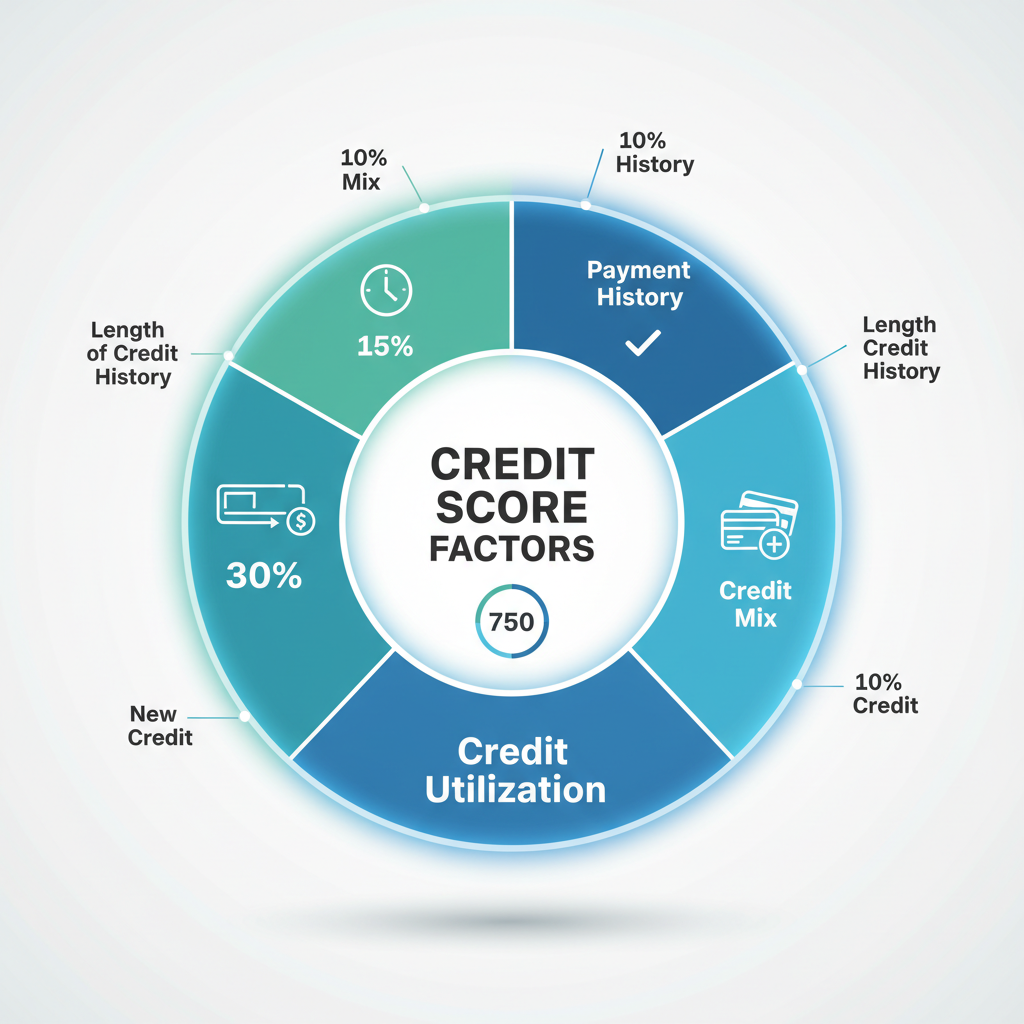

Just having the card and paying it isn’t enough to get the fastest results. You need to understand the rules of the game you’re playing. The second biggest factor in your credit score, after payment history, is something called Credit Utilization Ratio (CUR).

In plain English, it’s how much of your available credit you’re using. If you have a $300 limit and a $150 balance, your CUR is 50%. Lenders see high utilization as a red flag that you’re overextended.

The Golden Rule: Keep your balance below 30% of your limit at all times. The real pros? They keep it under 10%.

Let’s do the math. On a card with a $300 limit:

- 30% Utilization: A balance of $90

- 10% Utilization: A balance of $30

This is why the ‘one small subscription’ strategy is so powerful. If you put your $15.49 Netflix bill on a $300 limit card, your utilization is just over 5%. That’s an A+ in the credit score game. It tells the bureaus that you have access to credit but you’re disciplined and don’t need to use it all. It’s a massive trust signal that will supercharge your score’s growth.

Combine a perfect on-time payment history with an ultra-low credit utilization ratio, and you’ve created the perfect recipe for a rapid score increase. You’re not just fixing mistakes; you’re actively building a stellar new record from the ground up.

The Endgame: Graduating and Getting Your Deposit Back

This isn’t a life sentence. The secured card is your training ground. After about 6 to 12 months of perfect payment history and low utilization, something amazing starts to happen. Your credit score will have likely increased significantly. At this point, two things can happen.

Automatic Upgrade

Many banks (especially the good ones you chose in step one) will automatically review your account. If they see you’ve been a responsible user, they will ‘graduate’ you to one of their standard, unsecured credit cards. They’ll send you a letter, mail you a new card, and—best of all—they’ll refund your original security deposit right back to you. You’ve proven yourself, and now you’re playing in the big leagues with a real, unsecured line of credit.

Requesting an Upgrade

If your bank doesn’t automatically upgrade you after a year, don’t be afraid to call the number on the back of your card and ask. Say something like, “Hi, I’ve had my secured card for 12 months and have a perfect payment history. I’d like to inquire about being upgraded to an unsecured card.” The worst they can say is no, but often, this is the nudge they need to review your account and give you the green light.

This is the ultimate win. You used your own money as leverage to fix your credit, and now you get your money back *plus* a better score and a new, unsecured card. You’ve successfully hacked the system to work for you.

Conclusion

Your credit score doesn’t have to be a source of stress. It’s just a number, and you have the power to change it. A secured card isn’t a penalty box; it’s the most effective training tool available for building a rock-solid credit history. By following this strategic game plan—using the card for small purchases, paying it off in full every month, and keeping your utilization absurdly low—you’re not just building credit; you’re building a foundation for wealth. You’re unlocking lower interest rates, better opportunities, and the financial freedom you deserve. Stop letting your past dictate your future. Grab your secret weapon, execute the plan, and take back control of your money.

Disclaimer: I am not a financial advisor, and this article is for informational and educational purposes only. The information provided does not constitute financial advice. Please consult with a qualified professional before making any financial decisions.