Pay Off Debt FAST: Why The Avalanche Method Math Wins Every Time

Let’s get real. Being in debt sucks. It’s a weight on your shoulders, a drain on your bank account, and a constant source of stress. You see your hard-earned cash disappear every month to interest payments, and it feels like you’re running on a treadmill going nowhere. You’ve probably heard about different strategies to pay it off, mainly the ‘Debt Snowball’ and the ‘Debt Avalanche’.

The Snowball method gets a lot of hype because it gives you quick, feel-good wins. But we’re not here for feelings, we’re here for results. We’re here to get you financially free as fast as humanly possible. That’s where the Debt Avalanche comes in. It might not give you the instant gratification of knocking out a tiny debt, but the math is undefeated. It is, without a doubt, the most efficient, money-saving, and fastest way to kill your debt. Stick with me, and I’ll show you why the math always wins and how you can put this powerhouse strategy to work for you, starting today.

The Main Event: Debt Avalanche vs. Debt Snowball

Before you can pick a winner, you gotta know the fighters. In one corner, you have the crowd-pleasing Debt Snowball. In the other, the quiet but deadly champion, the Debt Avalanche. They both have the same goal—get you to a $0 balance—but their game plans are night and day.

The Debt Snowball: The Emotional Favorite

The Snowball method is all about momentum and psychology. Here’s the play-by-play:

- You list all your debts from the smallest balance to the largest, completely ignoring the interest rates.

- You make minimum payments on everything, but you throw every extra cent you can find at the smallest debt.

- Once that smallest debt is toast, you feel a rush. A win! You then take the money you were paying on it (the minimum payment plus all the extra cash) and roll it into the next smallest debt.

- You repeat this process, creating a ‘snowball’ of a payment that gets bigger as it rolls through your debts.

The appeal is obvious: you get to cross debts off your list quickly at the beginning, which can be a huge motivator. It feels good. But feeling good can come at a steep price.

The Debt Avalanche: The Mathematical Champion

The Avalanche method doesn’t care about your feelings. It cares about your wallet. It’s a cold, calculated strategy designed for one thing: maximum efficiency.

- You list all your debts, but this time you rank them from the highest interest rate (APR) to the lowest. The actual balance doesn’t matter for the ranking.

- You make minimum payments on all your debts to keep them in good standing.

- You unleash every spare dollar you have on the debt with the highest interest rate. This is your financial enemy #1.

- Once that high-interest monster is dead, you take its entire payment (minimum plus all the extra) and redirect that cash cannon to the debt with the next-highest interest rate.

Think of it this way: high-interest debt is a fire that’s burning your money. The Snowball method has you blowing out candles while a bonfire rages in the corner. The Avalanche method sends you straight for the bonfire with a firehose. It’s less glamorous at the start, but it puts out the fire faster and saves more of your house from burning down.

The Cold, Hard Math: Why Avalanche Saves You Real Money

Talk is cheap. Let’s run the numbers and see the proof. This is where the Avalanche method leaves the Snowball in the dust. We’re going to use a common debt scenario and assume you’ve hustled up an extra $400 per month to throw at your debt. Pay close attention to the ‘Total Interest Paid’ and ‘Payoff Time’ columns. That’s your money and your time.

Your Debts:

- Credit Card (Enemy #1): $4,500 at a nasty 21.99% APR. Minimum payment: $120.

- Personal Loan: $8,000 at a more reasonable 9.5% APR. Minimum payment: $250.

- Student Loan: $12,000 at a low 4.75% APR. Minimum payment: $150.

Total Minimum Payments: $520. Your Extra Payment: $400. Total Monthly Debt Attack: $920.

Now let’s see how the two strategies play out with the exact same money.

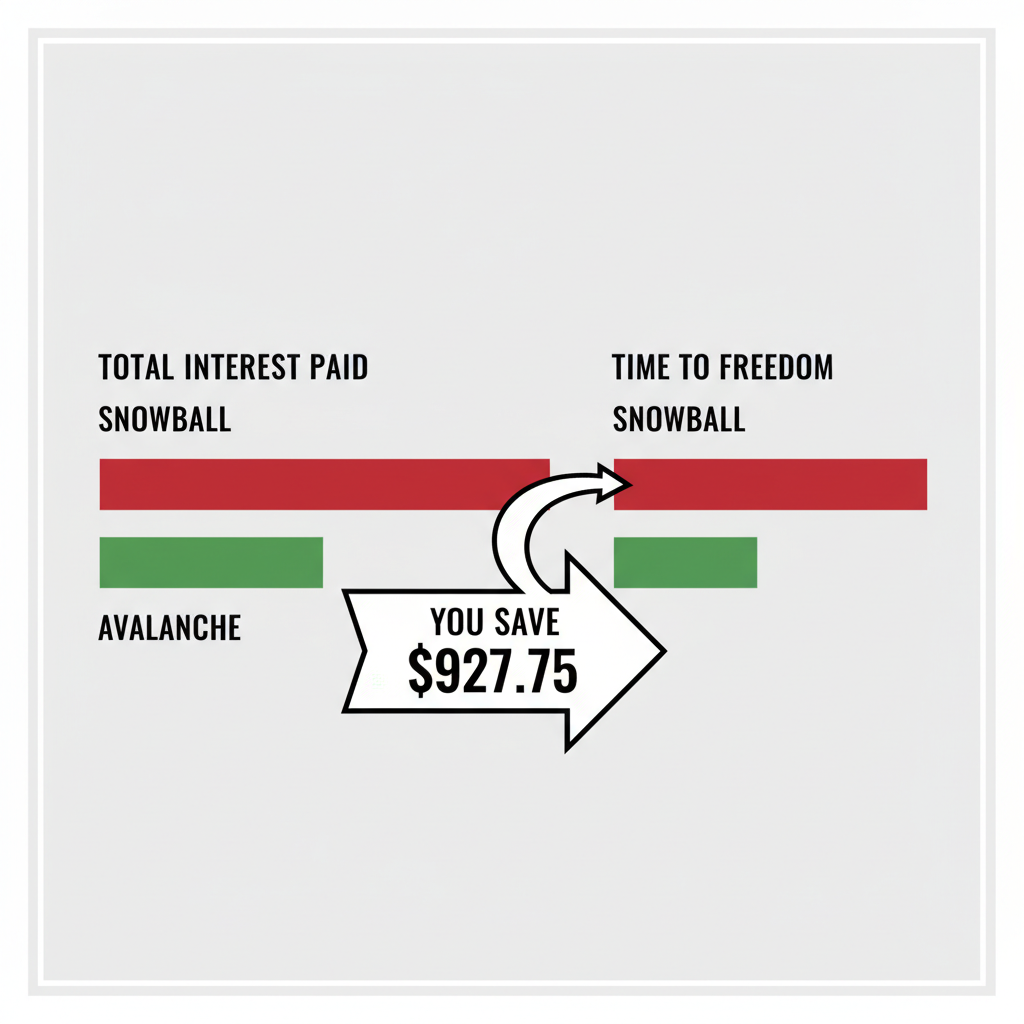

The Showdown: By the Numbers

| Strategy | Payoff Order | Total Interest Paid | Total Time to Debt-Free |

|---|---|---|---|

| Debt Snowball (Smallest Balance First) | 1. Credit Card ($4,500) 2. Personal Loan ($8,000) 3. Student Loan ($12,000) |

$6,215.89 | 37 Months |

| Debt Avalanche (Highest Interest First) | 1. Credit Card (21.99%) 2. Personal Loan (9.5%) 3. Student Loan (4.75%) |

$5,288.14 | 35 Months |

The Verdict

The numbers don’t lie. In this scenario, the payoff order happens to start the same, but the long-term impact is what matters. By using the Debt Avalanche method, you would pay off your debt 2 months faster and, more importantly, you would keep $927.75 in your pocket. That’s nearly a thousand dollars you didn’t have to hand over to the banks, all because you chose math over momentary satisfaction. Imagine if your debts were larger or the interest rates were higher. The savings would be even more massive. This is the power of targeting the interest rate first. You stop the bleeding where it’s most severe.

Your Avalanche Action Plan: How to Start Crushing Debt Today

Knowing the math is one thing; putting it into action is another. It’s time to stop planning and start doing. Here is your no-nonsense, step-by-step guide to launching your own debt avalanche.

-

Step 1: Get All Your Numbers in One Place

You can’t fight an enemy you can’t see. Grab every single one of your debt statements—credit cards, car loans, student loans, personal loans, medical bills, everything. Create a simple list or spreadsheet with four columns: Creditor (who you owe), Total Balance, Minimum Monthly Payment, and the most important number of all, the APR (Interest Rate).

-

Step 2: Create Your Hit List

Sort that list. Not by the balance, but by the APR, from the highest percentage down to the lowest. The debt at the very top of that list is your new obsession. This is your Target #1. Everything else is secondary.

-

Step 3: Find Your Extra Ammo

Your minimum payments are just keeping you afloat. The extra money is your weapon. This is where your side-hustle mentality and frugal living skills shine. Go through your budget with a fine-tooth comb. Can you cancel subscriptions? Cook more at home? Negotiate your cell phone bill? Can you pick up extra shifts, start that dog-walking gig, or sell stuff you don’t need online? Every single extra dollar you can squeeze out of your budget or earn on the side is ammunition to fire at your high-interest debt. Aim for a specific, consistent number you can throw at it every month.

-

Step 4: Automate and Annihilate

Set up automatic payments for the minimum amount due on all debts EXCEPT for Target #1. This prevents missed payments and keeps your credit healthy. Then, for Target #1, you attack. You pay the minimum PLUS all the extra ammo you found in Step 3. If you can, make extra payments bi-weekly instead of monthly to reduce the principal even faster. Be relentless.

-

Step 5: The Roll-Up and Repeat

The moment you make that final payment on Target #1, you celebrate for exactly five minutes. Then, you get back to work. Take the entire amount you were paying on that now-dead debt (the original minimum + all the extra cash) and add it to the minimum payment of Target #2 on your list. Your payment cannon just got bigger. You repeat this process, rolling up your payments into an unstoppable force until you’ve wiped out every single debt on your list. That’s the avalanche.

The Mental Game: Sticking With It When It Feels Slow

Let’s be honest: the biggest weakness of the Debt Avalanche is the mental game. If your highest-interest debt is also your largest balance, it can feel like you’re chipping away at a mountain with a teaspoon. The quick wins from the Snowball method can seem mighty tempting. But you’re smarter than that. You’re playing the long game to win big. Here’s how to stay motivated.

Reframe Your ‘Win’

Instead of celebrating a $0 balance on a small account, celebrate the money you’re saving. Create a chart that tracks how much interest you’ve *avoided* paying each month. That’s a real, tangible win. Every time you throw an extra $100 at a 22% APR credit card, you’re not just paying down debt; you’re giving yourself a 22% return on that money. No stock market can guarantee that. That’s a boss move.

Make It Visual

Your spreadsheet is great for tracking, but you need a visual motivator. Print out a debt-payoff thermometer or a chart for each loan. Every time you make a payment, color in a section. Seeing that red bar shrink and the green ‘Paid Off’ section grow gives you a powerful visual sense of progress, even when the numbers on the statement feel stubbornly high.

Find Your ‘Why’

Why are you doing this? Is it to quit a job you hate? To travel? To buy a house? To finally stop stressing about money? Write that reason down. Tape it to your bathroom mirror, make it your phone’s lock screen. When you’re tempted to skip an extra payment for a night out, that ‘why’ will be the kick in the pants you need to stay on track.

Remember this key rule: You are in a war against interest. Every dollar you pay in interest is a dollar you can’t use to build your own future. The Debt Avalanche is your strategy to win that war.

Conclusion

The debate between Debt Snowball and Debt Avalanche will probably go on forever. The Snowball method has its place for people who need those quick psychological boosts to get started. But if you’re a Frugal Hacker, a side hustler, or anyone who respects their own hard-earned money, the choice is clear. The math doesn’t have an opinion, and it doesn’t get emotional. It simply points to the fastest and cheapest path to zero debt.

The Debt Avalanche method is your declaration that you’re done letting banks profit from your situation. You’re taking control, using logic, and strategically dismantling your debt in the most powerful way possible. It requires discipline and a focus on the long game, but the reward is immense: more money in your pocket, less time in debt, and the ultimate freedom of owning your financial future. Now stop reading. Go build your hit list and start the avalanche.

Disclaimer: This article is for informational and educational purposes only and should not be considered financial advice. You are encouraged to consult with a qualified financial professional to discuss your individual situation.