You’re Wrong About Taxes: How Marginal Tax Brackets Actually Work

Let’s get one thing straight: if you’ve ever turned down a gig, avoided a raise, or hesitated on your side hustle because you were afraid it would ‘bump you into a higher tax bracket,’ you’ve been played. Played by a myth that costs people real money every single year. The idea that earning one extra dollar will cause your *entire* income to be taxed at a higher rate is one of the most persistent and damaging lies in personal finance.

Forget the confusing jargon and the intimidating forms. We’re going to break this down street-smart style. Understanding this one concept—marginal tax brackets—is like a cheat code for your financial life. It removes the fear and gives you the power to confidently chase more income. This isn’t just about taxes; it’s about giving you the green light to build your wealth without hesitation. So, let’s kill this myth once and for all and get you paid.

The Big Lie: What Everyone Gets Wrong About Tax Brackets

The core of the confusion is a simple misunderstanding. People hear ‘22% tax bracket’ and think it’s a flat tax on everything they earn once they cross that line. That’s dead wrong. Our tax system is progressive, which is just a fancy way of saying you pay different rates on different parts of your income.

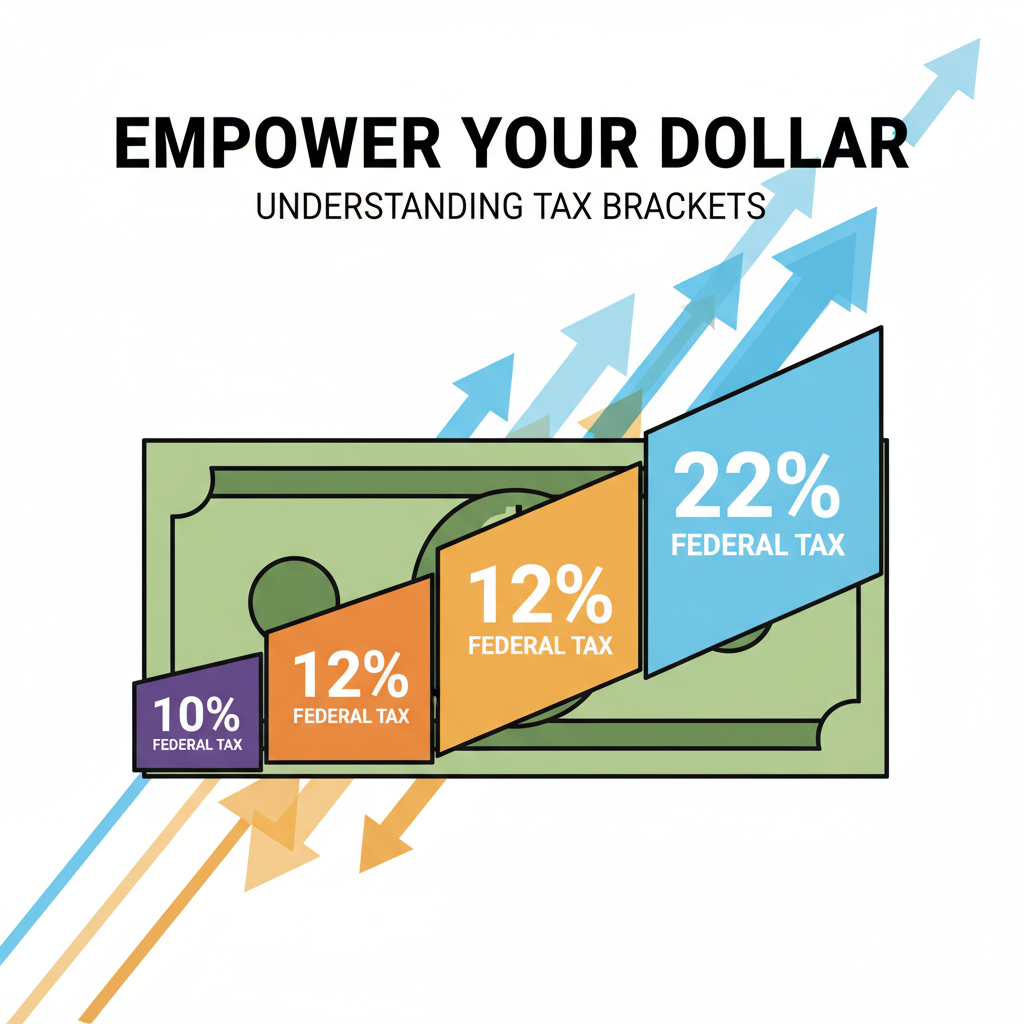

Think of it like a series of buckets you have to fill with your income, one by one.

- Bucket 1 (The 10% Bracket): The first chunk of money you earn goes in here. Everything in this bucket gets taxed at 10%. Period.

- Bucket 2 (The 12% Bracket): Once the first bucket is full, your *next* dollars start filling this one. Only the money that lands in this specific bucket is taxed at 12%. The money in the first bucket? Still safe at 10%.

- Bucket 3 (The 22% Bracket): Once bucket two is full, the income you earn after that starts filling this bucket. And only the dollars that fall into this third bucket get taxed at 22%.

Getting a raise doesn’t mean you go back and pour a higher tax rate on the buckets you already filled. You just start pouring your new money into a new bucket with a higher rate. This means your marginal tax rate—the rate you pay on your *very last dollar earned*—might be 22%, but your effective tax rate—your total tax paid divided by your total income—is much, much lower. That’s the number that really matters, and it’s never as scary as the bracket number makes it sound.

The Math: How It Actually Works (No PhD Required)

Talk is cheap. Let’s run the numbers with a real-world example. Meet Alex, a graphic designer with a growing side hustle. We’ll use the 2023 tax brackets for a single filer for this breakdown (note: these numbers change slightly most years, but the principle is always the same).

Scenario 1: Alex Earns $44,000

Alex is squarely in the 12% bracket. Here’s how the IRS actually looks at this income:

- The first $11,000 is taxed at 10% = $1,100

- The rest of the income ($44,000 – $11,000 = $33,000) is taxed at 12% = $3,960

- Total Tax Owed: $1,100 + $3,960 = $5,060

Even though Alex is ‘in’ the 12% bracket, their actual tax rate is ($5,060 / $44,000) = 11.5%. See? Not 12%.

Scenario 2: Alex Crushes It and Earns $47,000

That extra $3,000 pushes Alex’s top earnings into the 22% bracket, which for 2023 started at $44,726. This is where people panic. But they shouldn’t. The math doesn’t lie.

Here’s the breakdown of Alex’s total tax bill now:

| Income Portion | Tax Rate | Tax Owed on this Portion |

|---|---|---|

| First $11,000 | 10% | $1,100.00 |

| From $11,001 to $44,725 (which is $33,725 of income) | 12% | $4,047.00 |

| From $44,726 to $47,000 (which is $2,275 of income) | 22% | $500.50 |

| Total Taxable Income: $47,000 | Effective Rate: ~12.01% | Total Tax: $5,647.50 |

Look at that! By earning an extra $3,000, Alex’s take-home pay (before tax on that portion) increased by $3,000. The total tax only went up by $587.50. Alex is still significantly richer. The jump to the 22% bracket only applied to that small sliver of new income. Alex is taking home an extra $2,412.50. That’s a win, any way you slice it.

Your New Superpower: Using This Knowledge to Maximize Your Hustle

Okay, so you get the math. Now what? Now you use it. This knowledge is a financial superpower that separates the pros from the panicked. Instead of fearing your next dollar, you can now strategize around it.

Make Confident Decisions

A client offers you a last-minute project for $2,000? In the past, you might have worried about the tax hit. Now you know your marginal rate. If you’re in the 22% bracket like Alex, you can instantly calculate your move. You know you need to set aside 22% of that $2,000 (which is $440) for federal taxes. The remaining $1,560 (plus any state tax considerations) is yours. The question is no longer ‘Will this hurt me?’ but ‘Is $1,560 worth my time?’ That’s a business decision, not a fear-based one.

The Golden Rule of Earning: Never, ever turn down a raise or a gig because you’re afraid of a new tax bracket. More gross income is always more net income. The system is designed to reward you for earning more, not punish you.

Lower Your Taxable Income… The Smart Way

Knowing your marginal rate also shows you the power of tax deductions. Every dollar you can deduct from your income is a dollar you *don’t* have to pay your highest tax rate on. For a side hustler, this is huge. That new laptop for your business? The mileage you drive to meet clients? These are business expenses that reduce your taxable income. If your marginal rate is 22%, every $100 in deductions saves you $22 in cash. It’s like an instant discount on your business costs.

Furthermore, this is why financial advisors talk so much about retirement accounts like a Traditional 401(k) or IRA. Contributing to these accounts lowers your taxable income for the year. Putting $5,000 into a Traditional IRA means you get to subtract $5,000 from the income the government taxes you on, potentially saving you hundreds or even thousands at your marginal rate.

The Pro Move: Finding Your ‘Real’ Tax Rate

Your marginal tax rate is your decision-making tool for *new* money. But your effective tax rate is your reality check. It’s the single best number to understand your overall tax burden. As we said before, the formula is simple:

Effective Tax Rate = (Total Tax You Paid) / (Your Total Taxable Income)

Let’s revisit Alex’s $47,000 income scenario. Alex’s marginal rate was 22%, which sounds high. But the effective rate tells the true story:

- Total Tax Paid: $5,647.50

- Total Taxable Income: $47,000

- Effective Tax Rate: $5,647.50 / $47,000 = 0.1201, or 12.01%

When you’re budgeting or trying to figure out how much of your income is really going to taxes, this is your number. It cuts through the noise of brackets and percentages and gives you a clear, simple picture. Knowing your effective rate is a massive confidence booster. It proves that you’re keeping way more of your hard-earned money than you probably thought.

You can calculate this easily after you’ve filed your taxes by looking at your tax form (like the 1040). Find your total tax and your taxable income, and do the simple division. This is a five-minute exercise that will arm you with crucial knowledge for the entire next year.

Conclusion

The fear of tax brackets is a ghost story for your finances. It’s a myth that holds people back from their true earning potential. Now you have the flashlight to see right through it. You know that our tax system is a series of buckets, and you only pay a higher rate on the money in the newest bucket. You know that earning more always means keeping more.

Use this knowledge as your permission slip to go bigger. Pitch that higher-paying client. Negotiate that raise. Scale your side hustle. When you understand the rules of the game, you can play to win. You’re not just a hustler; you’re a smart operator who knows how their money works. Now go get what you’ve earned.

Disclaimer: I am not a financial advisor, and this article is for informational and educational purposes only. Tax laws are complex and change frequently. Please consult with a qualified tax professional or certified financial planner for advice tailored to your specific situation.