Paycheck to Paycheck Freedom: The Biweekly Budget Plan That Finally Works

Let’s be real. That sinking feeling a few days before payday? The constant stress of juggling due dates and hoping your account doesn’t dip into the red? That’s the reality of the paycheck-to-paycheck grind. You’ve probably tried the standard monthly budget. You download the app, you fill out the spreadsheet, and two weeks later, it’s a total mess. Why? Because you’re using the wrong playbook.

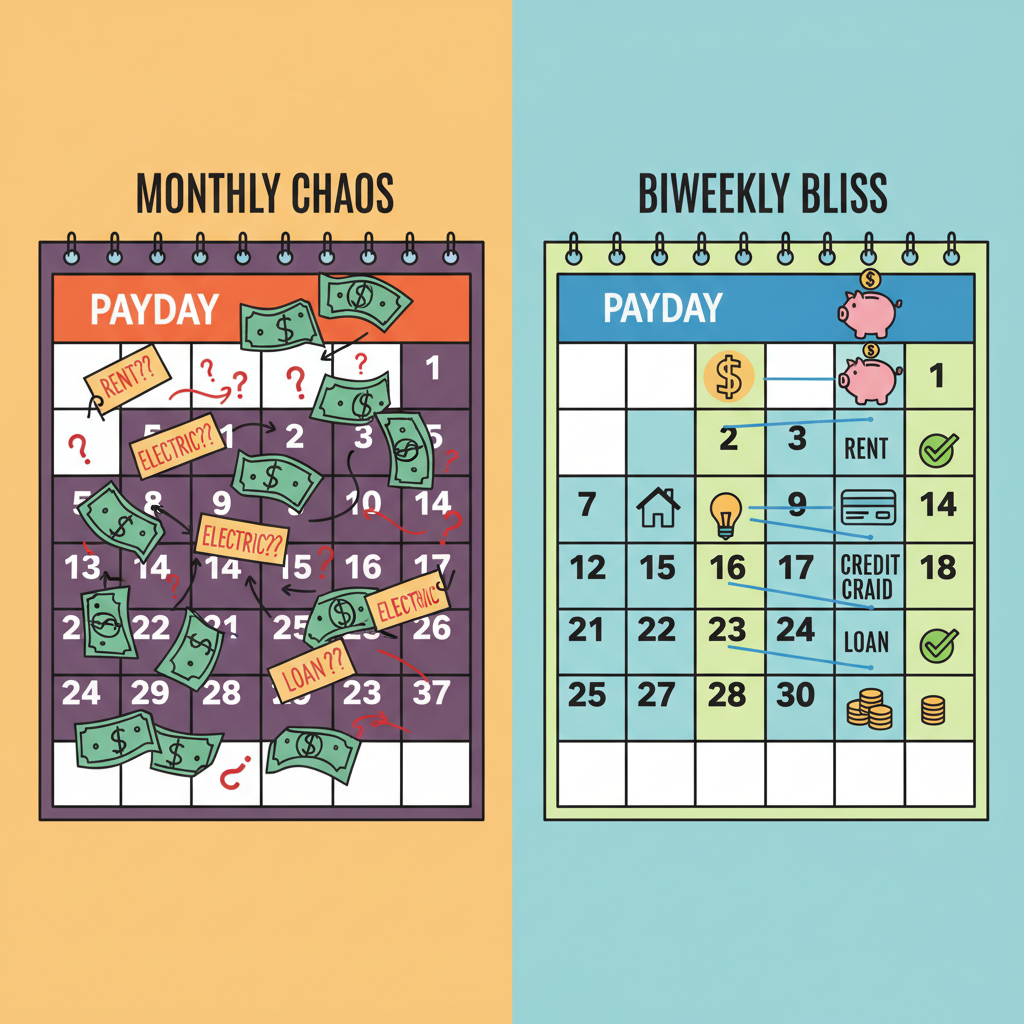

Monthly budgets are a trap for anyone paid biweekly or weekly. They force you to manage 30 days of expenses with money that only shows up every 14. It’s a recipe for failure that leaves you feeling broke and defeated. But what if you could align your budget with your actual cash flow? That’s not a fantasy; it’s the biweekly budget plan. This is the street-smart system that puts you back in the driver’s seat. No fluff, no complicated software—just a straightforward strategy to break the cycle for good.

Why Your Monthly Budget Is Sabotaging You

Why Your Monthly Budget Is Sabotaging You (And How the Biweekly Plan Fixes It)

Trying to make a monthly budget work when you get paid every two weeks is like trying to navigate a city with a map of a different country. It’s fundamentally mismatched and designed to make you fail. You get paid on the 5th, you feel rich. You pay your rent and a couple of other big bills. By the 15th, you’re scraping by, anxiously waiting for that next deposit on the 19th. This is the ‘feast or famine’ cycle, and it’s exhausting.

The core problem is a cash flow mismatch. Your expenses are spread across 30-31 days, but your income arrives in powerful, concentrated bursts. A monthly budget ignores this rhythm. It treats all your income for the month as one big pot of money, which is a lie. That money isn’t all there on the 1st. The biweekly method fixes this by breaking your massive, intimidating monthly budget into smaller, manageable, two-week sprints. You only budget the money you actually have in hand for the next two weeks. It’s about clarity and control, not confusion and anxiety.

The Setup: Your Biweekly Budget Blueprint

The Setup: Your Biweekly Budget Blueprint

Alright, let’s build this thing. No fancy apps required unless you want them. All you need is a calendar (digital or paper) and a way to list things out. This is about taking action, not getting bogged down in details.

Step 1: Map Your Paychecks & Bills

First, grab a calendar and mark every single payday for the next three months. Now, list all your fixed bills—the ones with a set amount and due date. We’re talking rent/mortgage, car payment, insurance, cell phone, internet, and any subscriptions you’re keeping. Assign each bill to the paycheck that falls *right before* its due date. For example, if your rent is due on the 1st and you get paid on the 20th and the 5th, the rent money comes out of the paycheck on the 20th. This stops the scramble.

Step 2: Calculate Your Paycheck Budgets

Now you create a mini-budget for each paycheck. For every payday, take your net take-home pay and immediately subtract the fixed bills you assigned to it. What’s left over is your discretionary fund for that two-week period. This is the money you have for everything else.

Here’s a simple example for someone taking home $1,600 every two weeks:

| Paycheck 1 (Deposited on the 5th) | Amount |

|---|---|

| Net Paycheck Amount | $1,600 |

| Assigned Bill: Car Payment (Due on 10th) | –$350 |

| Assigned Bill: Insurance (Due on 12th) | –$150 |

| Funds for Next 2 Weeks | $1,100 |

| Paycheck 2 (Deposited on the 19th) | Amount |

|---|---|

| Net Paycheck Amount | $1,600 |

| Assigned Bill: Rent (Due on 1st) | –$1,200 |

| Funds for Next 2 Weeks | $400 |

See the difference? Paycheck 1 has more breathing room than Paycheck 2. A monthly budget hides this fact. The biweekly budget puts it front and center so you can plan accordingly.

Step 3: Tame Your Variable Spending

With the remaining funds for each pay period ($1,100 and $400 in our example), you now allocate for your variable expenses. Keep it simple. Focus on the big three: Groceries, Gas, and Flex Spending (this covers everything else—coffee, a movie, takeout). Give every dollar a job. For the $400 paycheck, that might look like: Groceries ($200), Gas ($80), and Flex ($120). You know exactly what you have to work with.

The Math: How Biweekly Budgeting Creates ‘Magic’ Money

The Math: How Biweekly Budgeting Creates ‘Magic’ Money

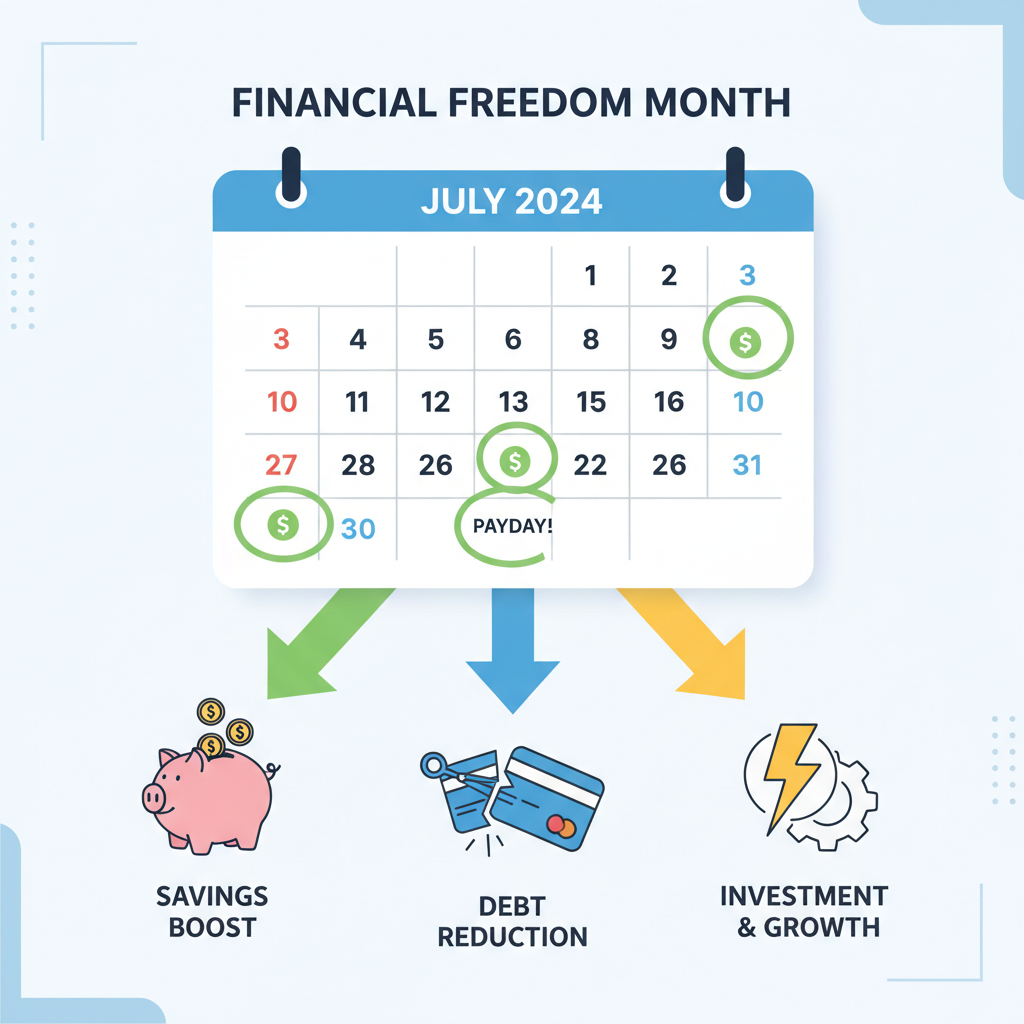

Here’s the part the monthly budget gurus never tell you about, the secret weapon of the biweekly system. If you get paid every two weeks, you receive 26 paychecks a year. But a standard monthly budget is built around 24 paychecks (two per month). This means that twice a year, you’ll have a month with three paychecks. Under a monthly system, this ‘extra’ money gets absorbed and disappears into the chaos. With a biweekly plan, it’s a planned windfall you can use to change your financial life.

Let’s do the math. Using our example of a $1,600 take-home paycheck, those two ‘extra’ checks add up to a whopping $3,200 a year. This isn’t a bonus; it’s *your* money that your old budget was hiding from you. By planning for it, you can make massive progress on your goals. You’re not just surviving anymore; you’re building.

Your ‘Third Paycheck’ Action Plan

When that magic third paycheck hits, it already has a job. You’ve paid all your monthly bills with the first two paychecks of the month. This entire check is pure rocket fuel. Here’s how you could hack it:

| Allocation Goal | Strategy | Amount (from $1,600 check) |

|---|---|---|

| Destroy Debt | Make a huge extra payment on your highest-interest debt (credit card, personal loan). | $800 |

| Build Your F*ck You Fund | Instantly boost your emergency savings. This is your freedom fund. | $500 |

| Get Ahead on Bills | Pay a bill for the *next* month, freeing up future cash flow. | $200 |

| Guilt-Free Spending | Reward yourself. Buy the shoes, go to the concert. You earned it. | $100 |

By giving this money a purpose *before* it even hits your account, you transform it from random cash into a powerful wealth-building tool. This is how you get ahead. This is how you stop being a slave to your bills.

Hacking Your Spending & Staying on Track

Hacking Your Spending & Staying on Track

A plan is useless without execution. The beauty of the biweekly budget is its simplicity, which makes it easier to stick to. Here’s how to make sure you stay on track and master your cash flow within each two-week sprint.

Use the Envelope System (Digital or Physical)

For your variable spending (Groceries, Gas, Flex), physical cash can be a powerful tool. At the start of each pay period, pull out the cash you’ve budgeted for those categories and put it in labeled envelopes. When the money’s gone, it’s gone. It’s a hard stop that a debit card swipe just can’t replicate. Not a cash person? No problem. Use digital envelope apps like Qapital or set up separate free checking accounts for each category. The principle is the same: partition your money so you can’t accidentally spend your grocery money on impulse buys.

Create a ‘Zero-Dollar’ Buffer

This is a game-changer for avoiding overdraft fees and stress. The goal is to build a small buffer in your main checking account—say, $200—that you treat as $0. This money does not exist in your budget. It’s an emergency cushion that sits there to protect you from miscalculations or unexpected auto-drafts. It’s your financial safety net, and it lets you sleep better at night.

The 48-Hour Rule & The Script

For any non-essential ‘Flex’ purchase over $50, enforce a strict 48-hour waiting period. If you still want it just as badly two days later, and it fits in the budget, go for it. This simple rule kills impulse spending. When you’re tempted to break the budget, ask yourself this out loud:

Is this a true ‘need’ or a temporary ‘want’? Does this purchase move me closer to or further from my goal of financial freedom? Can it wait until the next pay period?

It sounds corny, but externalizing the thought process forces you to be honest with yourself. It’s your money, your rules. Stick to them.

Conclusion

Breaking the paycheck-to-paycheck cycle isn’t about earning more money—it’s about gaining more control. The biweekly budget plan is your key to that control. It’s not a restrictive diet for your wallet; it’s a revolutionary way to manage your money that aligns with your life. You’re no longer looking at a massive, overwhelming month. You’re focused on winning the next two weeks. And then the next two after that.

By mapping your bills, planning for your ‘third paycheck’ windfalls, and consciously managing your variable spending, you flip the script. You tell your money where to go instead of wondering where it went. The freedom that comes from that certainty is priceless. So grab a calendar, look at your next payday, and make your first paycheck budget. This is the day you stop surviving and start building.