The Secret Trick To Doubling Your Credit Limit Instantly (Without A Hard Pull)

Alright, let’s get one thing straight. When we talk about doubling your credit limit, we’re not talking about a license to go on a shopping spree. Forget that noise. This is a power move. This is about playing the credit game to win, using the bank’s own rules to your advantage. A higher credit limit is one of the most underrated tools in your financial arsenal. It can instantly drop your credit utilization ratio, which is a fancy way of saying it makes you look way more responsible to lenders. The result? A healthier credit score, better loan offers, and more financial breathing room for your side hustles and life goals. Most people think asking for more credit means taking a hit on their score with a ‘hard pull.’ They’re wrong. There’s a backdoor method—a simple, digital request that often results in a ‘soft pull,’ leaving your precious credit score untouched. Ready to learn the hack? Let’s get to it.

The Real Reason a Higher Credit Limit is a Power Move (It’s Not About Spending More)

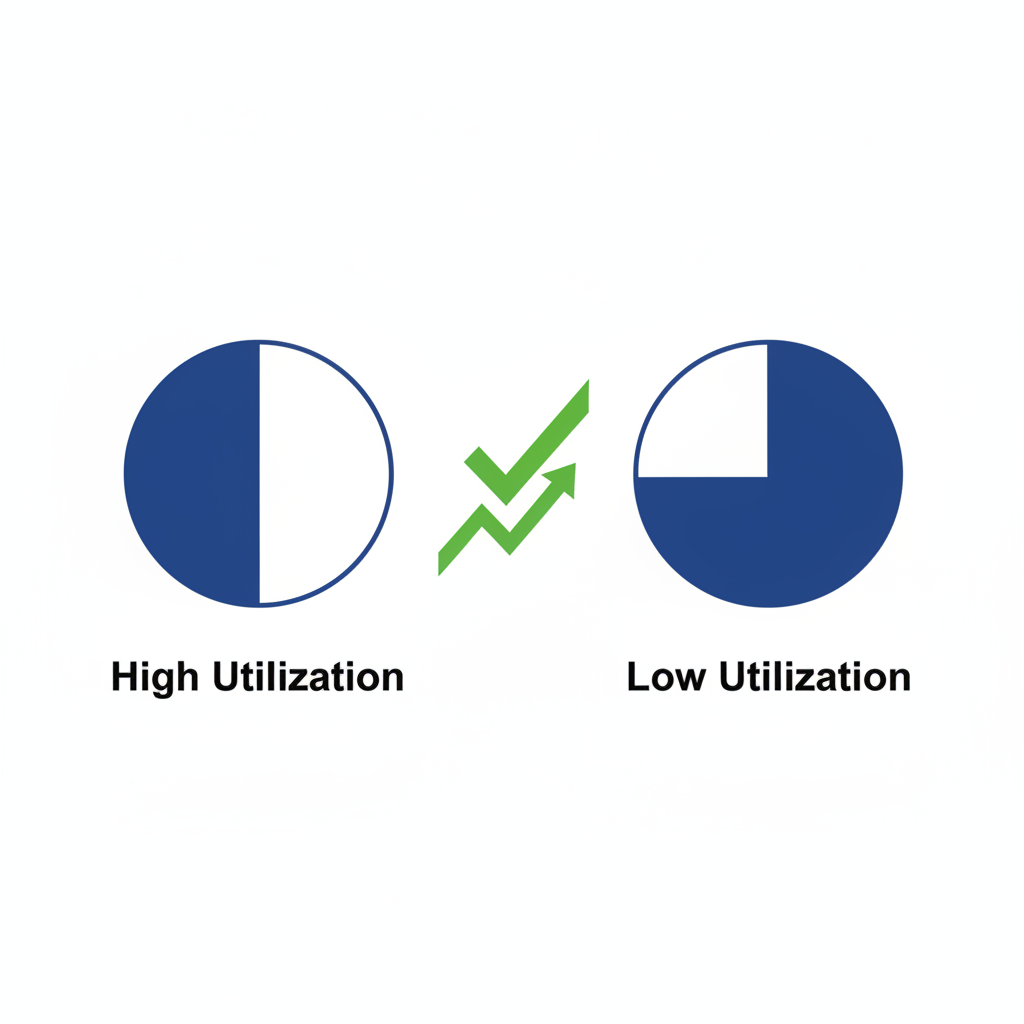

Before we get into the ‘how,’ you need to understand the ‘why.’ The single biggest factor this trick influences is your Credit Utilization Ratio (CUR). This is the percentage of your available credit that you’re currently using, and it makes up a whopping 30% of your credit score. Lenders get nervous when they see you maxing out your cards. A low CUR screams ‘financially stable,’ while a high CUR screams ‘risk!’

Let’s break it down with some simple math. Imagine you have one credit card with a $5,000 limit and you carry a balance of $2,000 from month to month for your business expenses.

Your CUR is calculated like this: (Your Balance / Your Limit) * 100

So, ($2,000 / $5,000) * 100 = 40% Utilization.

That’s not great. Most experts recommend keeping your utilization below 30%, and the real pros keep it under 10%. Now, let’s say you use our secret trick to get your limit doubled to $10,000, but your spending stays exactly the same.

New calculation: ($2,000 / $10,000) * 100 = 20% Utilization.

Look at that. Without paying off a single dime, you instantly cut your utilization in half and now look like a financial rockstar to the credit bureaus. Your score goes up, and you didn’t even break a sweat. See the power? It’s not about spending more; it’s about having more room to breathe.

| Scenario | Credit Limit | Balance | Credit Utilization Ratio (CUR) |

|---|---|---|---|

| Before Increase | $5,000 | $2,000 | 40% (High Risk) |

| After Increase | $10,000 | $2,000 | 20% (Low Risk) |

The ‘Soft Pull’ Secret: How to Get What You Want Without the Credit Score Hit

Here’s the core of the strategy. A hard pull (or hard inquiry) happens when a lender checks your credit report to make a lending decision, like when you apply for a new card, a mortgage, or an auto loan. These can temporarily ding your credit score by a few points and stay on your report for two years. We want to avoid these.

A soft pull (or soft inquiry), on the other hand, is a routine check that doesn’t affect your score. Think of it like you checking your own score or a company pre-approving you for an offer. It’s invisible to other lenders.

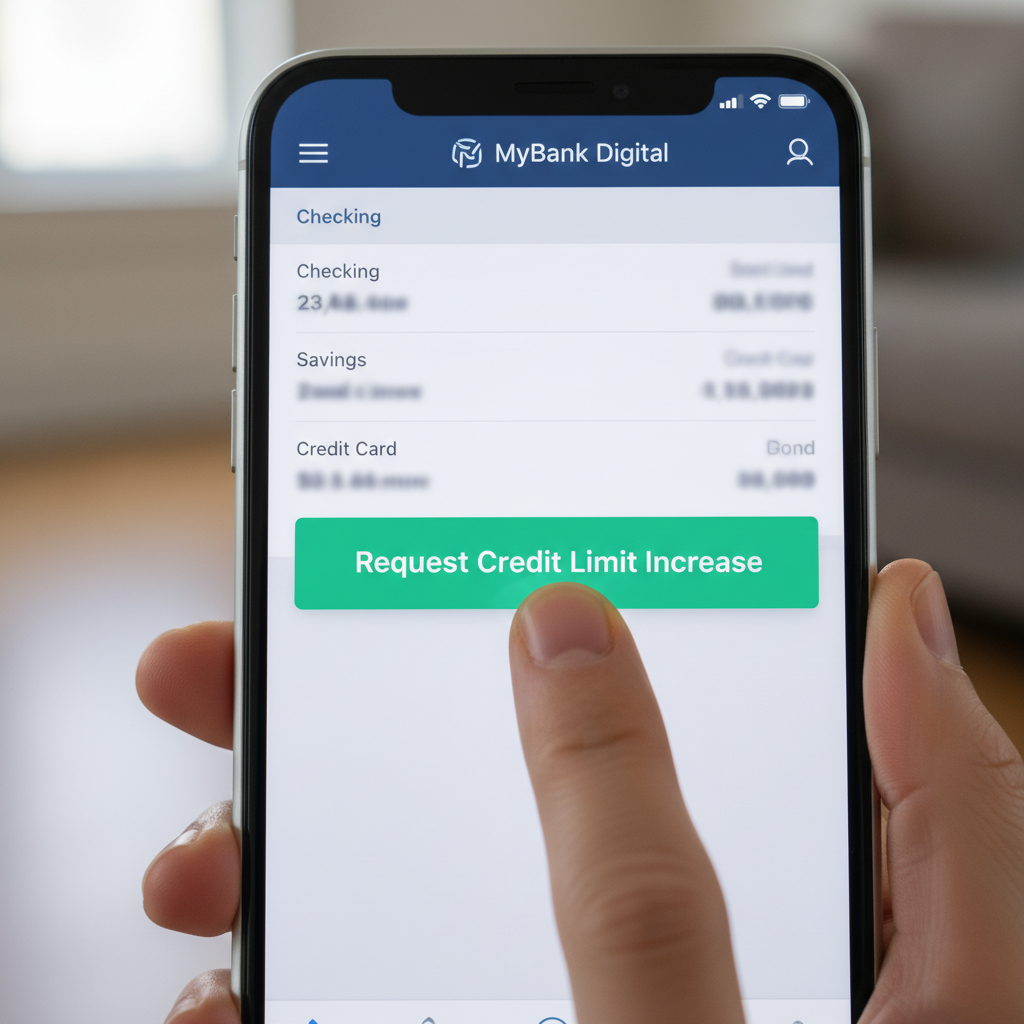

The secret is that most major credit card issuers now have automated systems that let you request a credit limit increase (CLI) right from their website or mobile app. In many cases, especially if it’s a reasonable request and your account is in good standing, their system can approve it instantly based on the data they already have on you—resulting in only a soft pull. You get the reward with zero risk.

Your Action Plan:

- Log In: Go to your credit card’s website or open their mobile app.

- Navigate to Account Services: Look for a menu item like ‘Account Services,’ ‘Card Services,’ or ‘Manage Account.’

- Find the Magic Button: Search for the option that says ‘Request a Credit Limit Increase,’ ‘Credit Line Increase,’ or something similar. It’s often buried in the menus, so be persistent.

- Fill Out the Form: You’ll typically be asked to update your total annual income and maybe your monthly housing payment. Be honest but optimistic. Include income from your side hustles, your partner if it’s a joint household, etc.

- Submit and Wait: Many systems will give you an answer instantly. If approved, your new limit is often available immediately. If they need to review it, you’ll get a notification later.

This digital-first approach is the key. Calling them on the phone or filling out a paper form is more likely to trigger a manual review and a hard pull. Stick to the app or website.

Your Winning Script: Exactly What to Say (or Type) to Get the ‘Yes’

When you fill out that online form, you’re making your case. The most important piece of information you’ll provide is your income. Don’t sell yourself short. Tally up everything: your main job, your side hustle income, investment returns, your spouse’s income if you have shared finances. The higher your stated income, the more credit they’re willing to extend.

Here’s the simple ‘script’ for the online form:

Total Annual Income: [Your total combined household income here. e.g., $85,000]

Monthly Housing Payment: [Your rent or mortgage. e.g., $1,500]

Requested Credit Limit: [Your desired new limit. A good rule of thumb is to ask for 2x your current limit, but no more than $25,000 for most online requests.]

That’s it. No long story needed. The numbers do the talking. If you *do* have to call for some reason, or if you get rejected and call the reconsideration line, your script is just as simple. Be polite, confident, and direct.

Phone Script Example:

“Hi, I’ve been a loyal customer for [Number] years and have maintained a perfect payment history. My financial situation has recently improved, and my income is now [Your Income]. I’m calling to request a credit limit increase on my account to better reflect my current financial standing and to lower my overall credit utilization. I was hoping for a new limit of [Your Desired Limit]. Can you please let me know if this can be processed without a hard inquiry?”

By asking about the hard inquiry, you put them on the spot and show you know the game. Many agents will tell you if it requires one, allowing you to back out if you wish.

Timing is Everything: When to Pull the Trigger for Maximum Success

You can’t just ask for a CLI whenever you feel like it. You need to strike when the iron is hot and you look like their ideal customer. The bank’s algorithm is looking for positive signals. Give them what they want to see.

Your Pre-Request Checklist:

- You’ve Had a Pay Raise or Income Boost: This is the #1 reason they’ll say yes. More income means you can handle more credit. This is your golden ticket.

- You’ve Paid on Time for 6+ Months: Consistency is king. They want to see a solid track record of responsible payments. Never, ever ask if you’ve recently missed a payment.

- You’ve Been Using the Card Responsibly: Show them you’re an active user. Use the card for small purchases and pay it off each month. A dormant card is less likely to get an increase.

- Your Credit Score Has Recently Increased: If you’ve been working on your credit and see a nice jump, that’s the perfect time to leverage that good news.

- It’s Been 6-12 Months Since Your Last Request: Don’t be needy. Asking too often can be a red flag. Give it at least six months between attempts.

Avoid asking right after you’ve opened several new credit cards or taken out a large loan. That activity makes you look ‘credit hungry’ and risky. Be strategic, be patient, and make your move when your financial profile is shining brightest.

The ‘What Ifs’: Handling a Rejection and Dodging Common Pitfalls

So what happens if the computer says ‘no’? Don’t panic. It’s not the end of the world. First, the issuer will mail you a letter explaining the reason for the denial. This is valuable intel. It might be because your income was too low, you have too much existing debt, or your credit history wasn’t long enough. Use this feedback to improve before you try again in six months.

Feeling bold? You can call the bank’s reconsideration line. This connects you with a human credit analyst who can override the computer’s decision. Be polite, explain why you believe you warrant the increase (e.g., “My income has increased significantly, and I want my limit to reflect that”), and plead your case.

The Biggest Pitfall: The Temptation Trap

Getting a higher limit feels good. Seeing that your available credit jumped from $5,000 to $10,000 can trick your brain into thinking you have more money to spend. This is the most dangerous trap, and you have to be smarter than that.

Key Rule: A credit limit is NOT your money. It is a tool. Your spending habits should not change one bit just because your limit did. Continue to only charge what you can afford to pay off in full. The goal here is to improve your financial health, not to go into debt.

Remember the mission: lower your credit utilization, boost your score, and increase your financial flexibility. That’s the win. Don’t turn a strategic victory into a financial failure by falling into the trap of lifestyle inflation.

Conclusion

You now have the playbook. The secret to getting a credit limit increase without a hard pull isn’t some mythical trick; it’s a calculated strategy. It’s about understanding the system, leveraging technology, and timing your move perfectly. By using the bank’s own automated systems, you can significantly boost your credit limit, which will slash your credit utilization, pump up your credit score, and give you the financial breathing room you deserve. This isn’t about spending more—it’s about building more power. Take this knowledge, apply it with discipline, and watch your financial opportunities grow.

Disclaimer: I am not a financial advisor. The information provided in this article is for educational and informational purposes only and does not constitute financial advice. You should consult with a qualified professional before making any financial decisions.