What Is Soft Saving? The Gen Z Trend That Makes Budgeting Less Toxic

Let’s be real: traditional budgeting sucks. It’s the financial equivalent of a crash diet. You go all-in, tracking every penny, cutting out every joy, and feeling like a failure when you inevitably ‘cheat’ by buying a latte. It’s a cycle of restriction, guilt, and burnout. But what if there was a way to save money that didn’t feel like a punishment? Enter soft saving.

This isn’t your grandma’s envelope system. Soft saving is the anti-budget, a flexible, intuitive approach to money management championed by a generation tired of toxic financial advice. It’s less about spreadsheets and more about self-awareness. It’s about ditching the rigid rules and instead creating a financial system that aligns with your actual life and values. It’s time to stop fighting your finances and start working with them. This guide will show you how to embrace the soft saving mindset, build real wealth, and finally make peace with your bank account.

Ditching the Budgeting Guilt: What ‘Soft Saving’ Actually Means

At its core, soft saving is about shifting your focus from restriction to intention. Instead of a ‘hard’ budget with dozens of strict categories (e.g., ‘$50 for coffee,’ ‘$200 for groceries’), you focus on a few big-picture goals and give yourself grace everywhere else. It’s a framework, not a cage.

Think of it like this: a hard saver knows they spent $4.75 on a coffee on Tuesday, exceeding their weekly ‘fun’ budget by 3%. A soft saver knows they automatically transferred $100 to their travel fund this week and feels good about making progress on a goal they actually care about. The coffee is just part of life, not a moral failing.

The Golden Rule of Soft Saving: Pay your future self first, then spend the rest without guilt. Focus on the big wins—automating savings for your core goals—and stop sweating the small stuff.

This approach has two key components:

- Values-Based Goals: You don’t just save for a ‘rainy day.’ You define what you actually want your money to do for you. Is it freedom to travel? The security of a down payment? The ability to invest in a side hustle? You identify 2-4 major goals that get you excited. These are your ‘why.’

- Flexibility and Forgiveness: Life happens. An unexpected car repair or a friend’s destination wedding isn’t a budget catastrophe; it’s just life. Soft saving allows you to adapt. Maybe you pause your concert fund savings for a month to cover the repair, no guilt attached. You adjust and move on, rather than scrapping the whole system because you broke a ‘rule.’

The ‘Hard Saving’ Hangover: Why Traditional Budgeting Fails

If you’ve ever felt like a failure at budgeting, congratulations—you’re normal. The rigid, all-or-nothing approach of traditional ‘hard saving’ is designed for robots, not humans. It sets people up for failure and creates a toxic relationship with money.

The Burnout Cycle

Hard budgeting often demands intense, upfront effort. You spend hours categorizing past transactions, building complex spreadsheets, and setting unrealistic limits. It feels productive for a week or two, but it’s not sustainable. When you slip up—because you will—the feeling of failure can be so overwhelming that you abandon the budget altogether. This creates a yo-yo effect: a month of intense restriction followed by a month of guilt-ridden overspending.

It Ignores Human Psychology

We aren’t purely logical beings. Our spending is tied to our emotions, our social lives, and our need for occasional joy. A budget that doesn’t allow for spontaneity or simple pleasures is a budget that’s destined to fail. Telling yourself you can’t afford to go out with friends or buy a book you’re excited about leads to feelings of deprivation, which can trigger ‘rebellious’ spending later on. It’s the same reason crash diets often lead to binge eating.

It Creates Financial Anxiety

Constantly tracking every single dollar can be exhausting and anxiety-inducing. It turns money from a tool into a source of constant stress and judgment. Every purchase is scrutinized. This hyper-vigilance doesn’t lead to financial peace; it leads to financial obsession and a constant fear of making a mistake. Soft saving aims to reduce that noise, letting you focus on what truly matters.

The Soft Saving Playbook: A 5-Step Guide to Getting Started

Ready to try a kinder, more effective way to manage your money? Forget the spreadsheets. Here’s the step-by-step playbook to implementing soft saving in your life.

- Step 1: Define Your ‘Why’. Before you save a dime, you need to know what you’re saving for. Get specific and emotional. Don’t just write ‘Save Money.’ Write ‘Save $3,000 for a two-week trip to Costa Rica to hike and see monkeys.’ Or ‘Save $10,000 for a down payment on a condo so I can finally paint my walls whatever color I want.’ Pick 2-4 big goals that truly motivate you.

- Step 2: Know Your Numbers (The Simple Way). You don’t need to track every penny, but you do need a basic idea of your cash flow. Calculate two things: your total monthly income after taxes, and your total fixed costs (rent/mortgage, utilities, car payment, insurance, subscriptions). The formula is simple: Income – Fixed Costs = Your Flexible Spending/Saving Money. This is the pool of money you have to work with for your goals and daily life.

- Step 3: Pay Your Future Self First (Automate Everything). This is the most critical step. Based on your goals and the number from Step 2, decide how much you can realistically put toward your goals each paycheck. Then, set up automatic transfers from your checking account to separate savings accounts (ideally high-yield ones!). Have the money move the day after you get paid. This way, you’ve already ‘won’ before you have a chance to spend it. If you can automate $200 a month toward your goals, that’s a huge win.

- Step 4: Create Your ‘Guilt-Free’ Spending Account. After your fixed costs are covered and your automated savings are sent away, the money left in your checking account is yours to spend. All of it. On whatever you want. This is the magic of soft saving. Because you’ve already prioritized your future, you can spend the rest without a shred of guilt. No more agonizing over a $15 lunch or a new pair of sneakers.

- Step 5: Check In, Don’t Obsess. Once a month, take 15 minutes to look at your savings progress. Are you on track for your goals? Does anything need to be adjusted? Maybe you got a raise and can bump up your automatic transfers. Maybe you have a tight month and need to briefly pause one of your goals. The point is to make small, intentional adjustments, not to conduct a full-blown audit of every transaction.

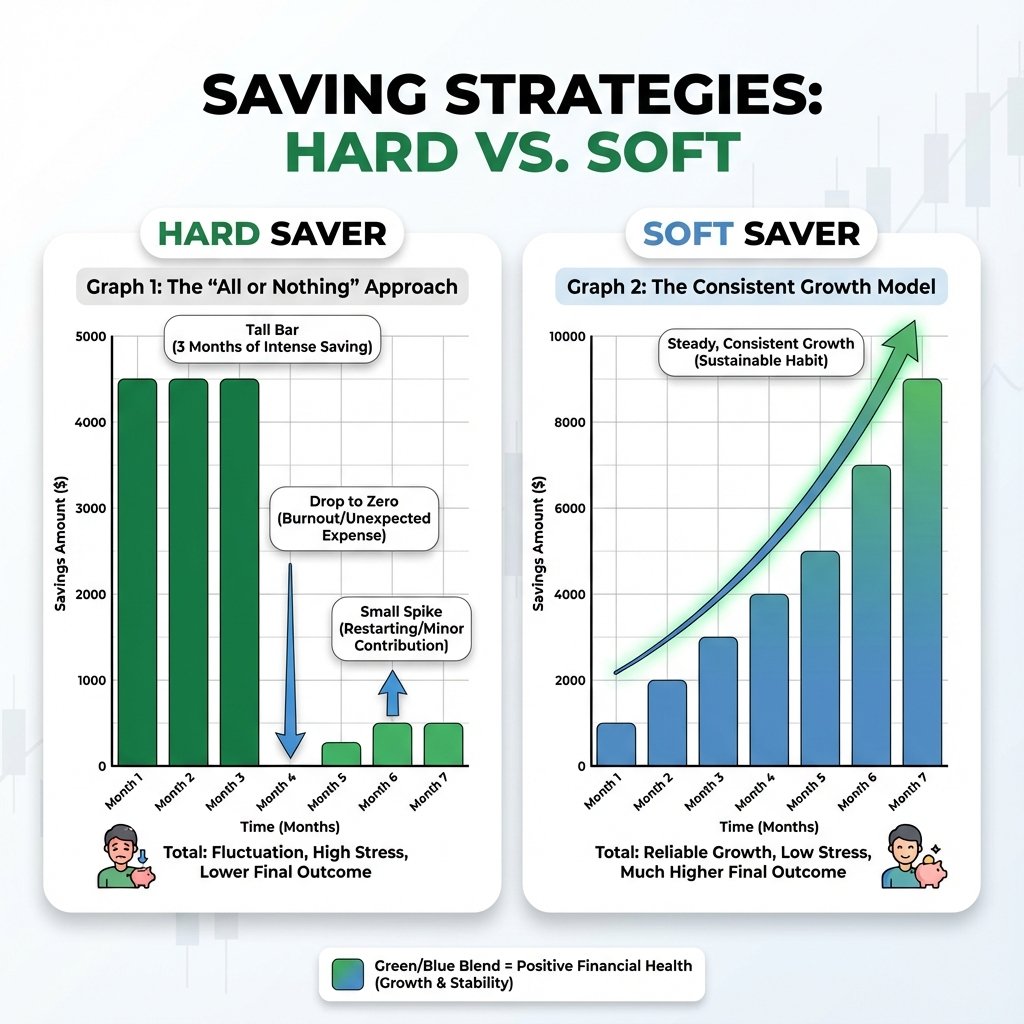

The Math: How Soft Saving Still Builds Serious Wealth

A common critique of softer financial methods is that they’re not aggressive enough. But which is better: a ‘perfect’ plan you abandon after two months, or a ‘good enough’ plan you stick with for five years? Consistency is the secret ingredient to building wealth, and that’s where soft saving shines.

Let’s look at a realistic scenario comparing a Hard Saver who burns out with a consistent Soft Saver over two years.

Case Study: Hard Saver vs. Soft Saver

| Metric | The Hard Saver (Aggressive & Unrealistic) | The Soft Saver (Consistent & Realistic) |

|---|---|---|

| Monthly Savings Goal | $500/month (Cuts out all dining out, hobbies, and ‘fun’ spending) | $250/month (Automated transfer to savings, allows for flexible spending) |

| Months 1-3 | Saves $1,500. Feels deprived and miserable. | Saves $750. Feels good about progress and enjoys life. |

| Month 4 | Burns out. Goes on a $600 ‘rebound’ spending spree and abandons the budget. | Saves another $250. Total saved: $1,000. |

| Months 5-12 | Saves $0. Feels guilty and avoids looking at their bank account. | Saves another $2,000. Total saved: $3,000. |

| Months 13-24 | Tries another ‘hard’ budget for 2 months, saves $1,000, then gives up again. | Saves another $3,000. Total saved: $6,000. |

| Total Saved After 2 Years | $2,500 | $6,000 |

As you can see, the ‘slower’ method wins by a landslide. The Soft Saver built more than double the wealth because their system was sustainable. They weren’t fighting against their own human nature. This is the power of consistency over short-term intensity. Saving just $250 per month consistently adds up to $3,000 in a year and $15,000 in five years—and that’s before any interest or investment growth. Soft saving isn’t about saving less; it’s about saving smarter for the long haul.

Conclusion

The conversation around money is changing. For too long, the only ‘right’ way to manage finances was through restriction, shame, and complicated rules. Soft saving is the antidote. It’s a powerful acknowledgment that your financial health is deeply connected to your mental health.

By prioritizing your biggest goals through automation and giving yourself permission to live your life with the rest, you create a system that’s not only easier to stick with but genuinely more effective in the long run. You’re not lazy for hating your budgeting app; you’re just ready for a more human approach. So ditch the guilt, define what matters to you, and start saving softly. Your future self—and your present self—will thank you for it.