Teach Kids Money Smart: The Ultimate Allowance & Chore Chart By Age

Let’s get real. Most of us learned about money the hard way—through overdraft fees, crippling student loans, or that soul-crushing feeling of living paycheck to paycheck. We were thrown into the deep end without a life jacket. But it doesn’t have to be that way for our kids. You have the power to break the cycle of financial illiteracy, and it starts way earlier than you think. It starts with chores and an allowance.

Forget thinking of it as just paying your kid to take out the trash. This is their first-ever ‘job.’ It’s their introduction to the earn-save-spend ecosystem. It’s a hands-on masterclass in budgeting, goal-setting, and understanding the value of a dollar. This guide is your battle plan. We’re cutting through the fluff to give you a straight-up, age-by-age strategy to turn your kids into money-savvy individuals who won’t get played by the system. Let’s build their financial backbone, one chore at a time.

The Foundation: Why an Allowance Isn’t a Handout

First things first, we need to kill the idea that an allowance is just free money. It’s not a welfare check for being cute. An allowance, when tied to effort, is a paycheck. It’s the most powerful financial teaching tool you have in your parenting arsenal. It’s the safe space for your kids to make $5 mistakes instead of $5,000 mistakes later in life.

Here’s the core philosophy: Money is earned, not given. By linking cash to chores, you’re hardwiring a fundamental life lesson: effort creates value. This system teaches them:

- Work Ethic: They learn that if they don’t work, they don’t get paid. Simple as that. This is the bedrock of every side hustle and career they’ll ever have.

- Budgeting Basics: With a finite amount of cash each week, they’re forced to make choices. Do they buy the candy bar now or save up for that video game? This is budgeting in its purest form.

- Delayed Gratification: In a world of instant downloads and next-day shipping, learning to wait for something you want is a superpower. Saving their allowance for a bigger goal builds that muscle.

- Financial Independence: They stop seeing you as a human ATM. When they ask for something at the store, the conversation shifts from ‘Can you buy me this?’ to ‘Do I have enough of my own money for this?’ That shift is a massive win.

Think of it as a financial sandbox. They get to play, experiment, and even mess up with money in a low-stakes environment where the only thing they can lose is a week’s worth of allowance, not their credit score.

The Game Plan: Age-by-Age Chore & Allowance Chart

There’s no one-size-fits-all answer for allowances, but there are smart guidelines. The goal is to make the chores and the pay age-appropriate. You don’t ask a 5-year-old to mow the lawn, and you don’t pay a 15-year-old $1 for making their bed. Here’s a realistic breakdown to get you started.

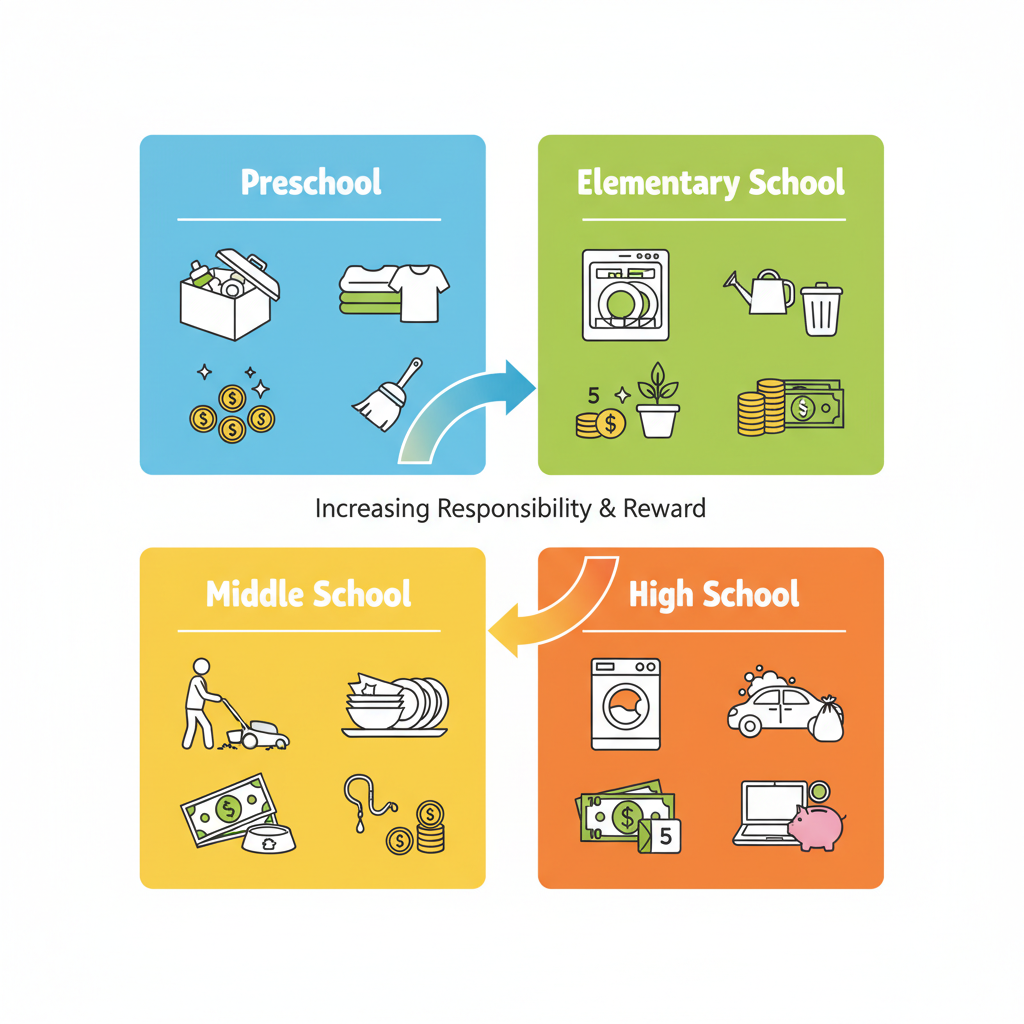

Ages 4-6: The Little Apprentices

At this age, it’s all about introducing the concept of ‘helping’ and getting a small reward. Keep it simple and visual. Their ‘job’ is to be a contributing member of the family team.

| Chore Example | Financial Skill Learned | Suggested Weekly Pay |

|---|---|---|

| Putting away their own toys | Responsibility for belongings | $1.00 – $3.00 |

| Placing their plate in the sink | Cleaning up after oneself | (Part of the base pay) |

| Helping to feed a pet | Caring for others | (Part of the base pay) |

Ages 7-10: The Junior Associates

They can handle more responsibility now. The chores become less about just their own stuff and more about contributing to the household. This is the prime time to introduce the ‘Three Jar’ system (more on that next).

| Chore Example | Financial Skill Learned | Suggested Weekly Pay |

|---|---|---|

| Making their own bed daily | Daily routine & discipline | $5.00 – $10.00 |

| Emptying small trash cans | Household contribution | (Part of the base pay) |

| Setting or clearing the dinner table | Teamwork | (Part of the base pay) |

| Watering plants | Consistency and care | (Part of the base pay) |

Ages 11-13: The Senior Staff

Middle schoolers are ready for more complex tasks and a bigger paycheck, which means bigger decisions. They can start managing their own ‘discretionary’ spending, like money for movies with friends or a new phone case.

| Chore Example | Financial Skill Learned | Suggested Weekly Pay |

|---|---|---|

| Taking out the trash and recycling bins | Managing a weekly task | $10.00 – $15.00 |

| Loading/unloading the dishwasher | Operating household machinery | (Part of the base pay) |

| Helping with meal prep (e.g., washing vegetables) | Life skills | (Part of the base pay) |

| Walking the dog | Responsibility for a living being | (Part of the base pay) |

Ages 14+: The Managers-in-Training

Teens need to be learning real-world money management. Their allowance should cover more of their personal expenses, like clothes, social outings, and gas money. This is where you can transition from a flat ‘allowance’ to a ‘commission’ model for bigger, one-off jobs.

| Chore Example | Financial Skill Learned | Suggested Pay Model |

|---|---|---|

| Doing their own laundry | Self-sufficiency | Part of being in the household |

| Mowing the lawn / Shoveling snow | Major project management | Pay per job (e.g., $20) |

| Babysitting younger siblings | Entrepreneurship | Pay per hour (e.g., $10/hr) |

| Cooking one family meal per week | Budgeting & planning | Give them the grocery budget |

The System: Implement the ‘Spend, Save, Give’ Method

Okay, your kid has earned their cash. Now what? If you just let them blow it all on candy and toys, you’re missing the biggest teaching opportunity. Enter the simplest, most effective budgeting system for kids: the Three Jar Method. It’s visual, tangible, and ridiculously easy to implement.

You’ll need three clear jars or envelopes. Label them:

- SPEND: This is their fun money. They can use it for small, immediate wants like a comic book, ice cream, or a toy. This teaches them how to handle cash and make purchasing decisions.

- SAVE: This is for bigger goals. That $60 video game or those $100 sneakers. They have to put money in this jar consistently to reach their goal. This is the ultimate lesson in delayed gratification and goal setting.

- GIVE: This teaches them that money isn’t just for them. It can be used to help others. They can save up to donate to a local animal shelter, buy a toy for a holiday drive, or give to a cause they care about. This builds empathy and perspective.

The Math in Action

Let’s say your 10-year-old, Maya, earns $10 a week. You both agree on a percentage split. A common one is 50% Spend, 40% Save, 10% Give.

- Spend Jar: Gets $5. She can use this for her weekly wants.

- Save Jar: Gets $4. She wants a new LEGO set that costs $80. She can now calculate that it will take her 20 weeks to save for it ($80 / $4 per week). This is a powerful, real-world math problem.

- Give Jar: Gets $1. After a couple of months, she’ll have enough to buy a bag of dog food to donate to the local shelter.

This system removes you from the equation. The jars—the system—become the authority. It’s not you saying ‘no’ to a toy; it’s the Spend jar being empty that says ‘no.’ This is a critical step in building financial autonomy.

Level Up: Advanced Money Skills for Teens

Once they’ve mastered the basics, it’s time to introduce more advanced concepts. The goal for your teenager isn’t just to manage a $20 allowance; it’s to prepare them for managing a $40,000 salary.

Transition to Digital

The jars are great, but the world runs on digital money. Open a joint checking or savings account with a debit card for your teen. This allows them to:

- Practice with a Debit Card: They learn to swipe, track their balance online, and understand that it’s not ‘magic money.’

- Learn About Interest: Open a high-yield savings account. Even if it’s just a few dollars a year, seeing their money make money is the best introduction to the magic of compound interest. Show them the math: A $500 savings at 4% interest earns $20 in a year for doing nothing.

- Use Budgeting Apps: Introduce them to simple, free apps like Mint or Goodbudget so they can track their spending digitally.

From Allowance to ‘Real World’ Budgeting

Instead of a weekly allowance, consider giving them a monthly budget for their key expenses. For example, give them $150 a month that has to cover their clothes, social life, and phone bill. If they blow it all in the first week, that’s a tough but invaluable lesson. They learn to plan and prioritize when the stakes are still relatively low.

Encourage the Side Hustle

This is where the real magic happens. Help them brainstorm ways to earn money outside of their regular chores. This could be mowing lawns, pet sitting, selling crafts on Etsy, or tutoring younger kids. This teaches them entrepreneurship, negotiation, and marketing. They learn that their earning potential isn’t capped by you; it’s capped by their own effort and ingenuity.

Scam Warning: The ‘Teen Influencer’ Trap

Be extremely wary of any ‘opportunity’ that requires your teen to buy a starter kit or pay for inventory to sell products (often seen in multi-level marketing). Real jobs and side hustles pay you; they don’t require you to pay them. Teach them to spot these predatory schemes that often target young, ambitious people.

Conclusion

Look, teaching your kids about money isn’t a one-time conversation. It’s a series of ongoing lessons that start with sorting toys and end with them opening their first retirement account. By implementing a clear, consistent allowance and chore system, you’re not just getting a cleaner house—you’re building a financially capable adult. You’re giving them the confidence to negotiate their first salary, the wisdom to avoid crippling debt, and the skills to build a life on their own terms.

This isn’t about raising penny-pinchers. It’s about raising smart, empowered individuals who understand that money is a tool. A tool they can use to build the life they want, support the people they love, and have a positive impact on the world. So start today. Grab those jars, make that chart, and give your kid the financial head start you wish you had. You’re not just their parent; you’re their first and most important financial advisor.