The Fine Print: What Your Credit Card Statement is Hiding From You

Let’s be real. When that credit card statement hits your inbox, you probably do what most people do: you flinch, skim for the total damage, check the minimum payment, and then try to forget about it. But that piece of paper—or that sterile PDF—is more than just a bill. It’s a carefully crafted document designed by banks to confuse you, trip you up, and squeeze every last cent out of you. They’re betting you won’t read the fine print. They’re betting you won’t understand the jargon. And for too long, they’ve been winning that bet.

Not anymore. Consider this your street-smart guide to financial self-defense. We’re pulling back the curtain on the tricks and traps hiding in plain sight on your statement. This isn’t about boring accounting; this is about reclaiming your power and your money. By the time you’re done here, you won’t just be reading your statement—you’ll be x-raying it, spotting the scams from a mile away and turning their own weapon against them. It’s time to learn the hustle.

The Anatomy of the Scam: Decoding Your Statement’s Key Sections

Before you can fight back, you need to know the battlefield. Your statement is broken into sections, each with its own potential for financial pain. Let’s dissect this thing like a pro and expose where the real danger lies.

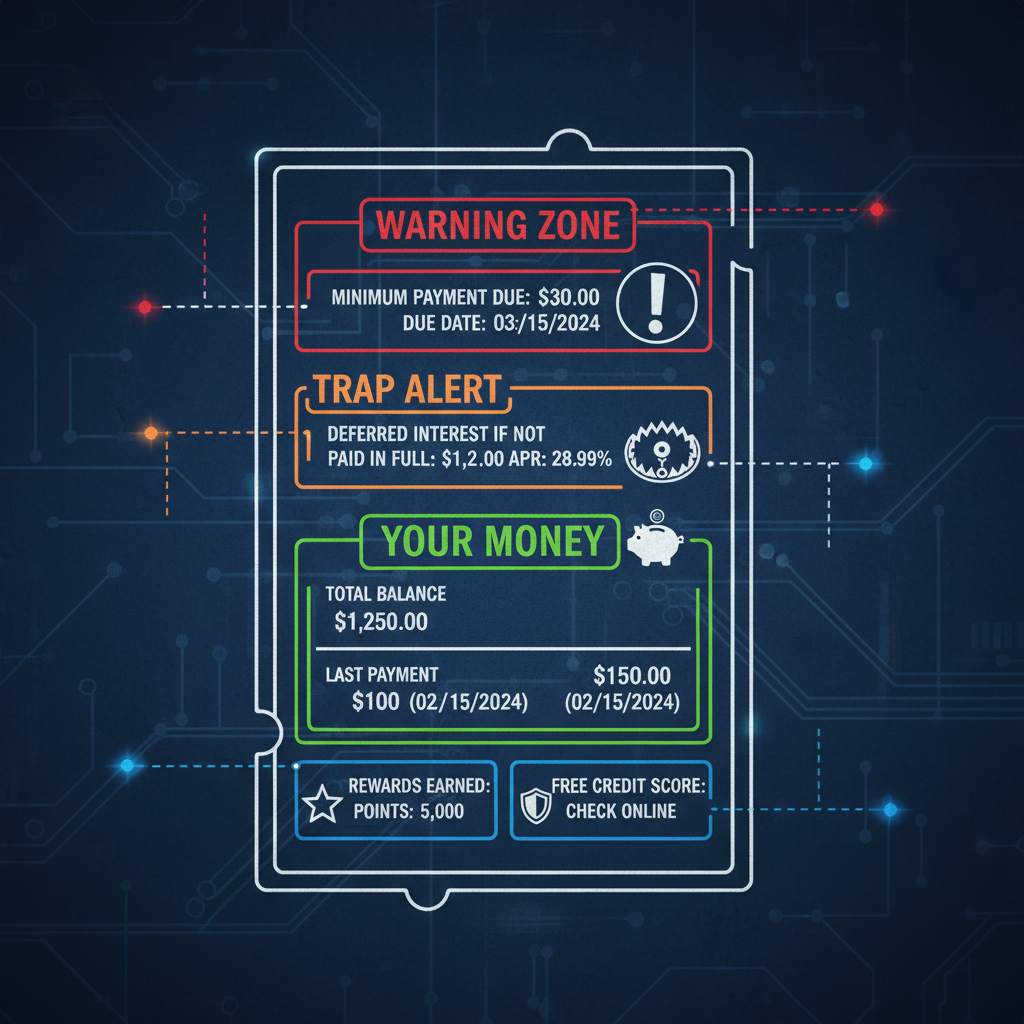

Summary of Account Activity

This is the big picture, the highlight reel of your month’s spending. It lists your previous balance, payments you made (good on you), new purchases, and then the nasty stuff: fees and interest. The number they want you to see is the New Balance. But the numbers you need to actually see are the Fees and Interest Charges. These are the silent parasites draining your account. If these numbers are anything other than $0, that’s a red flag that you’re losing money.

Payment Information: The Minimum Payment Trap

This is ground zero for the biggest hustle in the credit card game. They’ll show you the total amount due and, right next to it, a much smaller, much more tempting number: the Minimum Payment. This isn’t a helpful suggestion; it’s a trap designed to keep you in debt for as long as possible.

Here’s the math they don’t want you to do: Let’s say you have a $3,000 balance on a card with a 21% APR. The minimum payment might be around $90. If you only pay that minimum, guess how long it takes to pay it off? Over 17 years. And you’d end up paying more than $4,500 in interest alone. That’s more than the original debt! You bought $3,000 worth of stuff and paid $7,500 for it. That’s a bad deal, any way you slice it. The minimum payment is the financial equivalent of quicksand—the longer you stay in it, the harder it is to get out.

Interest Charge Calculation: Their Secret Formula

This section is usually a confusing block of text and numbers meant to make your eyes glaze over. Don’t let it. This is where they explain how they calculated the interest they’re charging you. You’ll see terms like ‘Daily Periodic Rate’ and ‘Average Daily Balance.’ Here’s the simple breakdown: they charge you interest every single day on your balance. That’s why credit card debt snowballs so fast. It’s also where you’ll see if you have different APRs for different things. For example, your APR for purchases might be 18%, but the APR for a cash advance could be a brutal 25% or higher, and it starts accruing the second you get the cash. It’s a multi-layered system designed to maximize their profit at your expense.

The Hidden Fees Playbook: Charges They Bank On You Ignoring

Fees are the credit card companies’ bread and butter. They’re the little charges you might not notice, but they add up to billions in profits for the banks. Here are the top offenders to watch out for on your statement.

- Late Payment Fee: This is the most common one. Miss your due date by even an hour, and BAM, you’re hit with a fee, often between $29 and $40. But the real damage is what comes next: this one slip-up can trigger a Penalty APR, which we’ll get to in a minute.

- Annual Fee: Some cards, especially travel and rewards cards, charge you a yearly fee just for having them. This can range from $95 to over $500. You have to be brutally honest with yourself: are the perks you’re getting actually worth more than the fee you’re paying? Do the math. If you’re paying $95 a year but only got $50 worth of rewards, you’re losing.

- Cash Advance Fee: This is one of the worst deals in finance. Need cash from your credit card? Not only will they hit you with an immediate fee (usually 5% of the amount), but they’ll also charge you a sky-high interest rate that starts ticking the moment the cash is in your hand. There’s no grace period. It’s an emergency-only move, and even then, you should avoid it like the plague.

- Balance Transfer Fee: That ‘0% APR for 18 months’ offer looks great, right? But read the fine print. Almost every balance transfer comes with a fee, typically 3% to 5% of the amount you’re moving. Transferring a $5,000 balance with a 4% fee means you instantly pay a $200 toll just to move your debt. It can still be a smart move to save on interest, but it’s not free.

- Foreign Transaction Fee: Using your card overseas? Many cards will tack on a 1-3% fee to every single purchase you make in a foreign currency. It feels like nothing on a $10 coffee, but on a $1,500 hotel bill, that’s an extra $45 for nothing.

The APR Shell Game: How Interest Rates Deceive You

APR, or Annual Percentage Rate, is the price you pay for borrowing money. But it’s not one-size-fits-all. Credit card companies play a shell game with different types of APRs to confuse and trap you. Understanding their game is key to winning.

Introductory APR vs. The Real APR

The ‘0% Intro APR’ is the classic bait-and-switch. They lure you in with a temporary period of no interest. It’s a great tool if you’re disciplined and pay off your balance before the promo period ends. But they are counting on you not to. The second that intro period is over, your remaining balance gets slammed with the regular APR, which could be 20% or more. Always know the exact date the intro period ends and have a plan to be at a $0 balance before that day arrives.

The Penalty APR: Financial Punishment

This is the nuclear option. If you pay late, go over your credit limit, or have a payment returned, the company can punish you by jacking up your interest rate to a ‘Penalty APR.’ This rate is often a nightmare, sometimes as high as 29.99%. And the worst part? They can apply this new, higher rate to your entire existing balance, not just new purchases. One mistake can literally double your interest charges overnight. It’s buried in your cardholder agreement, and it’s one of the most dangerous traps in your statement’s fine print.

Variable Rate Reality

Look for the word ‘(V)’ or ‘Variable’ next to your APR. This means your interest rate is not fixed. It’s tied to a benchmark rate, like the U.S. Prime Rate. When the Federal Reserve raises interest rates, your credit card APR will automatically go up too. You could be making every payment on time and still see your interest rate climb, increasing your cost of borrowing without you doing anything wrong. It’s a reminder that you’re playing in a system where the rules can change on you at any time.

Your Counter-Attack Plan: How to Fight Back and Win

Knowledge is power, but action is everything. Now that you know the tricks, it’s time to go on the offensive. Here’s your step-by-step plan to take control of your statement and your money.

Step 1: Always Pay On Time. No Excuses.

The single best way to avoid fees and penalty APRs is to never be late. The easiest way to guarantee this is to set up automatic payments. At the absolute minimum, set up an autopay for the minimum payment amount. This is your safety net. It ensures you’re never late, even if you forget. You should always plan to pay more, but this protects you from the system’s harshest penalties.

Step 2: Pay More Than the Minimum. Always.

We’ve already seen the minimum payment trap. Your mission is to throw as much money as you can at the balance, especially if it has a high APR. Look at the box on your statement that legally has to show you how long it will take to pay off your balance by only paying the minimum vs. paying a bit more. It’s a powerful motivator.

| Payment Strategy (on a $3,000 balance at 21% APR) | Time to Pay Off | Total Interest Paid |

|---|---|---|

| Minimum Payment Only (~$90/month) | ~17.5 Years | ~$4,580 |

| Fixed Payment of $150/month | ~2.5 Years | ~$850 |

| Fixed Payment of $250/month | ~1.25 Years | ~$460 |

Step 3: Master the Negotiation Script.

Did you get hit with a fee? Don’t just accept it. Call the customer service number on the back of your card. Be polite, but firm. Use this script:

“Hi, I’m reviewing my recent statement and I saw a [late fee / annual fee]. I’ve been a loyal customer for [X years] and my payment history has been excellent. I’m calling to see if it would be possible to have this fee waived as a one-time courtesy.”

You’d be shocked how often this works, especially if you have a good track record. They want to keep you as a customer. The worst they can say is no.

Step 4: Audit Your Statement Every Month.

Make it a habit. Grab a coffee, sit down, and read every single line item. Look for fraudulent charges, check for subscriptions you forgot you were paying for (that free trial that’s now costing you $19.99/month), and verify all the fees and interest charges. This is your money—be its best defender.

Step 5: Use Tech to Your Advantage.

Don’t fight this battle alone. Use a budgeting app like Mint, YNAB, or Copilot. These tools link to your accounts, track your spending, categorize it, and alert you to upcoming due dates. It’s like having a financial watchdog in your pocket, helping you spot problems before they show up on your statement.

Conclusion

Your credit card statement is no longer an instrument of confusion and fear. It’s a report card, a tool, a roadmap. By understanding the game, you can now navigate it with confidence. You know where the traps are, you know how the math works, and you have a plan to fight back against fees and high interest. The power has shifted. Don’t just pay your bill—master it. Pull out your last statement right now and put this guide to work. The money you save is your own.

Disclaimer: I am not a financial advisor. This content is for informational and educational purposes only. Please consult with a licensed financial professional for advice tailored to your individual situation.