Safe Savings: How to Build a CD Ladder for Guaranteed Returns

Let’s be real: watching the stock market rollercoaster or seeing crypto bros lose their shirts can be terrifying. You work hard for your money, and the last thing you want is to gamble it away. Meanwhile, your standard savings account is probably earning you enough interest to buy a pack of gum… maybe. It feels like a rigged game. You want your money to grow, but you need it to be safe. You need a guaranteed win.

Enter the CD ladder. This isn’t some new, complicated financial product. It’s an old-school, time-tested strategy that smart money managers use to get the best of both worlds: the safety and high interest rates of a Certificate of Deposit (CD) combined with the flexibility of keeping your cash accessible. It’s about taking control, playing the system to your advantage, and building a foundation of wealth that nobody can touch. Forget the hype and the risk; it’s time to learn the blueprint for secure, predictable growth.

What the Heck is a CD Ladder and Why Should You Care?

Alright, let’s break this down. No confusing Wall Street jargon here. A Certificate of Deposit (CD) is basically a savings account with a commitment. You agree to leave your money with a bank for a set amount of time (the ‘term’), which could be anything from three months to five years. In exchange for that commitment, the bank gives you a much higher, fixed interest rate than a regular savings account. The catch? If you pull your money out early, you get hit with a penalty.

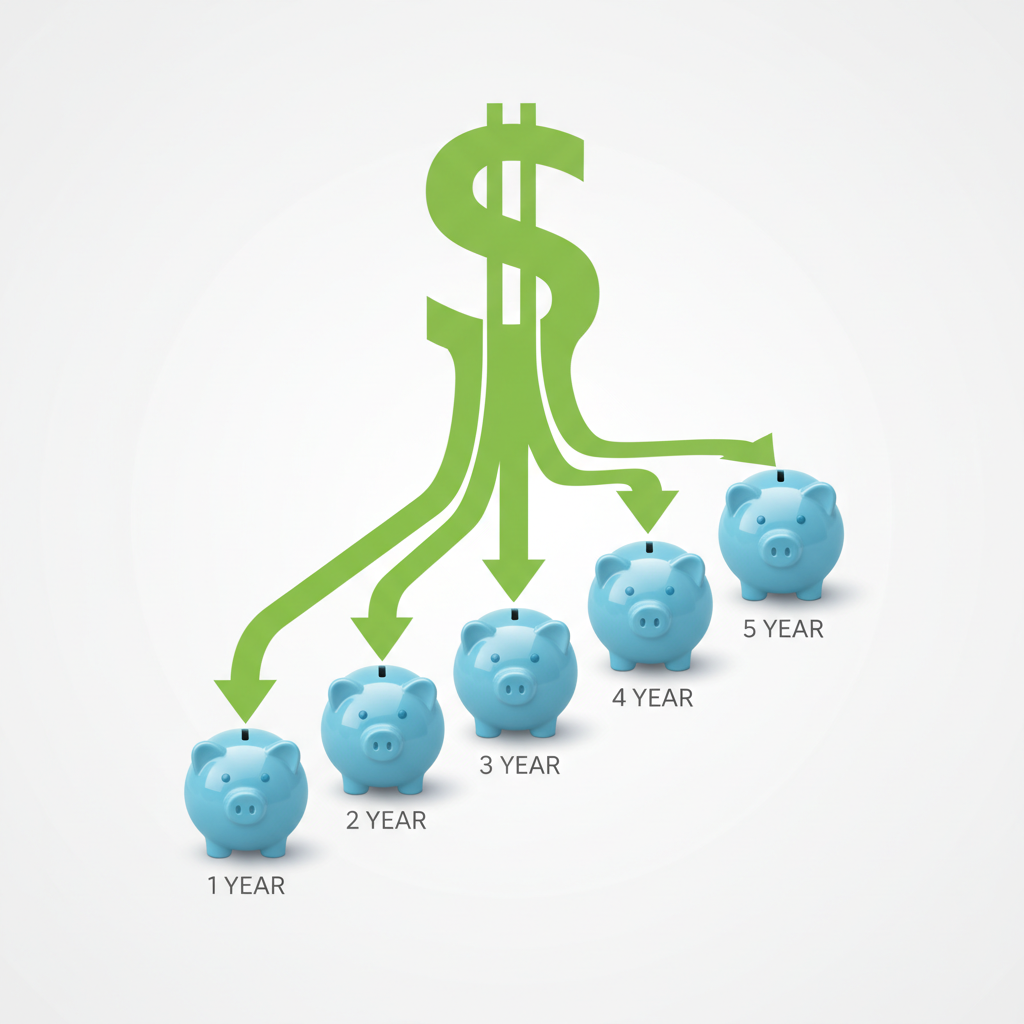

So, where does the ‘ladder’ come in? Instead of dumping all your cash into one big, long-term CD and locking it away for years, you get strategic. A CD ladder means you split your investment into several smaller CDs with different maturity dates. Think of it like climbing a ladder, one rung at a time.

For example, instead of putting $10,000 into a single 5-year CD, you could build a 5-rung ladder:

- $2,000 in a 1-year CD

- $2,000 in a 2-year CD

- $2,000 in a 3-year CD

- $2,000 in a 4-year CD

- $2,000 in a 5-year CD

Now, every single year, one of your CDs ‘matures,’ giving you access to your cash plus the interest you earned. This is the genius of the system. You get the high rates of long-term CDs, but a portion of your money becomes available every year. This strategy solves two huge problems:

- Liquidity: You’re not totally cash-strapped. If an emergency happens or a great opportunity comes up, you know you have money becoming available soon without paying a penalty.

- Interest Rate Risk: If interest rates go up, you’re not stuck with a low rate for five years. As each ‘rung’ of your ladder matures, you can reinvest that money into a new CD at the current, higher rate. You’re constantly capturing the best available deals.

Bottom line: A CD ladder is your tool for earning guaranteed returns that crush a traditional savings account, all while keeping your money safe (it’s FDIC insured up to $250,000 per depositor, per bank) and reasonably accessible.

The Math: How a CD Ladder Crushes Your Savings Account

Talk is cheap. Let’s run the numbers and see exactly how a CD ladder puts more money in your pocket. We’ll use a realistic example with $15,000 you want to save. We’ll compare three options over three years, using hypothetical (but typical) interest rates.

The Contenders:

- Option A: High-Yield Savings Account (HYSA): Flexible, but rates can change. Let’s say it averages 4.00% APY.

- Option B: Single 1-Year CD: You put all $15,000 in a 1-year CD at 5.00% APY and renew it each year.

- Option C: The 3-Year CD Ladder: You split the $15,000 into three CDs: $5,000 in a 1-year CD (5.00% APY), $5,000 in a 2-year CD (4.75% APY), and $5,000 in a 3-year CD (4.50% APY). As the 1-year CD matures, you reinvest it in a new 3-year CD.

Here’s how the earnings stack up. We’re assuming for the ladder example that when the 1-year CD matures, you can get a new 3-year CD at 4.50%.

| Strategy | Year 1 Earnings | Year 2 Earnings | Year 3 Earnings | Total Interest Earned |

|---|---|---|---|---|

| HYSA (4.00%) | $600 | $624 (compounded) | $649 (compounded) | ~$1,873 |

| Single 1-Year CD (5.00%) | $750 | $788 (compounded) | $827 (compounded) | ~$2,365 |

| 3-Year CD Ladder | ~$708 | ~$745 (compounded) | ~$780 (compounded) | ~$2,233+ (plus flexibility) |

Wait, the numbers look close, so what’s the big deal? The magic of the ladder isn’t just about the first few years, it’s about the long-term structure. After Year 1, you reinvest your first matured $5,000 into a new 3-year CD, likely at a higher rate than the 1-year. By Year 3, your entire ladder consists of higher-yield 3-year CDs, but one is still maturing every single year. You’ve locked in the best rates while creating annual liquidity. The HYSA rate could drop at any time, but your CD rates are guaranteed for their term. You’ve built a powerful, predictable cash flow machine that out-earns simple savings strategies over time, especially in a stable or rising interest rate environment.

The Blueprint: Building Your First CD Ladder, Step-by-Step

Ready to build this thing? It’s easier than you think. No special broker needed. Just you, an internet connection, and a plan. Here’s the exact blueprint to follow.

-

Step 1: Assess Your Cash Stash

First, figure out how much money you can realistically lock away. This should NOT be your emergency fund. This is money for a medium-term goal, like a down payment in 3-5 years, or just cash you want to grow safely without touching it. Be honest with yourself. How much can you commit?

-

Step 2: Hunt for the Best Rates

Don’t just walk into your local brick-and-mortar bank. Their rates are usually terrible. The real money is at online banks and credit unions. They have less overhead and pass the savings to you with higher APYs. Use rate comparison websites like Bankrate or NerdWallet to see who is offering the best deals today. Check out well-regarded online banks like Ally Bank, Marcus by Goldman Sachs, or Discover Bank.

-

Step 3: Decide on Your Ladder’s ‘Rungs’

How many CDs do you want and what terms? A simple and effective ladder for beginners is a 3- or 5-year ladder. For a 3-year ladder, you’d get a 1-year, 2-year, and 3-year CD. For a 5-year ladder, you’d get a 1-year, 2-year, 3-year, 4-year, and 5-year CD. The longer the ladder, the higher your potential average interest rate, but the longer it takes for the whole system to be cycling at the highest rate.

-

Step 4: Open and Fund the Accounts

Once you’ve chosen your bank(s) and your ladder structure, it’s time to execute. You’ll open each CD account online. Take your total investment amount (e.g., $10,000) and divide it evenly across your rungs (e.g., $2,000 into each of five CDs). The application process is usually quick, just like opening a savings account.

-

Step 5: Manage Your Maturities

This is the key to making the ladder work long-term. When your first, shortest-term CD matures (e.g., after one year), the bank will notify you. You have a choice: cash it out or reinvest it. To keep the ladder going and maximize returns, you’ll take that matured principal and interest and roll it into a new CD at the longest term on your ladder. So, your 1-year CD money now becomes a new 5-year CD. One year later, your original 2-year CD matures, and you do the same thing. Soon, you’ll have a ladder of all long-term, high-yield CDs, with one maturing every single year. You’ve built a money machine.

Pro-Tips & Traps to Avoid

Building a CD ladder is straightforward, but the street-smart saver knows the angles and avoids the pitfalls. Here’s what you need to watch out for.

Pro-Tip: Be a Rate Chaser

When a CD matures, don’t just let it automatically renew at whatever rate your current bank offers. That’s leaving money on the table. Your ‘grace period’ (usually 7-10 days after maturity) is your window to shop around again. If another FDIC-insured bank is offering a significantly better rate for the term you want, move your money. Loyalty doesn’t pay in the savings game; high rates do.

Pro-Tip: Consider No-Penalty CDs

Feeling a little nervous about locking up your money? Look into ‘no-penalty’ or ‘liquid’ CDs. These allow you to withdraw your entire balance and interest earned before the maturity date without paying a fee (usually after the first week). The trade-off? The interest rate is typically a bit lower than a standard CD of the same term. It’s a great option if you think you might need the cash but want to earn more than a HYSA.

Trap to Avoid: The Early Withdrawal Penalty

This is the big one. If you pull money from a standard CD before its maturity date, you will pay a penalty, which is usually a set number of months’ worth of interest. Know the penalty before you open the account.

Key Rule: Treat your CD money like it’s in a vault with a time lock. Do not commit funds you might need for emergencies. That’s what your separate, liquid emergency fund is for.

Trap to Avoid: Ignoring Inflation

Let’s be clear: a CD is a tool for capital preservation and guaranteed growth. It is not designed to generate the high returns needed to consistently crush inflation year after year like stocks might (with much higher risk). In times of high inflation, the ‘real return’ on your CD (the interest rate minus the inflation rate) might be low or even negative. However, it’s still protecting your principal and guaranteeing a return, which is far better than letting cash sit and lose value without earning anything.

Trap to Avoid: ‘Callable’ CDs

You might see these offered with a super attractive interest rate. A ‘callable’ CD means the bank has the right to ‘call’ it back—to close it and give you your money back before the maturity date. Why would they do this? If interest rates fall, they don’t want to be stuck paying you a high rate. They’ll call the CD back, and you’ll be forced to reinvest your money at the new, lower rates. For beginners, it’s best to stick with standard, non-callable CDs to ensure your rate is truly locked in.

Conclusion

Building a CD ladder isn’t about getting rich quick. It’s about getting rich smart. It’s a power move for anyone who wants to see their savings grow without the anxiety of market speculation. By laddering, you create a stable, predictable system that provides higher, guaranteed returns than a savings account, while still giving you regular access to your funds. You get the best of both worlds: safety and opportunity.

You now have the blueprint. You understand the math, the steps, and the traps to avoid. The next step is to take action. Start small if you need to, but start. Build your first rung. In a year, when that first CD matures and you see that guaranteed interest payment, you’ll understand the power of this strategy. You’re not just saving money; you’re building a secure financial future, one rung at a time.

Disclaimer: I am not a financial advisor. The information provided in this article is for informational and educational purposes only. It is not intended to be a substitute for professional financial advice. You should consult with a qualified financial professional before making any investment decisions.