Debt Collectors Calling? Say These 5 Words To Make Them Stop

That feeling. The phone buzzes, you see an unknown number, and the pit in your stomach drops. Is it them again? Debt collectors have a way of making you feel powerless, cornered, and stressed out. They call at dinner, at work, on weekends—a relentless assault designed to wear you down until you pay up, whether you can afford to or not. But what if I told you the power isn’t all on their side? What if you had a secret weapon, a simple five-word phrase that could stop the calls cold? This isn’t a magic trick; it’s your legal right. The system is built to intimidate you, but the law has your back if you know how to use it. Forget the fear and the frustration. It’s time to flip the script. In this guide, we’re not just giving you a line to say; we’re handing you the keys to shut down the harassment, force collectors to play by the rules, and give you the breathing room you need to handle your finances your way. Get ready to take back your peace of mind.

Why They Call and Why You Have the Power

Why They Call and Why You Have the Power

First, let’s pull back the curtain on the debt collection game. It’s a business, plain and simple. When you fall behind on a bill—a credit card, a medical bill, a personal loan—the original creditor might try to collect for a while. If they’re unsuccessful, they often sell your debt to a third-party collection agency. And here’s the kicker: they sell it for pennies on the dollar. That $2,000 credit card debt? A collector might have bought it for as little as $80. Their entire business model is based on getting you to pay as much as possible over what they paid. That’s why they’re so aggressive—every dollar they squeeze out of you is almost pure profit.

They rely on a strategy of pressure, intimidation, and sometimes, outright confusion. They want you to feel flustered and scared, so you’ll make a rash decision, like paying a debt you don’t actually owe, or one that’s too old to be legally collected (more on that later). They’re counting on you not knowing your rights.

Meet Your Secret Weapon: The FDCPA

This is where you gain the upper hand. The U.S. government passed a law back in the 70s called the Fair Debt Collection Practices Act (FDCPA). This is your shield. This law was specifically created to protect consumers like you from abusive, unfair, or deceptive debt collection practices. It sets the rules of the game, and if collectors break them, they can get in serious trouble.

The FDCPA gives you a ton of rights, including:

- The right to not be harassed or abused.

- The right to not be lied to or deceived.

- The right to control how and when collectors contact you.

- And most importantly for our purpose: The right to dispute the debt and demand proof that you owe it.

This last one is the key. You don’t have to take their word for it. The burden of proof is on them, not you. Understanding this simple fact is the first step to shifting the power dynamic from them to you. They aren’t your boss; they’re a company trying to make a profit, and you have the legal right to make them prove their claim.

The 5 Magic Words: ‘Prove This Debt Is Mine’

The 5 Magic Words: ‘Prove This Debt Is Mine’

Okay, here it is. The simple, powerful phrase that stops collectors in their tracks. When a debt collector calls, and after they’ve identified themselves and the reason for their call, you need to say this calmly and clearly:

‘Please send me proof of this debt in writing.’

You can also say, ‘I am disputing this debt. Prove it is mine.’ Both phrases trigger the same legal mechanism. Let’s break down why this is so effective. When you say these words, you are formally invoking your rights under the FDCPA. You are not arguing. You are not explaining your financial situation. You are not making promises. You are giving them a legal directive. Once you do this, they are legally required to stop all collection efforts—including phone calls—until they have sent you verification of the debt.

What ‘Debt Validation’ Actually Means

This isn’t just a stalling tactic; it’s a formal legal process. ‘Proof’ or ‘validation’ isn’t just a scribbled note saying ‘You owe us money.’ Under the law, they must provide you with specific information, which typically includes:

- The amount of the debt.

- The name of the creditor to whom the debt is currently owed.

- Information that allows you to identify the original transaction (like an account number).

- A statement informing you of your right to dispute the debt within 30 days.

li>The name of the original creditor (if different).

This process is powerful for several reasons. First, it gets them off the phone immediately. Second, it forces them to do paperwork, which costs them time and money. Third, and most importantly, sometimes they can’t even find the proof! Remember, they bought your debt in a large bundle with thousands of others. The original paperwork can be messy, lost, or incomplete. If they can’t provide the legal validation, they cannot legally continue to try and collect the debt from you. It essentially makes the debt uncollectible by them.

The Full Script: How to Say It and What to Do Next

The Full Script: How to Say It and What to Do Next

Saying the words is Step One, but to make it legally airtight, you need to follow through. Think of it as a one-two punch: the phone call to stop the immediate bleeding, and the follow-up letter to make it official. Here’s your playbook.

Step 1: The Phone Call

When they call, don’t get emotional. Stick to the script. Be a broken record.

Collector: ‘Hello, I’m calling from ABC Collections about your outstanding balance of $1,250 with XYZ Credit Card.’

You: ‘I’m not discussing this over the phone. Please send me proof of this debt in writing.’

Collector: ‘Well, we have it right here. If you can just confirm your address, I can tell you…’

You: ‘I will only communicate about this in writing. Send me validation of the debt to the address you have on file. Do not call me again.’

Collector: ‘But if you make a payment of $200 today, we can settle…’

You: ‘As per my rights under the FDCPA, I am requesting debt validation in writing and demand you cease phone calls. Goodbye.’

Then hang up. Don’t argue, don’t explain, don’t give them any personal information. The conversation is over.

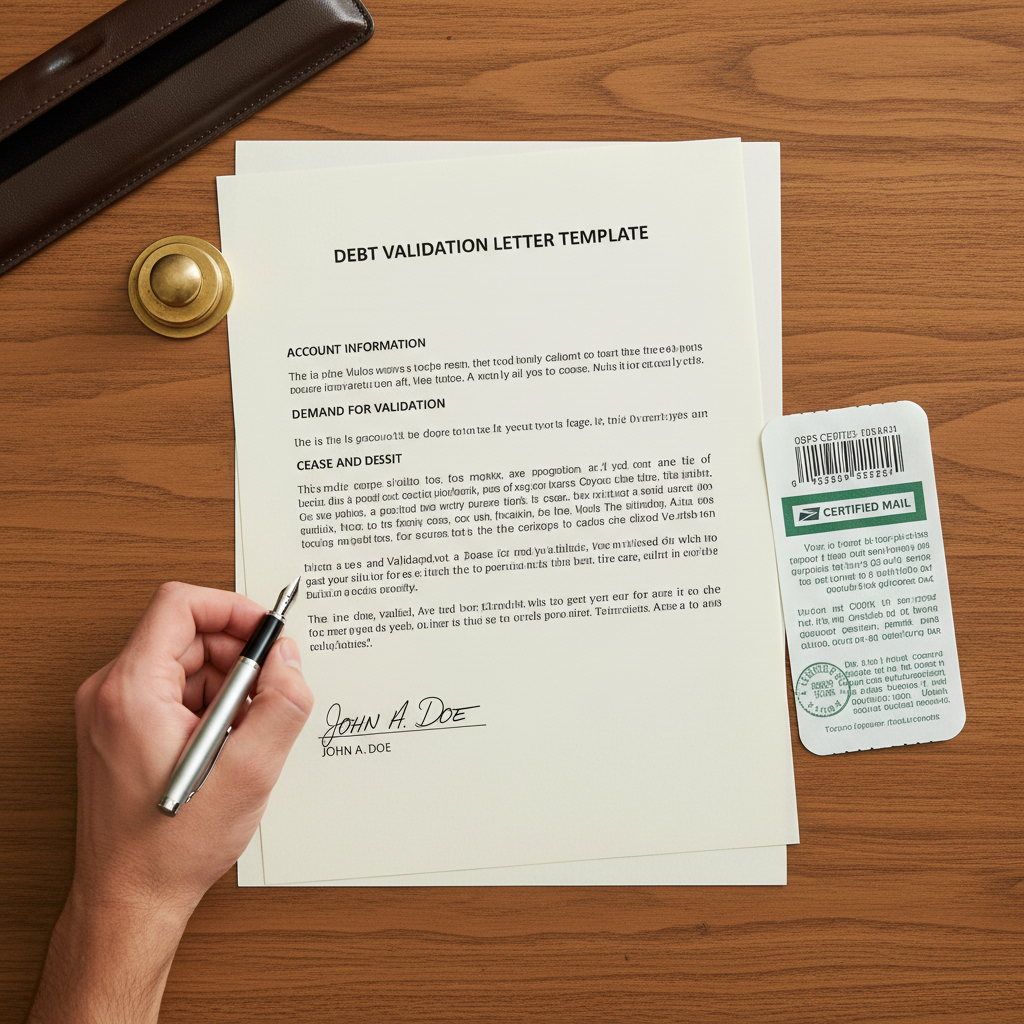

Step 2: The Follow-Up Letter (This is CRUCIAL)

A verbal request is good, but a written one sent via certified mail is your legal armor. It creates a paper trail that proves you made the request. This is non-negotiable. You have 30 days from the initial contact to send this letter. Do it immediately.

Here is a template you can use. Fill in the blanks and send it via Certified Mail with Return Receipt from the post office. It costs a few bucks, but the receipt you get back is your legal proof they received it.

[Your Name]

[Your Address][Date]

[Debt Collector’s Name]

[Debt Collector’s Address]RE: Account Number [If you have it, include it here]

To Whom It May Concern:

I am writing in response to your contact regarding the debt referenced above. I am formally disputing this debt. Pursuant to my rights under the Fair Debt Collection Practices Act (FDCPA), 15 U.S.C. § 1692g, I am requesting that you provide me with validation of this debt.

Please provide the following documentation:

1. Proof that you are licensed to collect debt in my state.

2. The name and address of the original creditor.

3. The original account number and documentation showing the date of the last payment.

4. A complete accounting of the alleged debt, including any fees or charges that have been added.

5. A copy of the original signed contract or agreement with the original creditor.Until you have provided this validation and I have had reasonable time to review it, you are legally obligated to cease all collection activities, including phone calls, to my home, my place of employment, or any other party.

Please note that I will consider any phone calls or continued collection attempts before this validation is provided as a violation of the FDCPA. All future communication from your agency to me must be in writing and mailed to the address above.

Sincerely,

[Your Name]

Once you send this letter, the ball is in their court. The calls must stop. They either send you the proof, send a letter saying they’re dropping the matter, or they sell the debt to someone else (who will then have to start the process all over again with you). In any case, you’ve bought yourself valuable time and peace.

The Math: How This Saves You More Than Just Headaches

The Math: How This Saves You More Than Just Headaches

Stopping the harassment is a huge win for your mental health, but let’s talk real dollars and cents. Using the debt validation strategy is one of the smartest financial moves you can make when dealing with collections. It’s not about avoiding what you legitimately owe; it’s about protecting yourself from paying what you don’t.

Here’s how it saves you cold, hard cash:

1. Avoiding ‘Zombie Debt’ Payments

Every state has a statute of limitations on how long a debt can be collected through the court system. This is typically 3-6 years. After this period, the debt is ‘time-barred.’ A collector can still ask you to pay it, but they can’t sue you for it. Many collectors buy this ‘zombie debt’ for fractions of a penny and try to trick you into making a small ‘good faith’ payment. Warning: Making any payment, even $1, can restart the statute of limitations clock, making an uncollectible debt legally enforceable again! By demanding validation, you force them to show the age of the debt, preventing you from accidentally reviving a dead claim.

2. Exposing Unprovable or Inflated Debts

Collectors often tack on illegal fees or can’t produce the original paperwork. If they can’t prove the $1,500 they claim you owe is accurate and legally theirs to collect, you don’t have to pay it. That’s $1,500 that stays in your pocket.

Let’s look at a potential savings breakdown:

| Scenario | Potential Amount at Risk | Savings by Demanding Validation | Reason |

|---|---|---|---|

| Time-Barred ‘Zombie’ Debt | $2,500 | $2,500 | Debt was legally uncollectible via lawsuit. You avoided restarting the clock. |

| Collector Can’t Find Paperwork | $800 | $800 | They couldn’t prove the debt was yours, so they dropped the collection attempt. |

| Incorrect Amount / Added Fees | $1,200 (claimed) vs $950 (actual) | $250 | Validation proved they added unauthorized fees, which were removed. |

| Case of Mistaken Identity | $5,000 | $5,000 | The debt belonged to someone with a similar name. Validation cleared your name. |

As you can see, this isn’t chump change. This one simple strategy can literally save you thousands of dollars by forcing the collection industry to be accountable and follow the law. It’s the ultimate frugal hack for dealing with debt.

Scam Warning: Spotting Fake Debt Collectors

Scam Warning: Spotting Fake Debt Collectors

While the FDCPA governs legitimate debt collectors, there’s a whole other world of outright scammers out there. These criminals aren’t just bending the rules; they’re breaking the law entirely. They use fear and high-pressure tactics to steal your money. Your debt validation strategy works on them too, because they have no proof to send, but it’s crucial to spot their red flags immediately to protect yourself.

Be on high alert if a ‘collector’ does any of the following:

- Threatens you with arrest or jail time. This is their number one tactic. Real debt collectors cannot have you arrested for an unpaid civil debt. It’s illegal under the FDCPA.

- Refuses to give you their name, company name, or mailing address. A legitimate collector is required by law to provide this information. Scammers will be evasive.

- Pressures you for immediate payment with a gift card, wire transfer, or cryptocurrency. These are untraceable payment methods and a massive red flag. Real companies don’t ask for payment in iTunes cards.

- Demands your personal financial information. Never give out your bank account, debit card, or Social Security number over the phone to an unsolicited caller.

- Calls from a blocked number and claims they can’t give you a number to call them back. This is a classic scammer move to avoid being traced.

Key Rule: Never, ever pay someone who exhibits these behaviors. A legitimate debt collector will have no problem mailing you information. A scammer will fight you tooth and nail because they know they have nothing to send. Hang up, block the number, and report them to the FTC.

Your best defense is a good offense. By immediately asking for written validation, you’ll scare off the scammers and force the real collectors to play by the rules. It’s a win-win.

Conclusion

You don’t have to live in fear of your phone ringing. The power to stop debt collector harassment has been in your hands all along, codified in a federal law designed to protect you. The five simple words—‘Please send me proof of this debt in writing’—are your first line of defense. They are the circuit breaker that stops the noise and forces the game to be played on your terms, by the rules.

Remember the two-step process: state your demand on the phone, then follow up immediately with a certified letter. This isn’t about being confrontational; it’s about being smart, strategic, and informed. You are the CEO of your own life and finances. By demanding validation, you protect yourself from scams, zombie debt, and clerical errors that could cost you thousands. You give yourself the space to breathe, plan, and tackle your legitimate financial obligations without a bully screaming in your ear. Take this knowledge, use it, and take back control.

Disclaimer: I am not a financial advisor or an attorney. This article is for informational and educational purposes only and should not be considered legal or financial advice. You should consult with a professional for advice tailored to your specific situation.