Boost Your Credit Score 100 Points! The Ultimate Beginner’s Guide

Listen up. That three-digit number—your credit score—is more than just a grade from the financial bigwigs. It’s the key that unlocks lower interest rates, better loan terms, and ultimately, more money in your pocket. We’re talking about the difference between a soul-crushing car payment and one that barely makes a dent. For too long, the credit game has been confusing and intimidating, designed to keep you guessing. No more. This isn’t your parents’ boring financial guide. This is the ultimate beginner’s playbook, a straight-up guide to taking control and jacking up your score. Forget the myths and the so-called ‘gurus’. We’re giving you the real, actionable strategies to boost your score by 100 points or more, starting right now.

The Bottom Line: Why Your Score is Your Financial Report Card

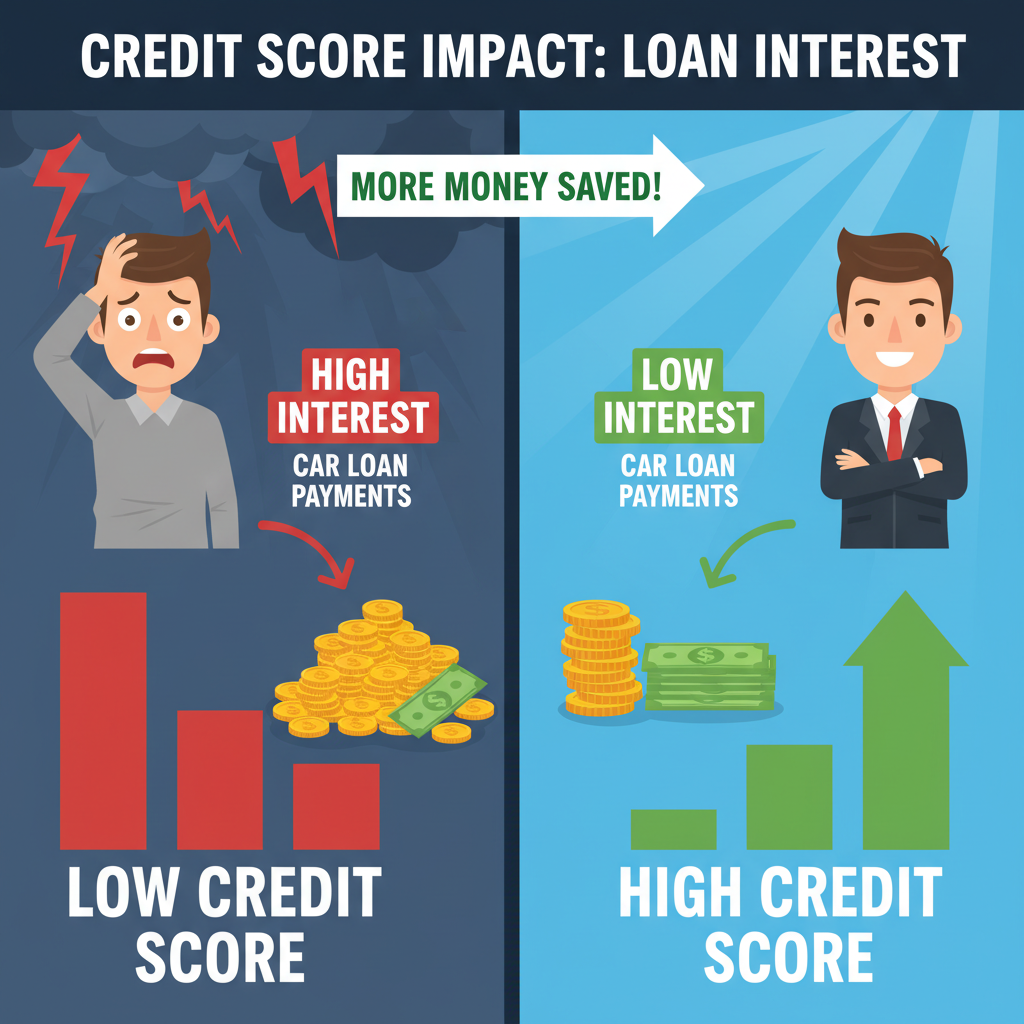

Before we get into the hacks, you need to understand the ‘why’. Lenders use your credit score to decide if you’re a good bet. A high score says, ‘This person pays their bills, they’re reliable.’ A low score screams, ‘RISK!’ and they make you pay for that risk with higher interest rates. This isn’t small change; we’re talking about thousands of dollars over the life of a loan. Think of it as a ‘good financial behavior’ discount. You wouldn’t pay full price if you had a coupon, so why pay extra interest if you don’t have to?

The Real-World Math: Good Score vs. Bad Score

Let’s break down what a 100-point difference actually means for your wallet. Imagine you’re buying a used car for $20,000 on a 5-year (60-month) loan.

| Credit Score | Typical APR | Monthly Payment | Total Interest Paid |

|---|---|---|---|

| Poor (580-669) | ~11.92% | $444 | $6,640 |

| Good (670-739) | ~6.70% | $393 | $3,580 |

| The Difference | -5.22% | $51/month | $3,060 Saved! |

Look at that. Just by having a better score, you’d save over $3,000. That’s a vacation, an emergency fund, or a serious boost to your side hustle. That’s real money. This is why we hustle. This is why we get smart about our credit.

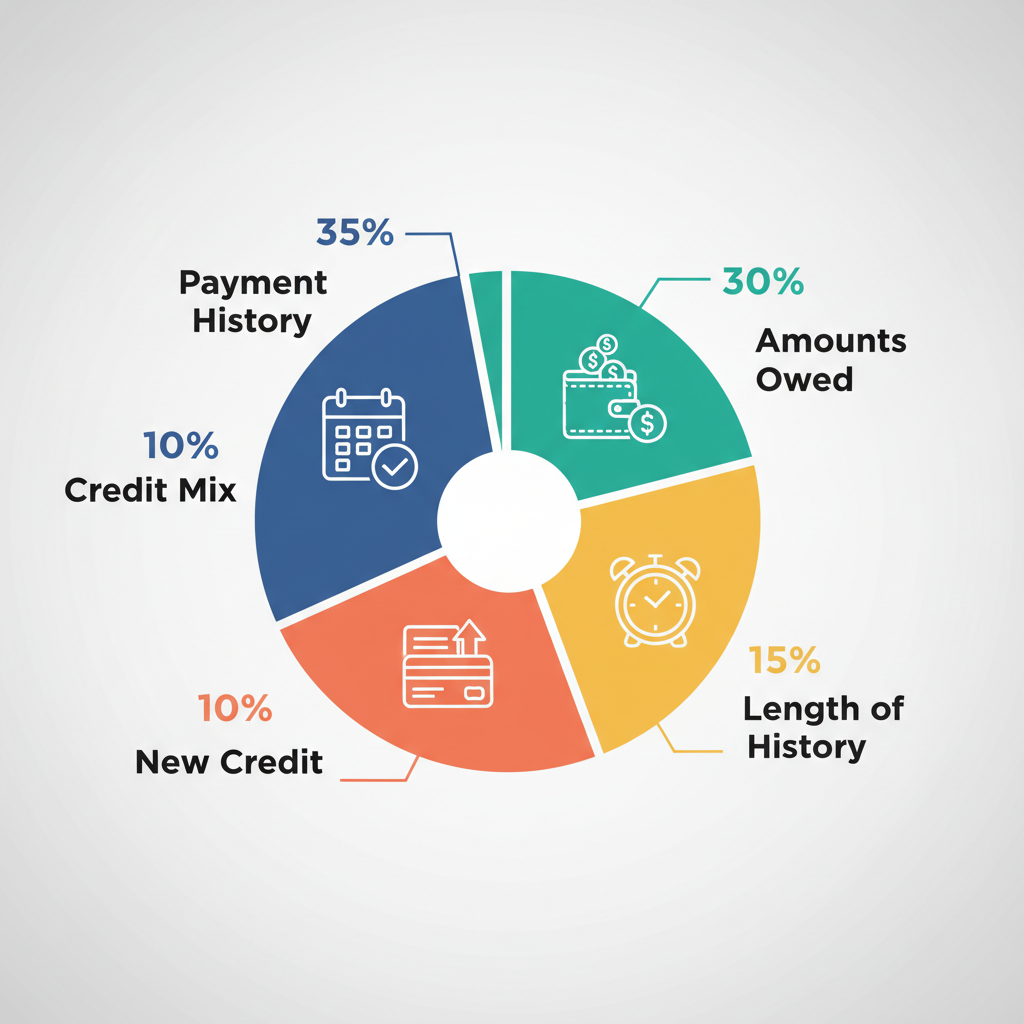

The Game Plan: Know the 5 Factors That Control Your Score

You can’t win the game if you don’t know the rules. Your FICO score, the one most lenders use, is calculated based on five key factors. Master these, and you master your score. It’s that simple.

- Payment History (35%): This is the heavyweight champion. Do you pay your bills on time? That’s it. One late payment can tank your score. This is non-negotiable.

- Amounts Owed / Credit Utilization (30%): This is how much of your available credit you’re using. If you have a $10,000 limit and a $5,000 balance, your utilization is 50%. We’ll get into why this is a massive opportunity for a quick score boost.

- Length of Credit History (15%): The average age of your accounts. Older is better. This factor rewards patience and long-term good habits.

- New Credit (10%): How many new accounts have you opened recently? Opening a bunch of cards at once looks desperate to lenders. It’s a red flag.

- Credit Mix (10%): Lenders like to see that you can handle different types of credit, like credit cards (revolving credit) and installment loans (car loans, mortgages).

Focus your energy on the big two: Payment History and Credit Utilization. They make up 65% of your score and are the areas where you can make the fastest, most impactful changes.

Level Up Move #1: Crush Your Credit Utilization Ratio

If you’re looking for the fastest way to see a significant point jump, this is it. Your Credit Utilization Ratio (CUR) is the percentage of your available credit that you’re currently using. High balances signal to lenders that you might be overextended. The lower your CUR, the better your score.

The Golden Rule of Utilization

Key Rule: Keep your overall credit utilization below 30% at all times. For a pro-level score boost, aim to keep it under 10%.

So, if you have a total credit limit of $10,000 across all your cards, you should never have more than a $3,000 balance reporting on your statements. To really crush it, aim for under $1,000.

Two Killer Plays to Lower Your CUR:

- The Debt Pay-Down Blitz: This is straightforward. Throw every extra dollar you can at your credit card balances. Start with the card that has the highest utilization (balance divided by limit), not necessarily the highest interest rate, for the fastest score impact.

- The Limit Increase Ask: Call the number on the back of your credit cards and ask for a credit limit increase. If you have a good payment history, they’ll often grant it. This instantly lowers your utilization without you paying a dime. For example, if you have a $2,000 balance on a $4,000 limit card (50% CUR), getting that limit raised to $8,000 instantly drops your CUR to a much healthier 25%.

Level Up Move #2: Make Late Payments a Thing of the Past

Your payment history is 35% of your score for a reason: it proves you’re reliable. A single 30-day late payment can drop your score by 60-110 points and stay on your report for seven years. It’s a killer. You must make this a zero-tolerance area of your financial life.

Your Automation Arsenal:

- Set Up Autopay: Log in to all your credit card accounts right now and set up automatic payments for at least the minimum amount. This is your safety net. You can always pay more manually, but this ensures you’re never late.

- Use Calendar Alerts: Set up two reminders on your phone’s calendar for each due date: one a week before and one two days before. This gives you time to make sure the money is in your account.

What If I Already Have a Late Payment? The Goodwill Tactic

Made a mistake? It happens. If you have an otherwise good history with a creditor, you can send a ‘goodwill letter’ asking them to remove the late payment notation as a courtesy. It’s not guaranteed, but it’s worth the shot.

Sample Script Snippet: “I am writing to respectfully request a goodwill adjustment to my payment history on account [Your Account Number]. I have been a loyal customer for [Number] years and have always prided myself on my on-time payments. Unfortunately, due to [a simple, honest reason like a technical error or family emergency], I missed the payment due on [Date]. I have since paid the account in full and have set up autopay to ensure this never happens again. Would it be possible to have this one-time late payment removed from my credit report?”

Level Up Move #3: The Smart Plays for Building Credit History

Whether you’re starting from scratch or recovering from past mistakes, you need to show lenders you can handle credit responsibly over time. This is about playing the long game with a few clever shortcuts.

For the Credit Newbie:

- Secured Credit Cards: This is the best entry point. You provide a small security deposit (e.g., $200), and that becomes your credit limit. You use it like a regular credit card, and after 6-12 months of on-time payments, you’ll often get your deposit back and be upgraded to an unsecured card. It’s like credit with training wheels.

- Credit-Builder Loans: These are offered by credit unions and some banks. You don’t get the money upfront. Instead, you make small monthly payments into a locked savings account. At the end of the term, you get the money back, and you’ve built a solid history of on-time payments.

The Piggyback Hack:

- Become an Authorized User: If you have a trusted family member or partner with a long history of on-time payments and low utilization on a credit card, ask them to add you as an authorized user. You don’t even need to use the card. Their positive history for that account gets reported on your credit file, which can give you a major boost, especially for the ‘Length of Credit History’ factor.

Free Tools to Use:

Look into services like Experian Boost. It’s a free tool that lets you add on-time utility, phone, and streaming service payments to your Experian credit report. It’s a no-brainer way to get credit for bills you’re already paying.

Scam Alert: Don’t Get Played by Credit Repair Sharks

The moment you start looking into credit repair, you’ll be bombarded by ads from companies promising the world. Be skeptical. Most of what they charge you hundreds or thousands for, you can do yourself for free using the strategies in this guide. These companies prey on desperation.

Scam Warning: Red Flags to Watch For

- They demand you pay hefty fees before they do any work. (This is illegal under the Credit Repair Organizations Act).

- They ‘guarantee’ to remove negative information from your report, even if it’s accurate. (No one can guarantee this).

- They tell you to dispute everything on your report, regardless of its accuracy.

- They advise you to create a new credit identity by applying for an Employer Identification Number (EIN) instead of using your Social Security Number. (This is fraud).

You are your own best advocate. The law (Fair Credit Reporting Act) gives you the right to dispute inaccurate information on your credit report for free. You don’t need to pay a shark to do it for you. Stick to the legitimate strategies: pay on time, keep balances low, and be patient.

Conclusion

There you have it—the straight-up, no-fluff game plan to take your credit score to the next level. This isn’t magic; it’s strategy. By focusing on the big wins—crushing your utilization and locking down your payment history—you can see a 100-point jump faster than you think. Remember, your credit score is a tool. A powerful one. A better score means lower payments, more approvals, and more financial firepower to achieve your goals. Take these plays, put them into action, and take back control of your financial future. You’ve got this.

Disclaimer: I am not a financial advisor. The information provided in this article is for educational and informational purposes only and does not constitute financial advice. You should consult with a qualified professional before making any financial decisions.