This 100-Year-Old Japanese Trick Saved Me $5,000 This Year

You’ve tried the apps. The ones with the slick interfaces, the endless notifications, and the monthly subscription fees. They promise to automate your savings, but all they really do is automate your anxiety, linking to your bank accounts and tracking your every move. Let’s be real: most of them are designed to keep you hooked, not to make you wealthy. What if the secret to financial control isn’t in your phone, but in your hands?

Enter Kakeibo (pronounced ‘kah-keh-boh’), the 100-year-old Japanese budgeting method that’s more like a financial martial art than a spreadsheet. It’s a simple, pen-and-paper system that forced me to confront my spending habits head-on. No logins, no syncing, no data breaches. Just pure, unadulterated awareness. And the result? I found an extra $5,000 in my budget this year without getting a raise or starting a new side hustle. This isn’t about restriction; it’s about intention. Forget the tech noise. I’m going to show you how this old-school trick can put you back in the driver’s seat of your financial life.

What Exactly is Kakeibo? (And Why It Crushes Modern Apps)

Before you can master the technique, you have to respect its origin. Kakeibo isn’t some new fad cooked up by a finance influencer. It was created in 1904 by Hani Motoko, one of Japan’s first female journalists. She designed it to empower women to manage their household finances with intelligence and mindfulness. It’s not just a ledger; it’s a philosophy.

The core principle of Kakeibo is that the physical act of writing down your expenses creates a powerful psychological connection to your money. Swiping a card or tapping your phone is abstract and painless. Forcing yourself to write ‘$7.50 – latte and croissant’ makes you pause and consider the transaction. It makes the intangible tangible.

Modern budgeting apps are passive. They categorize your spending after the fact, showing you a pie chart of your failure. Kakeibo is active. It’s a daily ritual that encourages you to think before you spend. It’s about asking simple but profound questions to separate what you truly need from what you momentarily want. This isn’t about shaming yourself; it’s about gathering intel on your own habits so you can make smarter plays with your money. It’s you versus your impulse spending, and Kakeibo is your secret weapon.

The Kakeibo Framework: Your Four-Step Takedown of Wasteful Spending

Kakeibo’s power lies in its structured, monthly ritual. It’s a simple loop that builds momentum and insight over time. Forget complex formulas; this is the street-smart framework that gets results. Here’s how you execute it every single month:

- Step 1: Plan Your Month (The Strategy Session). At the very beginning of the month, sit down with your Kakeibo. Write down your total monthly income. Immediately subtract your fixed, non-negotiable expenses—your ‘must-pays.’ This includes things like rent/mortgage, utilities, car payments, and debt minimums. The number you’re left with is your actual ‘spendable’ income for the month. This is your battlefield.

- Step 2: Set Your Savings Target (The Mission). Look at your spendable income. Now, decide how much you want to save. Don’t just wish for it—commit to a number. Write it down and physically move that amount to a savings account if you can. What remains is the money you have for everything else. This flips the script from ‘save what’s left’ to ‘spend what’s left after saving.’

- Step 3: Track Every Dollar (The Reconnaissance). This is the daily grind, and it’s where the magic happens. Carry your notebook everywhere. Every time you spend money, you write it down. No exceptions. Then, you categorize it into one of four pillars:

The Four Pillars of Spending:

- Survival: The absolute essentials. Groceries (not takeout), housing, transportation to work, utilities.

- Optional: Your wants. Restaurants, bars, hobbies, new clothes, streaming services. Be honest here.

- Culture: Money spent on self-improvement. Books, museum tickets, concerts, online courses.

- Unexpected: The curveballs. Doctor’s visit, car repair, emergency vet bill.

- Step 4: Review and Reflect (The Debrief). At the end of the month (and the end of each week), you analyze your spending. Kakeibo prompts you to answer four key questions: How much money do you have? How much money would you like to save? How much are you actually spending? How can you improve? This isn’t about judgment. It’s about finding the patterns. Where are the leaks? What spending actually brought you joy, and what was just mindless? This reflection is what turns tracking into a powerful tool for change.

The Math: How Kakeibo Found Me a ‘Hidden’ $5,000

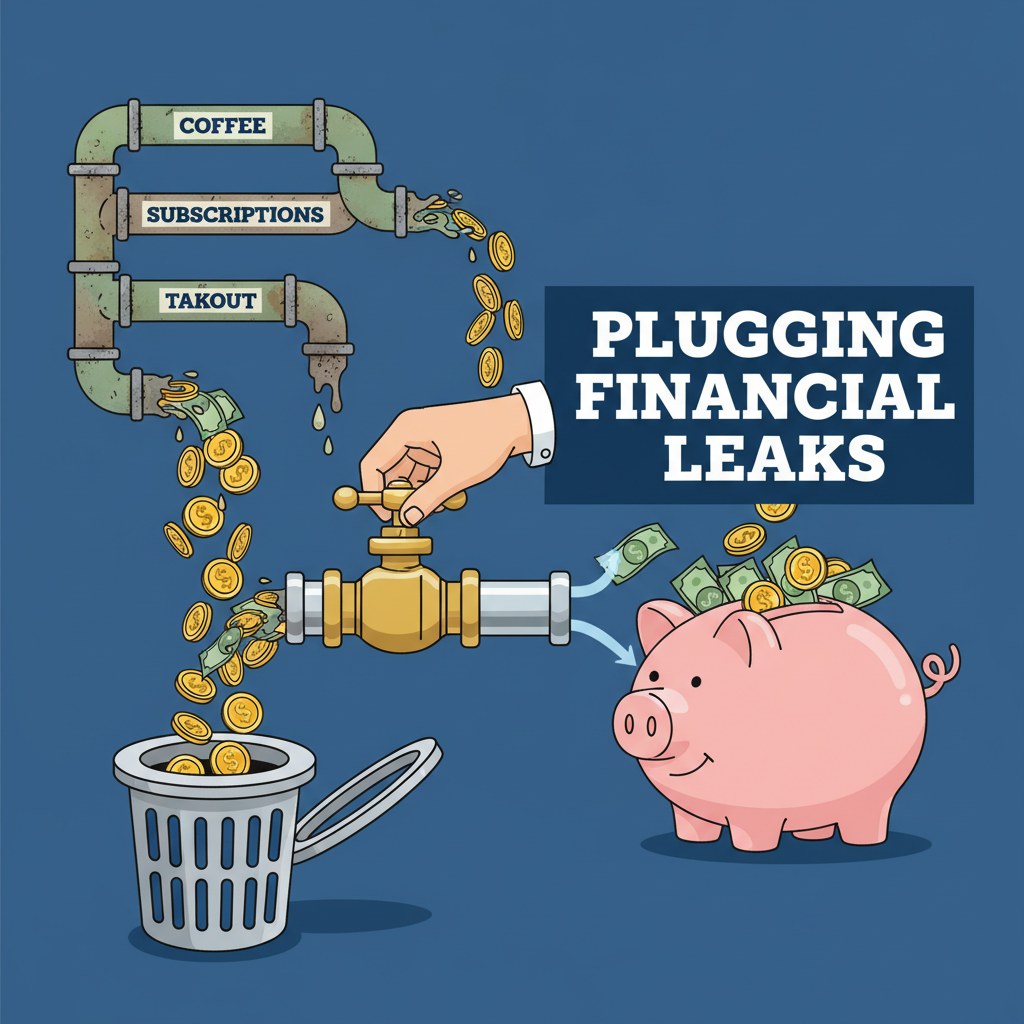

Talk is cheap. Let’s get down to the numbers. The $5,000 I saved wasn’t from some windfall; it was hiding in plain sight, scattered across dozens of small, mindless transactions every month. Kakeibo didn’t magically create more money; it gave me the clarity to see where my money was going and redirect it. Here’s a typical breakdown of how small, mindful changes, identified through Kakeibo, add up to a massive win.

Let’s look at a common scenario. Below is a comparison of a budget with ‘spending leaks’ versus a budget sharpened by Kakeibo’s mindful approach. The difference is staggering.

| Spending Category | ‘Before Kakeibo’ Monthly Cost | ‘After Kakeibo’ Monthly Cost | Monthly Savings |

|---|---|---|---|

| Morning Coffee | $120 ($6 x 20 workdays) | $20 (Home-brewed, occasional treat) | $100 |

| Lunch at Work | $300 ($15 x 20 workdays) | $120 (Packed lunch 4 days/week) | $180 |

| Streaming/App Subscriptions | $65 (Multiple services, some unused) | $20 (Kept the 2 most-used services) | $45 |

| Impulse Online Shopping | $150 (Random Amazon/Target buys) | $50 (Planned, intentional purchases only) | $100 |

| Takeout/Delivery | $200 (2-3 times per week) | $80 (Planned once-a-week treat) | $120 |

Just by focusing on these five common spending leaks, the total monthly savings come to a whopping $545. That’s money that was just evaporating before. Now, let’s look at the annual impact:

$545 (Monthly Savings) x 12 (Months) = $6,540 (Annual Savings)

That’s well over the $5,000 I claimed. And this doesn’t even account for bigger wins, like negotiating a better cell phone plan or cutting back on expensive weekend entertainment—all habits that Kakeibo brings to your attention. The proof is in the math. The money is already there; you just need the right system to see it.

Your Kakeibo Game Plan: Tools & Mindset

Ready to get started? The beauty of Kakeibo is its simplicity. You don’t need to buy an expensive course or a fancy planner (though you can if you want). All you need are a few basic tools and the right mindset to make it stick.

The Toolkit

- A Notebook: Seriously, any notebook works. A simple spiral-bound or a Moleskine will do the job. The goal is function, not fashion. If you want a dedicated Kakeibo ledger, you can find them online, but don’t let the search for the ‘perfect’ notebook stop you from starting.

- A Pen: Find a pen you actually like writing with. It sounds silly, but if the physical act is enjoyable, you’re more likely to stick with it.

- A Quiet Moment: Set aside 5 minutes every evening to log your expenses and 30 minutes at the start of each month to plan. Make it a non-negotiable ritual, like brushing your teeth.

The Mindset for Success

The tools are easy; the mindset is what separates the dabblers from the masters. Engrain these rules into your approach.

Rule #1: Consistency Over Perfection. You will miss a day. You will forget to log a purchase. It’s okay. Don’t throw the whole notebook out. Just pick it up the next day and keep going. The goal is progress, not a flawless record.

Rule #2: No Judgment, Only Data. The first month of Kakeibo can be a shock. You might be horrified to see how much you spend on takeout or subscriptions. Do not beat yourself up. You are not a bad person; you are a detective gathering intelligence. This data is your roadmap to improvement. Treat it as such.

Rule #3: Embrace the Pause. The ultimate goal of Kakeibo is to create a moment of friction between the impulse to buy and the act of buying. Before you tap that card, think to yourself, ‘I’m going to have to write this down later.’ That simple thought is often powerful enough to make you reconsider if you truly need it. That’s the Kakeibo mindset in action.

Conclusion

The financial world wants you to believe that managing your money has to be complicated, automated, and app-based. They sell you convenience at the cost of your awareness and, often, your own data. Kakeibo is the rebellion against that noise. It’s a declaration that you are smarter than any algorithm and that the most powerful financial tool you have is your own attention.

This isn’t just about saving money. It’s about reclaiming control. It’s about transforming your relationship with your finances from one of anxiety and avoidance to one of intention and empowerment. The process of physically writing down your journey with money will teach you more about your habits, dreams, and values than any pie chart ever could. So grab a notebook. Ditch the apps for a month and try it. That $5,000—or whatever your number is—isn’t just a possibility. It’s waiting for you to find it.