Freelancer Panic? How To Budget Irregular Income Without The Stress

Let’s be real. The freelancer life is sold as a dream of freedom—working from a laptop on a beach, being your own boss, endless flexibility. But they conveniently leave out the part where you’re staring at your bank account at 3 AM, heart pounding, because you just landed a $5,000 project but have no idea when the next one will hit. That’s the ‘feast or famine’ cycle, and it’s a brutal, anxiety-inducing rollercoaster that can make you question everything.

If you’ve ever felt that pit in your stomach during a dry spell or blown through a huge payment with nothing to show for it, you’re not alone. But here’s the street-smart truth: irregular income does not have to equal irregular stress. The problem isn’t your fluctuating cash flow; it’s the outdated, employee-mindset budget you’re trying to force on it.

Forget everything you think you know about traditional budgeting. This isn’t about meticulously tracking every penny or giving up lattes. This is about a power shift. It’s about building a financial fortress so you can weather any storm, a system so solid you can finally enjoy the freedom you set out to achieve. It’s time to stop being a victim of your income stream and start acting like the CEO of your own life. This guide will show you exactly how.

The Mindset Shift: From Paycheck Panic to CEO Control

The single biggest mistake freelancers make is treating their earnings like a paycheck. You get a payment from a client, it hits your personal checking account, and you think, ‘Great, I’m rich this month!’ Then you pay your bills, splurge a little, and panic when the well runs dry. This has to stop. You are not an employee of your clients; you are a business owner. Your business has revenue, and you, the CEO, need to pay yourself a salary.

Repeat after me: All money that comes in is business revenue, not my personal income.

This mental separation is the foundation of everything. When you see that $3,000 deposit as ‘revenue,’ you’re less likely to immediately earmark it for a new gadget. Instead, you’ll see it as capital that needs to be managed intelligently. Your business—that’s You, Inc.—has obligations: taxes, business expenses, and most importantly, your own salary. By creating this mental (and physical) distance between your business earnings and your personal spending money, you remove the emotion from the equation. High-income months don’t lead to reckless spending, and low-income months don’t trigger a full-blown crisis, because your personal ‘paycheck’ remains stable. This is the first and most critical step to taking back control. It’s about building a system that serves you, not the other way around.

The Three-Bucket System: Your Financial Command Center

Theory is great, but you need an actionable system. This is it. The Three-Bucket System is your new command center, and it’s brutally effective because of its simplicity. You’ll need three separate bank accounts. Yes, three. This isn’t negotiable. Most online banks let you open new accounts for free, so there are no excuses.

Bucket 1: The Revenue Tank (Your Business Checking Account)

This is where every single dollar from every client, gig, and side hustle gets deposited. All your business revenue flows into this one account. This account’s sole purpose is to be a holding tank. You do NOT pay personal bills from here. You do NOT buy groceries from here. This is the headquarters of You, Inc. Its job is to collect the cash so you, the CEO, can decide how to allocate it.

Bucket 2: The ‘Pay Yourself’ Fund (Your Personal Checking Account)

This is where your ‘salary’ lives. On a set schedule—I recommend the 1st and 15th of the month, just like a traditional job—you transfer a fixed, consistent amount from your Revenue Tank (Bucket 1) to this account. This is the money you live on. It pays your rent, your bills, your fun money—everything. How much? We’ll calculate that in the next section, but the key is consistency. Whether you earn $10,000 or $1,000 in a month, you pay yourself the exact same amount. This is how you kill the rollercoaster.

Bucket 3: The Fortress (Your High-Yield Savings Account)

This is your defense system. Every time a payment hits your Revenue Tank, before you do anything else, you immediately transfer a set percentage into this account. This bucket is for two things: taxes and long-term savings. A good starting point is 30%. So if a $1,000 payment comes in, $300 goes straight to The Fortress. This money is not to be touched for anything else. It sits there, earning interest, waiting for Uncle Sam and your future self. This single habit will save you from the number one freelancer nightmare: a massive, unexpected tax bill.

This isn’t just budgeting; it’s cash flow management for your business. You are separating your business’s finances from your personal finances, which is the cornerstone of long-term stability.

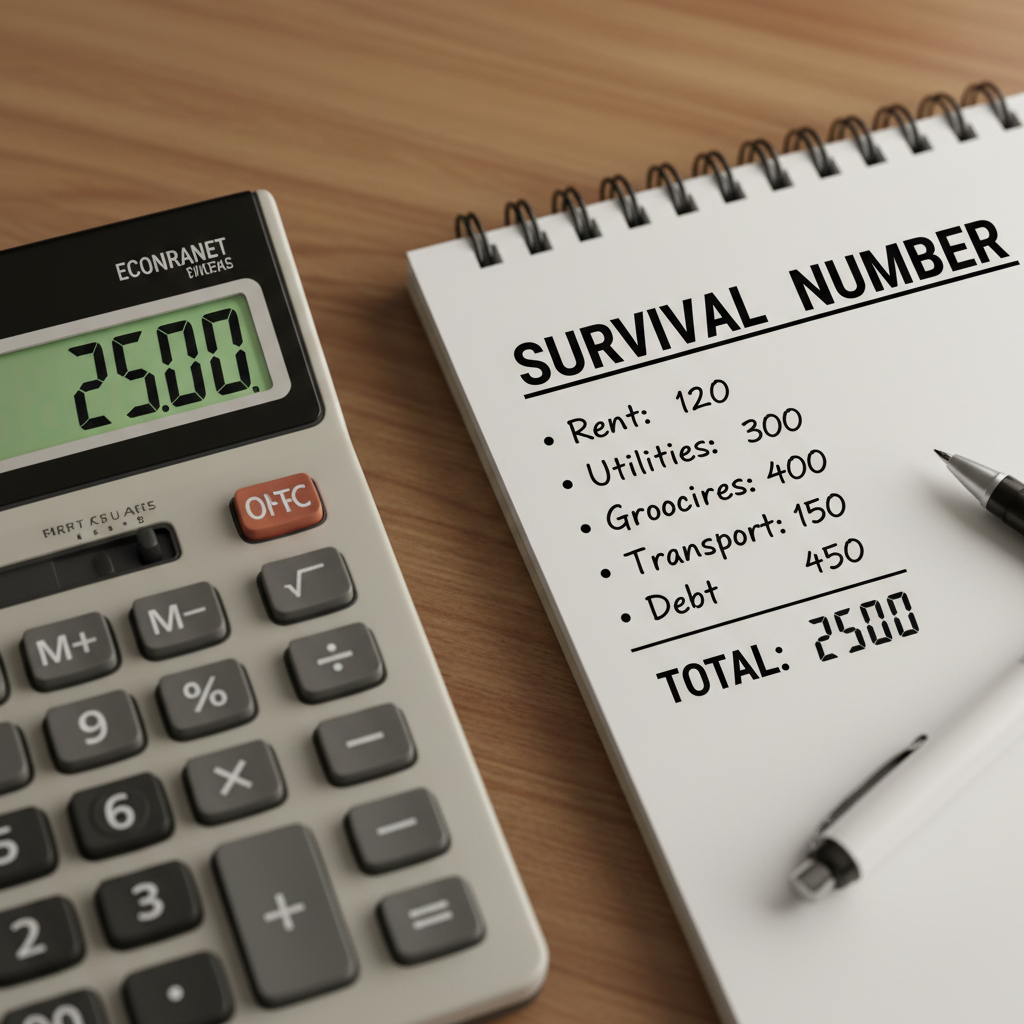

The Bare-Bones Budget: Nailing Down Your Survival Number

Your ‘Pay Yourself’ amount can’t be a random number you pluck from the air. It needs to be based on reality. And that reality starts with your ‘Survival Number’—the absolute minimum amount of money you need to keep the lights on and a roof over your head each month. This is not your ‘thrive’ number; it’s the baseline. Knowing this number with 100% certainty gives you immense power and clarity.

To find it, you need to be brutally honest. Track your spending for a month or go through your last few bank statements. Add up only the absolute essentials. We’re talking about the non-negotiables:

- Housing: Rent or mortgage payment.

- Utilities: Electricity, water, gas, internet (yes, internet is essential for most freelancers).

- Food: A realistic grocery budget, not your ‘eating out every night’ budget.

- Transportation: Gas, public transit pass, or essential car maintenance.

- Insurance: Health, car, renters insurance.

- Debt Minimums: The minimum required payments on any loans or credit cards.

Anything else—subscriptions, gym memberships, entertainment—is cut for this calculation. Your Survival Number is the financial floor. It’s the amount your ‘Pay Yourself’ salary must cover, no matter what. Once you have this number, you can decide on your actual salary. A good starting point is Survival Number + 20% for some breathing room and minor variable spending.

| Expense Category | Estimated Monthly Cost |

|---|---|

| Rent/Mortgage | $1,200 |

| Utilities (Electric, Water, Internet) | $250 |

| Groceries (Basic) | $400 |

| Transportation (Gas/Transit) | $150 |

| Insurance (Health & Car) | $300 |

| Student Loan Minimum | $150 |

| TOTAL SURVIVAL NUMBER | $2,500 |

In this example, your baseline is $2,500. You might decide to pay yourself a salary of $3,000 per month ($2,500 + 20% buffer). This $3,000 is the number you transfer from your Revenue Tank to your Personal Account. Now you have a concrete, data-driven salary to work with.

Taming the Famine: Building Your Freelancer Freedom Fund

A standard emergency fund is great. A freelancer emergency fund is a non-negotiable weapon against anxiety. We call it the ‘Freedom Fund’ because that’s what it buys you: the freedom to say no to bad clients, the freedom to survive a slow month without panicking, and the freedom to take a sick day without watching your finances crumble. This fund is your buffer between you and disaster.

Your goal is to save 3 to 6 months’ worth of your Survival Number expenses in a separate, high-yield savings account. Using the example from before, with a Survival Number of $2,500, your goal is between $7,500 and $15,000.

That might sound daunting, but you have a secret weapon: feast months. Here’s how you build it aggressively:

- Prioritize It: Building this fund is Priority #1 after you’ve implemented the bucket system. It comes before paying off extra debt (besides minimums), before investing, and definitely before lifestyle upgrades.

- Use Windfalls: When you have a massive month and your Revenue Tank (Bucket 1) starts to swell, it’s tempting to give yourself a raise. Don’t. Not yet. After you’ve paid yourself your regular salary and set aside your tax percentage, funnel as much of the surplus as possible directly into your Freedom Fund until it’s full.

The Math of Peace of Mind

Let’s say your salary is $3,000 and your tax set-aside is 30%. This month, you have a killer month and bring in $8,000 in revenue.

- Step 1: $8,000 hits your Revenue Tank.

- Step 2: Immediately move 30% ($2,400) to The Fortress (Bucket 3).

- Step 3: Pay yourself your normal $3,000 salary into your Personal Account (Bucket 2).

- Step 4: You now have a surplus of $2,600 ($8,000 – $2,400 – $3,000) sitting in your Revenue Tank. Instead of blowing it, you transfer that entire $2,600 straight to your Freedom Fund.

By doing this consistently, you’ll build a cash cushion that completely changes the game. A client paying late is no longer a catastrophe; it’s a minor annoyance. A slow month is a chance to work on your business, not a reason to panic.

Hacking the Feast: A Smart Plan for Windfall Months

The ‘famine’ is scary, but the ‘feast’ is dangerous. A huge influx of cash can lead to ‘lifestyle creep’ and reckless decisions that leave you just as broke as before, only with more expensive habits. When a big check hits and your Revenue Tank is overflowing—even after filling your Freedom Fund—you need a plan. This is your waterfall. Money flows down this list, and you don’t move to the next step until the one above it is complete.

- Taxes First, Always. We’ve said it before, but it bears repeating. The moment the money hits, calculate your percentage (e.g., 30%) and move it to The Fortress. This money was never yours; it belongs to the government. Getting this out of sight and out of mind immediately prevents you from accidentally spending it.

- Fortify Your Freedom Fund. Is your 3-6 month buffer fully funded? If not, any surplus revenue goes here until it is. No exceptions.

- Annihilate High-Interest Debt. If you have credit card debt with a 20%+ APR, that’s not just a bill; it’s a five-alarm fire. Use your surplus to attack this debt with overwhelming force. Every dollar you put toward it is a guaranteed 20%+ return. You can’t beat that anywhere else.

- Invest in Your Future Self. Once your high-interest debt is gone and your Freedom Fund is solid, it’s time to pay your future self. Open a retirement account designed for the self-employed, like a SEP IRA or a Solo 401(k). Start contributing a percentage of your surplus here. This is how you build long-term, life-changing wealth.

- Invest in Your Business. Is there a course that could help you command higher rates? A piece of software that could save you hours each week? A new laptop that isn’t on its last legs? Reinvesting in your business is an investment in your future earning potential.

- Enjoy It (Guilt-Free). This is the last step for a reason. Only after you have handled all your other obligations should you take a planned portion of the surplus and enjoy it. Buy the new shoes, take the weekend trip, enjoy a fancy dinner. Because you’ve handled your business first, you can spend this money with zero guilt or anxiety, which makes it feel ten times better.

Conclusion

Living with an irregular income is a reality for millions of us, but living with constant financial stress is a choice. The panic you feel isn’t because your income is unpredictable; it’s because your system is nonexistent. By shifting your mindset from employee to CEO, implementing the Three-Bucket System, and having a clear plan for both feast and famine months, you take back the power.

This isn’t about restriction. It’s the ultimate form of freedom. It’s the freedom to know your bills are covered, your taxes are handled, and a slow month won’t sink you. It’s the freedom to build real wealth, not just live payment-to-payment. You have the hustle, the talent, and the drive to make it as a freelancer. Now you have the financial game plan to match. Stop letting your bank account be the boss. It’s time to build your fortress, pay yourself what you’re worth consistently, and finally run your financial life with the confidence of the CEO you truly are.