How I Erased $5,000 in Medical Debt: 3 Negotiation Scripts That Work

That envelope hits your kitchen counter with a thud. You know what it is before you even open it. The medical bill. Your stomach sinks as you see the number—a figure so absurd it feels like a typo. $5,000. For what? A few hours in the ER? A routine procedure? It’s enough to make you want to crawl into a hole. But hold on. Before you drain your savings or sign up for a payment plan that stretches into the next decade, I’m here to tell you something the healthcare system doesn’t want you to know: that bill is a starting point, not a final verdict.

I’ve been there. I’ve felt that panic. But I turned that fear into a strategy. I treated that medical bill not as an unbreakable command, but as an opening offer from a business—a business that often makes mistakes. By shifting my mindset and using a few powerful, repeatable scripts, I got that $5,000 bill wiped out. This isn’t about luck or magic; it’s about knowing the game and having the right playbook. In this guide, I’m handing you my exact playbook. No fluff, no vague advice. Just the street-smart tactics and word-for-word scripts you need to call up that billing department and take back control of your financial life.

The Mindset Shift: Stop Thinking Like a Patient, Start Acting Like a Customer

First things first, we need to rewire your brain. When you’re sick or injured, you’re a patient. You’re vulnerable, and you place your trust in medical professionals. But the moment you get that bill, the relationship changes. You are now a customer dealing with a service provider. And let me tell you, this service provider has a shockingly high error rate. Studies have shown that up to 80% of medical bills contain errors. Let that sink in. You wouldn’t pay for a sandwich you didn’t order at a deli, so why would you blindly pay for a medical service you didn’t receive or that was coded incorrectly?

Your power lies in understanding this dynamic. The billing department is not a charity; it’s a business’s accounts receivable department. They want to close the books. A paid bill, even a partially paid one, is better for them than an unpaid one that goes to collections, where they only get pennies on the dollar. You are not begging for mercy; you are negotiating a business transaction. You are a customer questioning the accuracy and fairness of an invoice. Once you internalize this, you trade fear for confidence. You’re no longer asking for a handout; you’re demanding fair business practices. This mindset is the foundation of every successful negotiation.

Common Billing Errors to Hunt For:

- Duplicate Charges: Being billed twice for the same service, medication, or supply.

- Canceled Services: Charges for a test or procedure that was ordered but then canceled.

- Incorrect Quantities: Billed for ten pills when you only received one, or for a full hour of a service that only took 15 minutes.

- Upcoding: When a provider bills for a more expensive service than the one you actually received. This is illegal but happens all the time.

- Balance Billing: When you’re billed for the difference between what your insurance paid and what the provider charges, which may be prohibited if the provider is in-network.

Your Pre-Call Battle Plan: Gathering Your Arsenal

You don’t walk into a negotiation unprepared. A few minutes of prep work can save you thousands of dollars. Before you even think about picking up the phone, you need to build your case. This is your homework, and it’s the most important assignment you’ll have all year. Follow these steps methodically.

- Demand an Itemized Bill: The summary bill they send you is useless. It’s designed to be confusing. Call the billing department and say, “I need a complete, itemized bill with CPT codes for my date of service.” They are legally required to provide this. CPT (Current Procedural Terminology) codes are the specific codes for every single service, from a simple blood draw to complex surgery.

- Perform a Line-by-Line Audit: Once you have the itemized bill, grab a red pen and a highlighter. Go through it line by line. Does it look right? Were you actually in the hospital on that day? Did you receive that specific medication? Question everything. Circle anything that seems off, from a $50 charge for a single Tylenol to a duplicate lab test.

- Become a Code Investigator: Look at those CPT codes for major services. You can use free online resources like the CPT Code Search from the American Medical Association or websites like Healthcare Bluebook. This helps you understand what you’re being billed for and, more importantly, what the fair market price is in your area. If the hospital charged you $3,000 for a service that typically costs $800, you’ve just found your strongest negotiating point.

- Know Your Numbers: Before you call, decide on two numbers: 1) The amount you believe is fair and accurate based on your audit and research, and 2) The maximum amount you are willing and able to pay to settle the debt today. Having these numbers in your head prevents you from getting flustered and agreeing to a bad deal.

The Scripts That Slashed My Bill: 3 Word-for-Word Negotiation Tactics

Okay, this is it. You’ve done your prep, your heart is pounding a little, but you’re ready. Remember to be polite but firm. You’re a customer resolving a billing issue. Get the name of the person you’re speaking with and take detailed notes. Here are three scripts for three different scenarios.

Script 1: The ‘Eagle Eye’ Billing Error Angle

Use this when you’ve found clear errors on your itemized bill. This is the most straightforward approach.

“Hello, my name is [Your Name] and my account number is [Account Number]. I’m calling about my bill for my visit on [Date of Service]. I’ve received the itemized statement, and I’ve found a few potential errors I’d like to resolve. For example, on line 12, I was charged for [Service Name] under CPT code [Code Number], but my records show this test was canceled. Also, on line 18, I appear to have been charged twice for [Medication Name]. Could you please open an investigation into these charges and send me a revised, corrected bill?”

Why it works: You are being specific, professional, and non-accusatory. You’re not calling them scammers; you’re helping them correct an oversight. This puts them in problem-solving mode, not defense mode.

Script 2: The ‘Cash is King’ Prompt Pay Offer

Use this when the bill is technically correct, but the price is inflated, or you simply want to settle for less. This is incredibly effective because hospitals love getting guaranteed cash now versus chasing a debt for months or years.

“Hi, my name is [Your Name], account number [Account Number]. I’m calling about my outstanding balance of $5,000. The bill is more than I can manage right now, but I am in a position to resolve this today. Uninsured patients or those paying directly often receive a discount. I’d like to be extended that same rate. Based on my research, a fair price for these services is closer to $2,000. If you can adjust the bill to that amount, I can pay the full $2,000 over the phone right now via credit card.”

Why it works: You’ve made a specific, reasonable offer and created a sense of urgency. The phrase “pay the full amount right now” is music to a bill collector’s ears. They may counter-offer, but you’ve just started a real negotiation.

| Negotiation Tactic | Original Bill | Potential Offer (40% of Original) | Potential Savings |

|---|---|---|---|

| Prompt Pay Offer | $5,000 | $2,000 | $3,000 |

| Prompt Pay Offer | $1,200 | $480 | $720 |

| Prompt Pay Offer | $10,000 | $4,000 | $6,000 |

Script 3: The ‘Financial Hardship’ Lifeline

Use this when you genuinely cannot afford to pay, even a discounted amount. Be honest and prepared to provide documentation if requested.

“Hello, my name is [Your Name], account number [Account Number]. I’m calling about my bill for $5,000. Honestly, paying this bill is a significant financial hardship for my family right now. My income is [Your Income] and I simply do not have the resources to cover this amount. I want to do the right thing and pay what I can, but I need help. Could you please tell me about your financial assistance or charity care programs? I’d be happy to fill out any necessary applications to see if I qualify for a bill reduction or forgiveness.”

Why it works: Non-profit hospitals are legally required to have financial assistance policies. You are showing a willingness to pay while clearly stating your inability to cover the full amount. This moves the conversation from collections to assistance, which is a completely different department with a different goal: to help, not just collect.

Don’t Get Played: How to Lock In Your Deal in Writing

You did it. They agreed to lower your bill from $5,000 to $1,500. You’re floating on air. DO NOT HANG UP THE PHONE YET. A verbal agreement is worth the paper it’s written on—nothing. The person you spoke with could quit tomorrow, and their system might have no record of your conversation. You must lock it in.

“That’s fantastic, thank you so much. I can pay the $1,500 now. Before I give you my card number, can you please give me a reference number for this call and our agreement? Also, can you confirm that this payment will settle the account in full, with a zero balance, and that it will not be reported to credit bureaus as ‘settled for less than the full amount’? Finally, can you please send me a confirmation letter or email reflecting the new balance and our agreement?”

Wait on the phone until you receive that email. If they can only send a letter, ask them to put a note on your account reflecting the agreement and tell them you will make the payment as soon as you receive the letter. Do not pay a single cent until you have written proof. This is non-negotiable. This is how you protect yourself and ensure your hard work doesn’t go to waste.

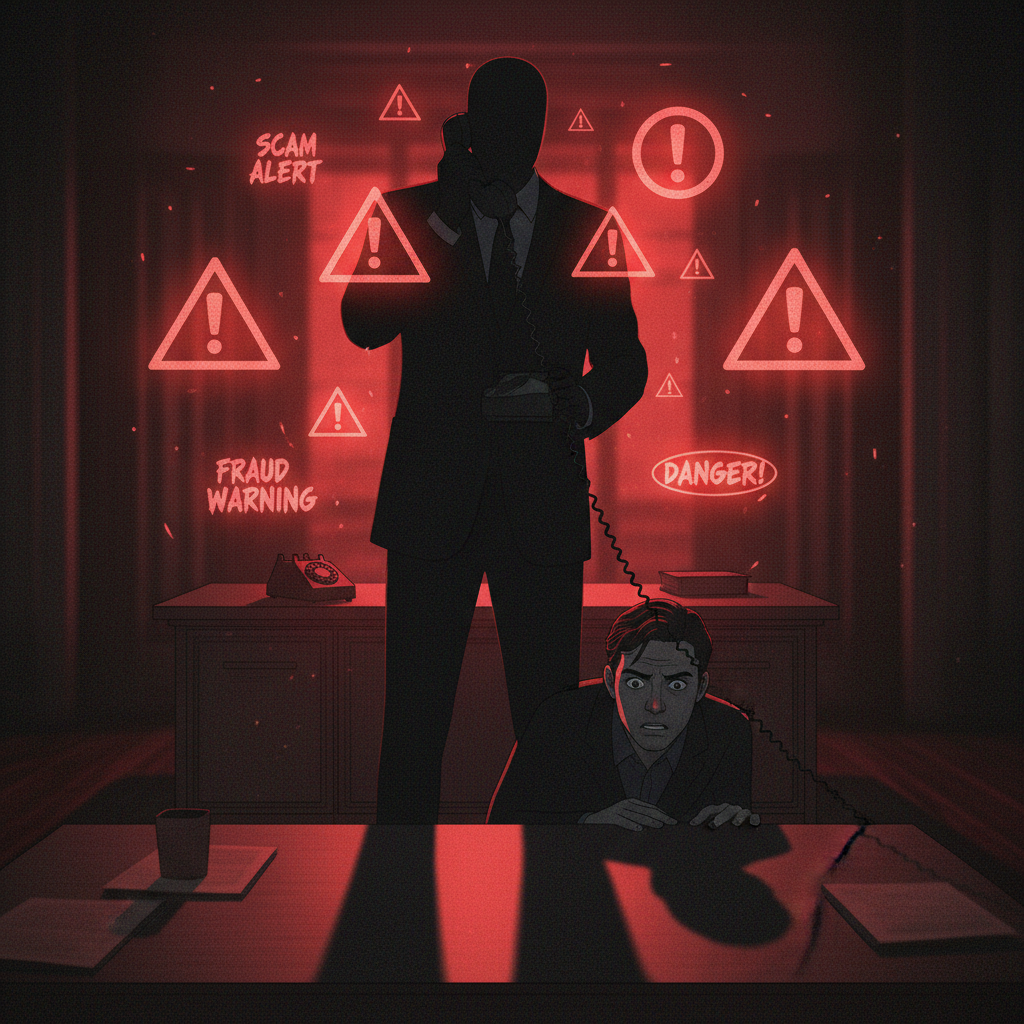

Scam Warning: Watch Out for These Medical Debt Sharks

As you navigate this process, you need to be aware of the predators. The world of debt is full of them, and medical debt is a feeding frenzy. Be on the lookout for these red flags, whether from a third-party collector or even the provider’s own aggressive billing department.

- High-Pressure Tactics: Anyone who threatens you with immediate legal action, jail time (which is illegal for consumer debt), or tells you that you have to pay *right now* without time to think is a major red flag.

- Refusal to Provide Documentation: If a collector refuses to mail you a written validation of the debt or your payment agreement, hang up. It’s likely a scam.

- Requesting Weird Payment Methods: No legitimate medical provider or collection agency will ask you to pay via wire transfer, gift card, or a pre-paid debit card. That’s a classic scammer move.

- The ‘Debt Relief’ Mirage: Be very wary of for-profit companies that promise to erase your medical debt for a hefty upfront fee. Many of them do nothing more than what you can do yourself for free using the scripts in this article.

Key Rule: Never provide personal information or payment to anyone who calls you out of the blue claiming to be collecting a debt. Hang up, find the original provider’s official billing number yourself, and call them directly to verify.

Conclusion

That $5,000 bill that once felt like a life sentence is now just a memory. By transforming from a passive patient into an empowered customer, you’ve taken control of the situation. You gathered your intel, you used a proven script, and you locked in your victory. This process works. It works for $500 bills and it works for $50,000 bills. The numbers change, but the strategy remains the same: question everything, negotiate with confidence, and always, always get it in writing.

Don’t let medical debt derail your financial goals or your peace of mind. You have the playbook now. Save it, share it, and the next time one of those envelopes lands on your counter, you won’t feel dread. You’ll feel ready. You’ll know exactly what to do.

Disclaimer: I am not a financial advisor, lawyer, or medical billing professional. This article details my personal experience and strategies for educational purposes. You should consult with a qualified professional for advice tailored to your specific situation.