Drowning in Debt? Why the Snowball Method Is Your Only Way Out

Let’s be real. That feeling of being buried in debt is suffocating. It’s the pit in your stomach when you check your bank account, the stress that keeps you up at night, the constant voice whispering that you’ll never get ahead. Most of the advice out there is a slap in the face—complicated spreadsheets, jargon-filled lectures, and strategies that assume you’re a robot, not a human.

They tell you to follow the “smart” path, the one with the highest interest rates. But when you don’t see progress for months, you burn out, give up, and the cycle continues. It’s time to ditch the advice that makes you feel like a failure. It’s time for a new game plan.

Enter the Debt Snowball Method. This isn’t your accountant’s favorite strategy. This is a street-smart, psychological hack designed for real people. It’s not about complex math; it’s about momentum. It’s about landing quick, dirty, satisfying wins that build your confidence and turn you into an unstoppable debt-destroying machine. If you’re serious about getting out, this is your playbook.

The Game Plan: What is the Debt Snowball Method & Why It Actually Works

Forget everything you’ve heard about interest rates being the end-all, be-all. The number one reason people fail to get out of debt isn’t math—it’s burnout. The Debt Snowball Method is the antidote to financial fatigue.

Here’s the core concept, stripped of all the fluff:

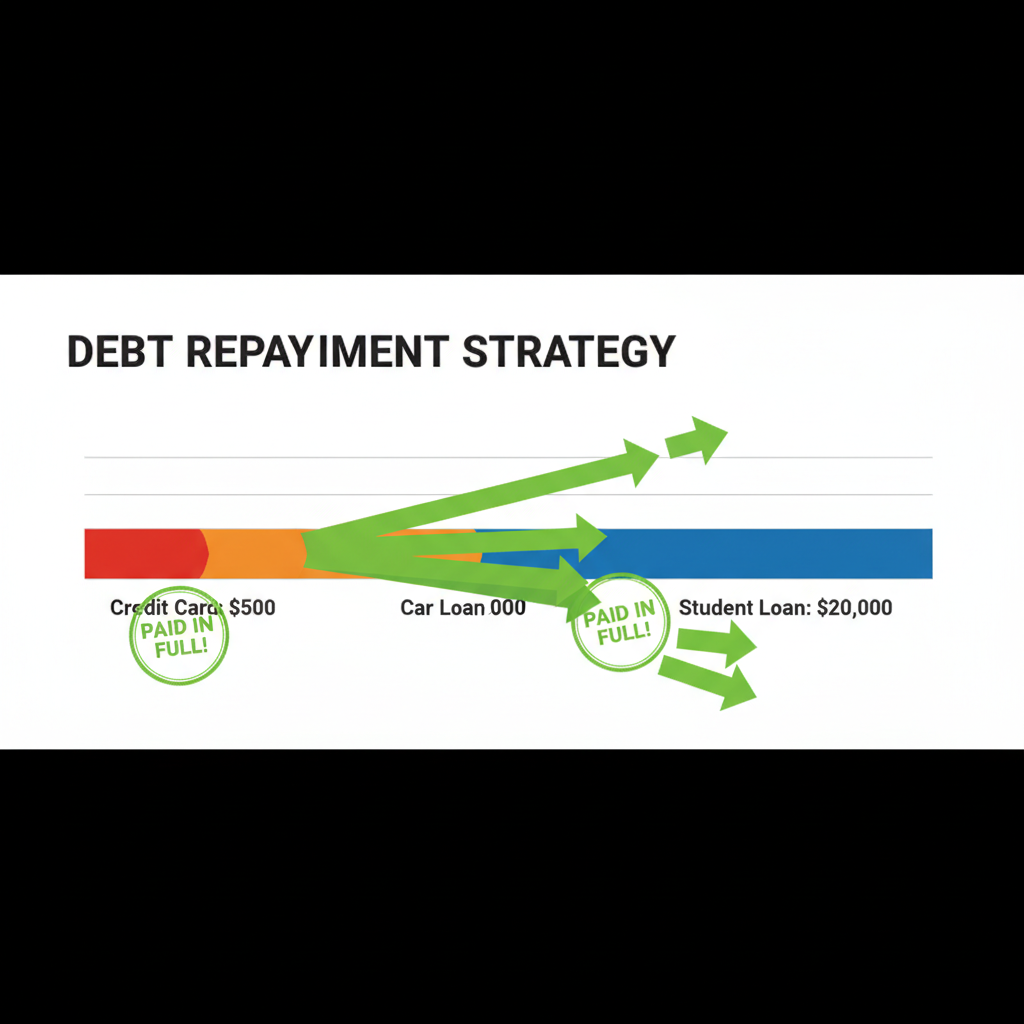

- Step 1: You list every single one of your debts (excluding your mortgage) from the smallest balance to the largest.

- Step 2: You make the minimum payment on ALL of your debts, just to keep them current.

- Step 3: You take every extra dime you can scrape together and throw it at the smallest debt on your list. You attack it with everything you’ve got.

- Step 4: Once that smallest debt is obliterated—gone forever—you take the money you were paying on it (the minimum payment PLUS all the extra cash) and you “roll it” onto the next-smallest debt.

That’s it. You repeat this process, and with each debt you eliminate, your “snowball” of cash gets bigger and bigger, rolling downhill faster and faster, wiping out the next debt even quicker.

Why This Crushes the ‘Smarter’ Debt Avalanche

The finance gurus will scream from the rooftops about the Debt Avalanche method, where you focus on the highest-interest-rate debt first. And yes, on paper, you’ll pay slightly less in total interest. But personal finance is 80% behavior and only 20% math. The Avalanche method is like starting a video game on the hardest level. You face the final boss first, and when you keep losing, you quit.

The Snowball method is the opposite. It’s a psychological masterpiece:

- It gives you quick wins. Knocking out that first small $500 credit card in a couple of months feels incredible. You get a shot of dopamine. You see progress. You feel like a winner.

- It builds momentum. That feeling of victory fuels you to keep going. You’re not just paying bills; you’re conquering enemies.

- It simplifies your life. With each debt paid off, you have one less bill to track, one less mental burden. Your financial life gets cleaner and easier to manage.

This isn’t just a budget plan; it’s a behavior-change engine. You’re not just paying off debt; you’re rewiring your brain to win with money.

The Takedown: Your 4-Step Launch Sequence

Alright, enough talk. It’s time to get your hands dirty. This is where you stop being a victim of your debt and start becoming the hunter. Follow these four steps exactly. No shortcuts.

-

Step 1: The Hit List (Face the Music)

You can’t fight an enemy you can’t see. Grab a piece of paper or open a spreadsheet and list every single debt you have, except for your primary mortgage. Be brutally honest. This is a no-judgment zone, but it requires radical honesty.

You need to list:

- Creditor Name: (e.g., Capital One, Honda Financial, Sallie Mae)

- Total Balance Owed: The exact amount down to the cent.

- Minimum Monthly Payment: The lowest amount you’re required to pay.

-

Step 2: Rank ‘Em (Set Your Targets)

Now, rewrite that list. But this time, order it from the smallest total balance to the largest total balance. That’s it. Ignore the interest rates. I don’t care if your $500 medical bill is at 0% interest and your $10,000 credit card is at 25%. The $500 bill is at the top of your hit list. This is your battle order. The smallest balance is your first target.

-

Step 3: Find Your Ammo (The Debt-Crushing Fund)

Your minimum payments are your defensive line. The extra money is your offense. You need to find more ammo. Your mission is to find at least an extra $100–$500 a month to throw at your debt. How? By getting ruthless with your budget.

- Cancel subscriptions: That gym you don’t use? Gone. The five streaming services? Pick one. Gone.

- Stop eating out: Packing your lunch and making coffee at home can easily save you $300+ a month.

- Sell stuff: Go through your garage, closets, and storage. That old bike, those video games, the clothes you never wear? That’s cash waiting to be deployed. List it on Facebook Marketplace or Poshmark tonight.

- Pick up a side hustle: Even 5-10 extra hours a week delivering for DoorDash or walking dogs with Rover can generate hundreds of dollars in pure debt-fighting ammo.

This extra money is not for fun. It has one purpose: to be aimed directly at the smallest debt on your list.

-

Step 4: Attack! (Execute the Plan)

This is where it all comes together. Set up automatic payments for the minimum amount on ALL debts *except* the smallest one. For the smallest debt, you will pay the minimum PLUS every single dollar from your Debt-Crushing Fund. If you found an extra $250, you pay the minimum + $250. If you sold an old TV for $150, that goes straight to the debt too. You don’t stop, you don’t pause, you don’t make excuses until that balance is zero.

The Math That Matters: Seeing the Snowball in Action

Let’s see how this works for a real person. Meet Alex. Alex is drowning. Here’s Alex’s debt hit list:

| Creditor | Total Balance | Minimum Payment |

|---|---|---|

| Store Credit Card | $750 | $35 |

| Personal Loan | $3,000 | $120 |

| Car Loan | $9,500 | $250 |

Alex did the hard work and squeezed an extra $200 out of the budget each month. This is the ammo. According to the Debt Snowball rules, Alex will attack the Store Credit Card first.

Month 1-3: The First Kill

Alex pays the minimums on the Personal Loan ($120) and the Car Loan ($250). For the Store Credit Card, Alex pays the minimum ($35) + the extra ammo ($200) for a total payment of $235. In just over 3 months, that $750 balance is GONE. Alex gets the first win. The psychological boost is massive. Alex proved it can be done.

Month 4 and Beyond: The Snowball Grows

Now, the magic happens. The Store Credit Card is history. Alex now takes the $235 that was going to that card and “rolls it” onto the next target: the Personal Loan.

The new payment on the Personal Loan is:

- Original Minimum Payment: $120

- Freed-up Snowball Payment: $235

- New Total Monthly Payment: $355

Look at that! Without finding any new money, Alex is now throwing $355 a month at the Personal Loan. What would have taken 2.5 years to pay off is now on track to be eliminated in under 9 months. Once that’s gone, the snowball gets even bigger.

| Target Debt | Initial Payment | Snowball Payment | Time to Obliterate |

|---|---|---|---|

| Store Credit Card ($750) | $35 + $200 extra | $235 | ~3 Months |

| Personal Loan ($3,000) | $120 + $235 snowball | $355 | ~8-9 Months |

| Car Loan ($9,500) | $250 + $355 snowball | $605 | ~16 Months |

By following this plan, Alex goes from being buried in payments for years to being completely debt-free (besides the mortgage) in just over 2.5 years. The math that matters isn’t the interest rate—it’s the speed and motivation you get from watching your debts fall one by one.

Level Up: How to Supercharge Your Snowball

Once your snowball is rolling, it’s time to pour gasoline on the fire. Your goal is to make that snowball bigger and faster. Here’s how you level up.

Find More Ammo: The Budget Squeeze

Your budget isn’t a prison; it’s a weapon. Every dollar you save is another soldier in your debt-free army. Use tools like YNAB (You Need A Budget) or Mint to track every penny. Then, get aggressive.

- The No-Spend Challenge: Try for one week, then two, then a whole month. You only spend money on absolute necessities (housing, utilities, basic groceries, gas to get to work). It’s a reset button for your spending habits and can free up hundreds of dollars.

- Negotiate Your Bills: Call your cell phone, internet, and insurance providers. Tell them you’re thinking of switching and ask for a better rate. A 15-minute phone call can save you $500+ a year.

- The Grocery Gauntlet: Plan your meals, stick to your list, use coupons, and never shop hungry. Ditching brand names for generics on most items can easily cut your grocery bill by 20-30%.

Earn More Ammo: The Side Hustle Playbook

The fastest way to accelerate your debt payoff is to increase your income. All extra income goes directly to the snowball. No exceptions.

Key Rule: Any money earned from a side hustle is not “your” money. It is your debt’s money. It goes straight to the smallest balance on your list.

Here are some no-excuse side hustles you can start this week:

Psychological Warfare: Staying in the Fight

This is a marathon, not a sprint. You need to keep your head in the game.

- Get Visual: Print out a debt-free thermometer or a chart. For every $100 you pay off, color in a section. Putting this on your fridge is a powerful daily reminder of your progress.

- Celebrate the Wins: When you kill off a debt, you MUST celebrate. But don’t go into debt to do it! Have a pizza night at home, go for a hike, take an afternoon off to do something you love. Anchor the victory with a positive (and free) reward.

- Find Your Community: Tell a trusted friend or family member about your goal. Or join online communities on Reddit (like r/personalfinance) where people share their wins and struggles. You’re not alone in this fight.

Conclusion

The Debt Snowball Method is more than a financial strategy—it’s a declaration of war on your debt. It’s you, finally taking control. The so-called experts can keep their complicated spreadsheets and their ‘mathematically optimal’ plans that nobody can stick to. We’re in the business of results, and the Snowball delivers because it’s built for humans.

It’s about momentum. It’s about tasting victory early and often. It’s about turning the soul-crushing weight of debt into a game you can actually win. Every small debt you eliminate is a boss battle you’ve conquered, making you stronger for the next one.

Stop drowning. Stop waiting for a miracle. The power is in your hands. List your debts, find your ammo, and start rolling that snowball today. Your freedom is waiting at the bottom of that hill.

Disclaimer: The content provided here is for informational purposes only and is not intended as financial, investment, or legal advice. I am not a financial advisor. Please consult with a licensed professional before making any financial decisions.