How To Survive Living Alone On Minimum Wage (Real Numbers)

Let’s cut the crap. Living alone on minimum wage is a street fight. The federal minimum wage is stuck at a measly $7.25 an hour. Before taxes, that’s about $1,256 a month. After Uncle Sam takes his cut, you’re lucky to see $1,000. Anyone telling you to just ‘cut back on lattes’ is living in a fantasy world. They don’t get it. But I do.

This isn’t a guide about deprivation. This is a guide about power. It’s about taking the garbage hand you’ve been dealt and playing it so smart that you not only survive, you start building a way out. We’re going to use real numbers, ruthless strategy, and a little bit of hustle to turn your financial situation from a source of stress into a source of strength. Forget ‘thriving’ for a second—let’s master the art of survival first. Let’s get to work.

The Brutal Math: Facing Your Real Numbers

First rule of the fight: know your enemy. Your enemy is your budget, or the lack of one. You can’t win if you’re flying blind. We need to put every single dollar on trial. Let’s assume a post-tax monthly income of $1,068 (based on $7.25/hr at 40 hours/week, after an estimated 15% tax). Here’s what the battlefield looks like for most people:

| Category | Average Cost | % of Income | Your Notes |

|---|---|---|---|

| Income (After Tax) | +$1,068 | 100% | |

| Median Rent (Studio/1BR) | -$950 | 89% | This is the budget killer. |

| Utilities (Electric, Water, Gas) | -$150 | 14% | Non-negotiable, but can be reduced. |

| Basic Groceries | -$250 | 23% | This is for bare-bones eating. |

| Transportation (Public) | -$60 | 6% | Assuming no car. |

| Phone/Internet | -$100 | 9% | Essential for work/life. |

| Total Expenses | -$1,510 | 141% | |

| Monthly Deficit | -$442 | -41% | This is the problem. |

Look at that table. The numbers don’t lie. Based on national averages, you’re starting the month $442 in the hole. This isn’t your fault; it’s a systemic failure. But crying about it won’t pay the rent. This deficit is the dragon we have to slay. The rest of this guide is about how we do it, systematically and ruthlessly.

The ‘Big 3’ Takedown: Slashing Housing, Transport, and Food

Over 70% of your money is devoured by three things: where you live, how you get around, and what you eat. Forget clipping coupons for toothpaste until you’ve taken a sledgehammer to these giants. This is where the real money is saved.

Housing Hacks: Your Biggest Expense is Your Biggest Opportunity

That $950 rent is an anchor. Your number one mission is to shrink it. ‘Living alone’ might have to mean ‘without family or a significant other,’ not ‘without another person helping pay bills.’ Consider these non-negotiable options:

- Get a Roommate: This is the fastest way to cut your biggest bill in half. Finding a reliable person is key. Screen them like you’re hiring an employee.

- Rent a Room: Cheaper than an apartment, renting a room in a larger house can slash your housing cost by 60% or more.

- Relocate (If Possible): Look at neighborhoods further from the city center or consider moving to a lower cost-of-living area if your job allows. A 15-minute longer commute could save you $300/month.

Transportation Takedown: Ditch the Money Pit

If you have a car, you have a financial emergency. A car payment, insurance, gas, and maintenance is a luxury you cannot afford. The average cost of car ownership is over $800/month. Ditching it is like giving yourself a massive raise.

- Public Transit: A monthly pass is your new best friend. It’s a fixed, predictable cost.

- Bike or Walk: If you live close enough to work, this is a $0 transportation cost that also keeps you healthy.

- Carpool/Rideshare: Use it only when absolutely necessary. It’s still cheaper than ownership.

The Math: Selling a car could eliminate a $300 payment, $150 in insurance, and $100 in gas. That’s $550 back in your pocket. Every. Single. Month. That’s $6,600 a year.

The Grocery Gauntlet: Fuel Yourself for Less

Your $250 grocery budget is tight, but it can be done. This is about strategy, not starvation.

- Shop the Perimeter: Stick to the outer edges of the grocery store where the whole foods are—produce, meat, dairy. Avoid the processed junk in the middle aisles.

- Discount Grocers: Aldi, Lidl, and other local discount chains are your new home. Their prices are significantly lower than traditional supermarkets.

- Meal Prep is Law: Spend Sunday afternoon cooking. Make a big batch of chili, rice and beans, or roasted chicken. This prevents you from buying expensive lunches or takeout when you’re tired.

| Meal Option | Cost Per Meal | Monthly Cost (Lunch Only) |

|---|---|---|

| Eating Out (Fast Food) | ~$10.00 | $300 |

| Meal Prepped (e.g., Chicken, Rice, Veggies) | ~$2.50 | $75 |

| Monthly Savings | $225 |

The Offensive Strategy: Your Side Hustle War Chest

Budgeting is defense. It stops the bleeding. Now it’s time to play offense. You MUST increase your income. An extra $300-500 a month completely changes the game. It erases your deficit and gives you breathing room. Don’t look for a passion project; look for the fastest path to cash with skills you already have or can learn quickly.

- Gig Work: Food delivery (DoorDash, Uber Eats) or grocery shopping (Instacart). You can work when you want and cash out daily. The key is to work peak hours to maximize earnings.

- Task-Based Gigs: Use apps like TaskRabbit for things like furniture assembly, mounting TVs, or running errands for people. You can set your own rates.

- Freelance from Your Couch: Got basic computer skills? Offer data entry, virtual assistant services, or transcription on sites like Upwork and Fiverr. The pay starts low, but you can build a reputation and increase your rates.

- Flip for Profit: Scour Facebook Marketplace and thrift stores for free or cheap items (furniture, electronics) that you can clean up and resell for a profit.

| Side Hustle | Time Investment | Realistic Earning Potential (Monthly) |

|---|---|---|

| Food Delivery (10-15 hrs/week) | Flexible | $300 – $600 |

| Freelance Data Entry (10 hrs/week) | Flexible | $200 – $400 |

| Pet Sitting / Dog Walking | Varies | $150 – $500+ |

Scam Warning: If a ‘job opportunity’ asks YOU to pay money upfront for a kit, for training, or for anything else, it is a SCAM. If it sounds too good to be true (‘Make $5,000 a week from home!’), it is a SCAM. Real jobs pay you; you do not pay them. Stick to reputable platforms like Upwork, Fiverr, Rover, and the major gig apps.

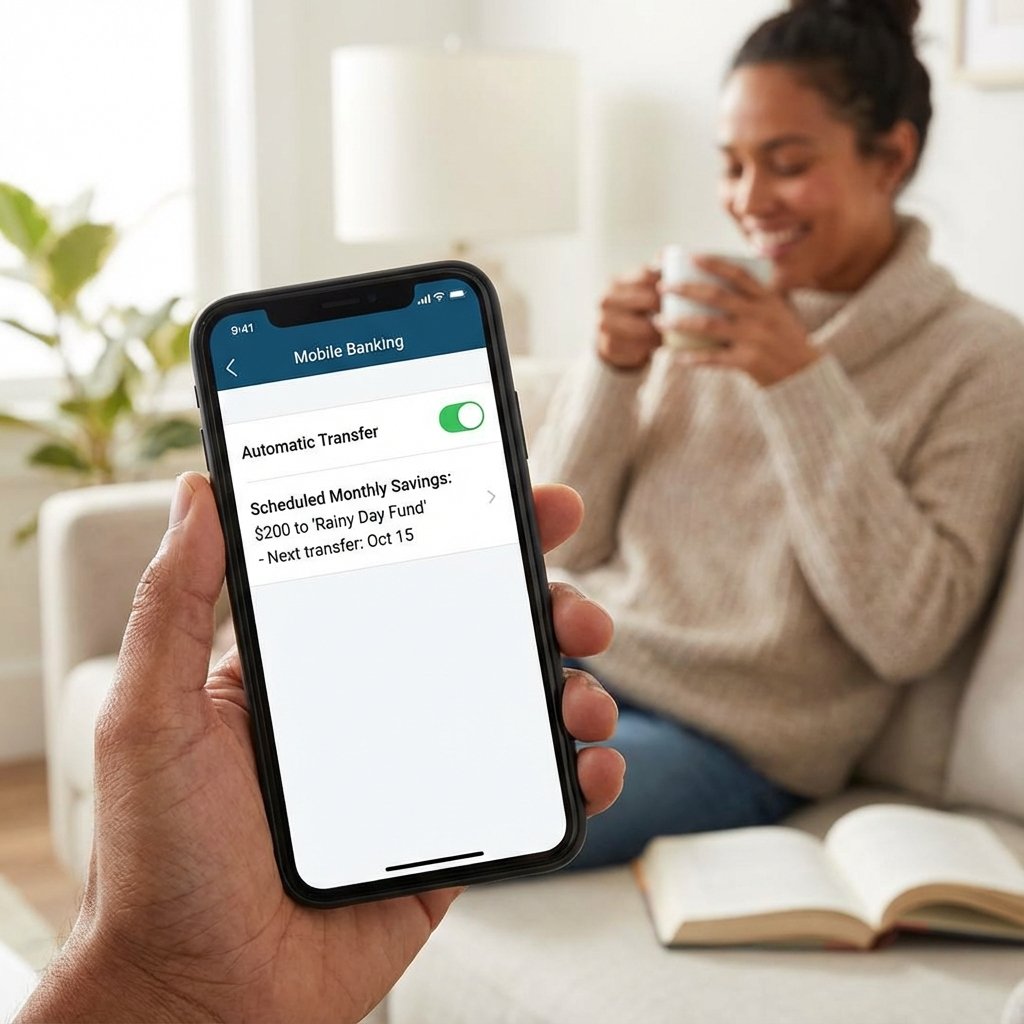

Automate Your Escape Plan: Building a ‘Freedom Fund’

When that first side hustle dollar comes in, it’s tempting to just use it to breathe. Don’t. Every extra dollar has a mission: to build your ‘Freedom Fund.’ This is a fancy name for a $1,000 emergency fund. This fund is your shield. It’s what keeps a flat tire or a medical bill from becoming a full-blown catastrophe that sends you into debt.

You must automate this process, or it won’t happen. Treat your savings like a bill you have to pay—to yourself.

- Open a High-Yield Savings Account (HYSA): Find an online bank that offers a HYSA. They are free and pay you more interest than a traditional bank. This account is ONLY for your Freedom Fund. Do not connect a debit card to it.

- Set Up Automatic Transfers: The moment your paycheck hits, set up an automatic transfer to your HYSA. Start small. $10 a week. $25 a week. Whatever you can. The amount is less important than the consistency.

- Direct Deposit Your Hustle: If you can, have your side hustle earnings deposited directly into your HYSA. You never even see the money in your checking account, so you’re not tempted to spend it.

The Power of Automation: Saving just $25 a week from your side hustle feels like nothing. But over a year, that’s $1,300. You’ve built your Freedom Fund and then some without even thinking about it. This is how you build a foundation. This is how you escape the paycheck-to-paycheck trap. It’s slow, but it’s real, and it works.

Conclusion

Surviving on minimum wage isn’t about being cheap; it’s about being a strategist. It’s a game of inches and a battle of wills. You now have the playbook. You know the brutal math, you have a plan to attack your biggest expenses, you know how to generate more cash, and you have a system to build your financial shield.

This isn’t easy. It requires discipline and sacrifice. But every dollar you save and every dollar you earn is a vote for your future. It’s a step away from financial anxiety and a step toward control. You are not your wage. You are your resourcefulness, your hustle, and your refusal to quit. Now stop reading and start doing. Take control of your money, and you take control of your life.