Never Miss A Bill Again: The Half Payment Method Explained Simply

Let’s be real: you know that feeling. It’s a few days before payday, you log into your bank account, and your stomach drops. The rent is due, the car payment is about to hit, and you’re doing the mental gymnastics to make sure you don’t overdraw your account. This is ‘bill dread,’ and it’s a classic symptom of a broken system. The problem isn’t always that you don’t have enough money; it’s that your bills are due on a schedule that has nothing to do with when you actually get paid.

Most of us get paid bi-weekly, but our biggest expenses—rent, mortgage, car loans—demand their cash in one giant lump sum. This creates a feast-or-famine cycle that leaves you feeling broke after one paycheck and flush after the next, all while juggling due dates. But what if you could break that cycle? What if you could smooth out your cash flow so that every paycheck felt the same? That’s not a pipe dream; it’s a simple, powerful strategy called the Half Payment Method. This isn’t about complex spreadsheets or cutting out everything you love. It’s a street-smart hack designed to put you back in the driver’s seat. By the end of this guide, you’ll have a step-by-step action plan to implement this system, eliminate late fees forever, and finally tell bill dread to get lost.

The Breakdown: What Is the Half Payment Method and Why It’s a Game-Changer

So what is this magic trick? It’s shockingly simple. The Half Payment Method involves splitting your major monthly bills into two smaller, more manageable payments. Instead of paying your $1,400 rent in one massive chunk on the 1st, you pay $700 from your first paycheck of the month and the other $700 from your second paycheck. You’re not paying a penny more, but you’re fundamentally changing *how* and *when* you pay.

Think of it like this: you’re aligning your expenses with your income flow. Your money comes in twice a month, so your money goes out twice a month. This simple shift from one big payment to two smaller ones is the key to unlocking financial stability and reducing stress. Why is this such a big deal?

- It Kills ‘Bill Week’ Panic: No more seeing half your paycheck vanish overnight to cover one or two massive bills. Each paycheck takes an equal, predictable hit, leaving you with a consistent amount of cash to work with throughout the month.

- It Eliminates Late Fees: By getting ahead of your due dates with the first half-payment, you drastically reduce the risk of ever missing a payment. A single $35 late fee wiped out is $35 back in your pocket. Do that a few times a year, and the savings add up.

- It Simplifies Budgeting: When your core expenses are the same from paycheck to paycheck, budgeting becomes almost automatic. You know exactly how much is left over for groceries, gas, savings, or fun money, without complex calculations.

- It Gives You Breathing Room: This method creates a buffer. If an unexpected expense pops up, you have more flexibility because you haven’t just drained your account to pay the rent. It’s a built-in emergency cushion that reduces the need to reach for a credit card.

This isn’t just about moving numbers around. It’s a psychological shift. You move from being reactive—scrambling when bills are due—to being proactive and in control. You dictate the terms of your cash flow, not your billing companies.

The Math: How This Hack Smooths Out Your Cash Flow

Talk is cheap. Let’s look at the actual numbers to see how this plays out in the real world. We’ll use a common scenario: you earn $1,500 every two weeks ($3,000/month), and your major bills are all due in the first week of the month.

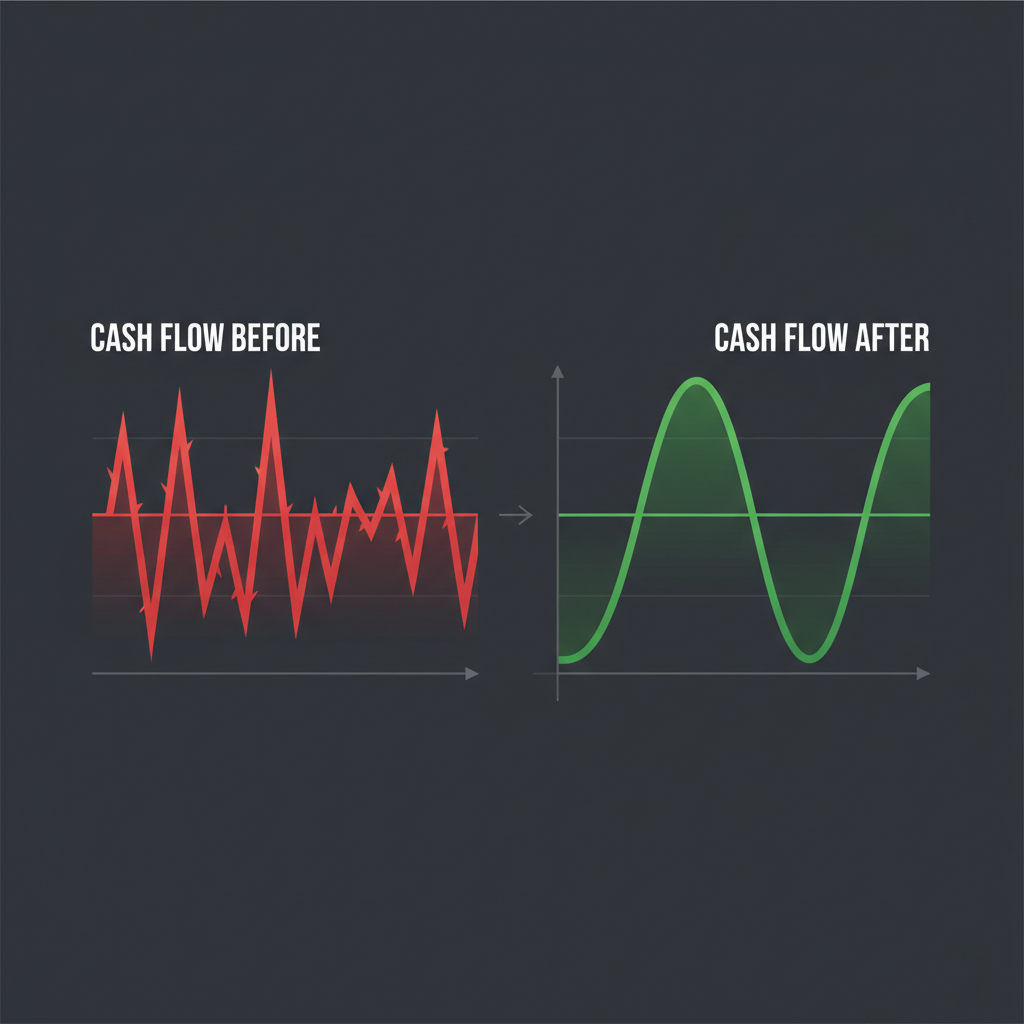

Before: The Standard Bill-Paying Rollercoaster

Your bills are stacked against you. Your biggest expenses hit right after your first paycheck, leaving you scraping by for two weeks.

| Paycheck & Bills | Cash In | Cash Out | Remaining Cash |

|---|---|---|---|

| Paycheck #1 (Day 1) | +$1,500 | $1,500 | |

| Rent (Day 1) | -$1,200 | $300 | |

| Car Payment (Day 5) | -$350 | -$50 (Overdraft!) | |

| Paycheck #2 (Day 15) | +$1,500 | $1,450 | |

| Utilities & Phone (Day 20) | -$250 | $1,200 |

Look at that. After the first paycheck, you’re not just broke; you’re in the red. You have to wait for your second check to cover basic living expenses. This is maximum stress.

After: The Half Payment Method in Action

Now, let’s apply the hack. You split the Rent ($600/$600) and the Car Payment ($175/$175). You arrange to pay the first halves with your first check and the second halves with your second check.

| Paycheck & Bills | Cash In | Cash Out | Remaining Cash |

|---|---|---|---|

| Paycheck #1 (Day 1) | +$1,500 | $1,500 | |

| Half Rent | -$600 | $900 | |

| Half Car Payment | -$175 | $725 | |

| Paycheck #2 (Day 15) | +$1,500 | $2,225 | |

| Half Rent | -$600 | $1,625 | |

| Half Car Payment | -$175 | $1,450 | |

| Utilities & Phone | -$250 | $1,200 |

The difference is night and day. After your first paycheck, you still have $725 left for groceries, gas, and life. After the second, you have a healthy $1,200. There’s no overdraft, no panic, no waiting for the next deposit to feel financially stable. The total money is the same, but your control over it is infinitely greater. This is how you stop living paycheck to paycheck, even with the same income.

Your Action Plan: Setting It Up in Under 30 Minutes

Ready to make this happen? Good. This isn’t theory; it’s an action plan. You can get this entire system set up in less time than it takes to watch an episode of your favorite show. Follow these steps exactly.

- List Your Targets: Grab a piece of paper or open a new note on your phone. List your main, fixed monthly bills. We’re talking about the big fish: Rent/Mortgage, Car Payment, Car Insurance, Student Loans, and any other significant recurring payment. Don’t worry about variable bills like electricity just yet.

- Do the Simple Math: Go down your list and divide each bill amount by two. That’s your new magic number for each paycheck. Write it down next to the bill. For example: Rent: $1400 becomes $700 x 2. Car Loan: $380 becomes $190 x 2.

- Make the Call (The Most Important Step): This is where people get nervous, but it’s easy. You need to contact your lenders and service providers. For things like car loans and mortgages, you often can’t just send half the money without them thinking you underpaid. You need to get on the phone or use their online portal. Use this script:

Hi, I get paid bi-weekly and I’m moving to a system where I pay half of my bill from each paycheck to better manage my cash flow. I’d like to schedule a payment for [your half amount] for [date of first paycheck] and a second payment for [your half amount] for [date of second paycheck]. Can you confirm this will keep my account in good standing and that I won’t incur any late fees?

Nine times out of ten, they will be happy to accommodate you. They just want their money. For rent, have a straightforward conversation with your landlord or property manager. Explain your plan; most will be fine with it as long as the full amount is in their account by the due date (e.g., the 1st or 5th of the month).

- Automate Everything: Do not leave this to manual payments. The whole point is to set it and forget it. Go into your online banking portal and set up two recurring automatic payments for each bill. Time the first payment to happen the day after your first payday of the month. Time the second payment for the day after your second payday. Automation is your best friend here—it makes the system foolproof.

- Track and Verify (For the First Month Only): For the first month, keep an eye on your accounts. Make sure the automatic payments go through as scheduled and that your billers reflect the payments correctly. Once you’ve confirmed it’s working smoothly, you can let the automation take over completely.

The Reality Check: Is This Hack Right for You?

This method is a powerhouse, but it’s not a one-size-fits-all solution. Let’s get real about who stands to gain the most and who might need to think twice.

Who It’s PERFECT For:

- The Bi-Weekly Worker: If you get paid every two weeks, this system was practically designed for you. It syncs your expenses perfectly with your income.

- The Clustered-Bill Sufferer: Is the first week of your month a financial warzone? If your rent, car payment, and insurance all hit within days of each other, this method will be a massive relief.

- The Budget-Hater: If you hate complex spreadsheets and tracking every penny, the Half Payment Method automates your biggest expenses, freeing up mental energy.

- The Side Hustler: If your income has some variability, getting half your major bills paid with your first stable paycheck gives you a huge psychological and financial buffer for the rest of the month.

Who Should Be Cautious:

- The Monthly or Weekly Earner: If you get paid once a month, you already have to budget for the full month, so this doesn’t help much. If you’re paid weekly, you might prefer a weekly pro-rated system instead.

- Those with Inflexible Lenders: Some old-school lenders or smaller credit unions might have rigid systems that only allow one payment per month. This is rare, but it’s why Step 3 (making the call) is non-negotiable. Don’t assume; always ask.

- The Disorganized: If you aren’t going to commit to automating the payments, you could create a nightmare of tracking two payments for every bill. This method thrives on automation. If you don’t automate it, don’t do it.

Key Rule: Never assume your biller will be okay with two payments. A 5-minute phone call is all it takes to confirm your plan and avoid any misunderstandings, late fees, or negative marks on your credit report. You can do this yourself, for free. Never pay a third-party service to arrange this for you.

Level Up: Supercharge Your Half Payment Strategy

Once you’ve mastered the basic Half Payment Method, you can use its principles to get even further ahead. These are the pro-level moves that turn a simple cash flow hack into a wealth-building tool.

The ‘Extra Payment’ Mortgage Hack

This is the hidden genius of a bi-weekly system. There are 52 weeks in a year, which means if you’re paid bi-weekly, you get 26 paychecks. By paying half of your mortgage with each of those 26 paychecks, you end up making 13 full monthly payments by the end of the year, not 12. That one extra payment goes directly to your loan’s principal. The result? You can shave years off your mortgage and save tens of thousands of dollars in interest over the life of the loan. Check with your mortgage lender to ensure extra payments are applied to the principal.

Create a ‘Bill Vortex’ Account

Want to make your bill paying truly untouchable? Open a separate, no-fee online checking account. Nickname it your ‘Bill Account’ or ‘Bill Vortex.’ Here’s how it works:

- Calculate the total of all your half-payments for one paycheck. Let’s say it’s $950.

- Set up an automatic transfer from your main checking account to your Bill Vortex for $950 the day after every payday.

- Set up ALL your automatic bill payments to pull from this Bill Vortex account, not your main account.

Now, your bill money is completely firewalled. You can’t accidentally spend it because it’s not in your main account. It’s a simple, elegant way to guarantee your bills are always covered.

Sync with Credit Card Rewards

If you pay your bills with a credit card to earn points or cashback (and you should, as long as you pay it in full), you can apply the same logic. Instead of waiting for the statement’s due date, make a half-payment to the credit card after your first paycheck and the second half after your second paycheck. This has a bonus effect: it helps keep your credit utilization ratio lower throughout the month, which can give your credit score a nice little boost.

Conclusion

The Half Payment Method isn’t financial wizardry. It’s a practical, no-nonsense strategy for taking back control. It’s about smoothing out the chaotic rollercoaster of your monthly finances and replacing it with a predictable, manageable system. By aligning your biggest expenses with your income schedule, you dismantle the power that due dates have over your life and your stress levels.

You don’t need more money to feel more in control; you need a better system. This is that system. Stop letting your bills dictate your life. Take the 30 minutes today to make the calls, set up the automations, and implement this plan. By your next paycheck, you’ll feel the difference. You’ll feel the breathing room. You’ll feel the power of telling your money exactly where to go. You’ve got this.

Disclaimer: I am not a financial advisor. The information in this article is for educational purposes only and should not be considered financial advice. Please consult with a qualified professional before making any financial decisions.