12 Stunning Bullet Journal Spreads That Will Make You Actually Want to Budget

Let’s get real for a second. The word ‘budget’ can make you want to run for the hills. It sounds restrictive, boring, and a lot like financial homework you never wanted. Most budgeting apps are soulless, and spreadsheets? They’re the digital equivalent of watching paint dry. They tell you where your money went, but they don’t make you care. That’s why most budgets fail. They lack connection.

But what if you could turn that dreaded chore into a creative ritual? What if tracking your money felt less like a punishment and more like a power move? Enter the bullet journal (BuJo). This isn’t just about making pretty pages with fancy pens—it’s about building a financial command center that’s 100% yours. It’s a hands-on, no-nonsense system that forces you to physically engage with your income and expenses. When you write it down, you remember it. When you can see your progress in a way you designed, you get invested. Forget the digital noise. We’re going analog to give your wallet a serious upgrade. These 12 spreads are your new playbook for financial control.

1. The Monthly Log: Your Financial Command Center

The Hack

This is ground zero. Before you can tell your money where to go, you have to know where it’s currently going. The Monthly Log is a brutally honest look at your spending habits. No complex categories, no fancy software. Just a simple, running list of every single dollar that leaves your pocket. It’s the financial equivalent of turning the lights on in a dark room.

How to Set It Up

It’s dead simple. Create two columns on a fresh page. Label them ‘Date/Description’ and ‘Amount.’ That’s it. For the entire month, log everything. The $5 coffee, the $1.99 app purchase, the $80 tank of gas. Everything. Don’t judge it, just log it. At the end of the month, you’ll have a raw, unfiltered dataset of your financial life.

The Street-Smart Angle

This spread isn’t about shame; it’s about awareness. You’ll quickly spot the patterns. Maybe you’re spending $150 a month on lunches you don’t even like. Maybe four different streaming services are quietly draining your account. This log is the evidence you need to make smarter cuts later. It’s your financial intel.

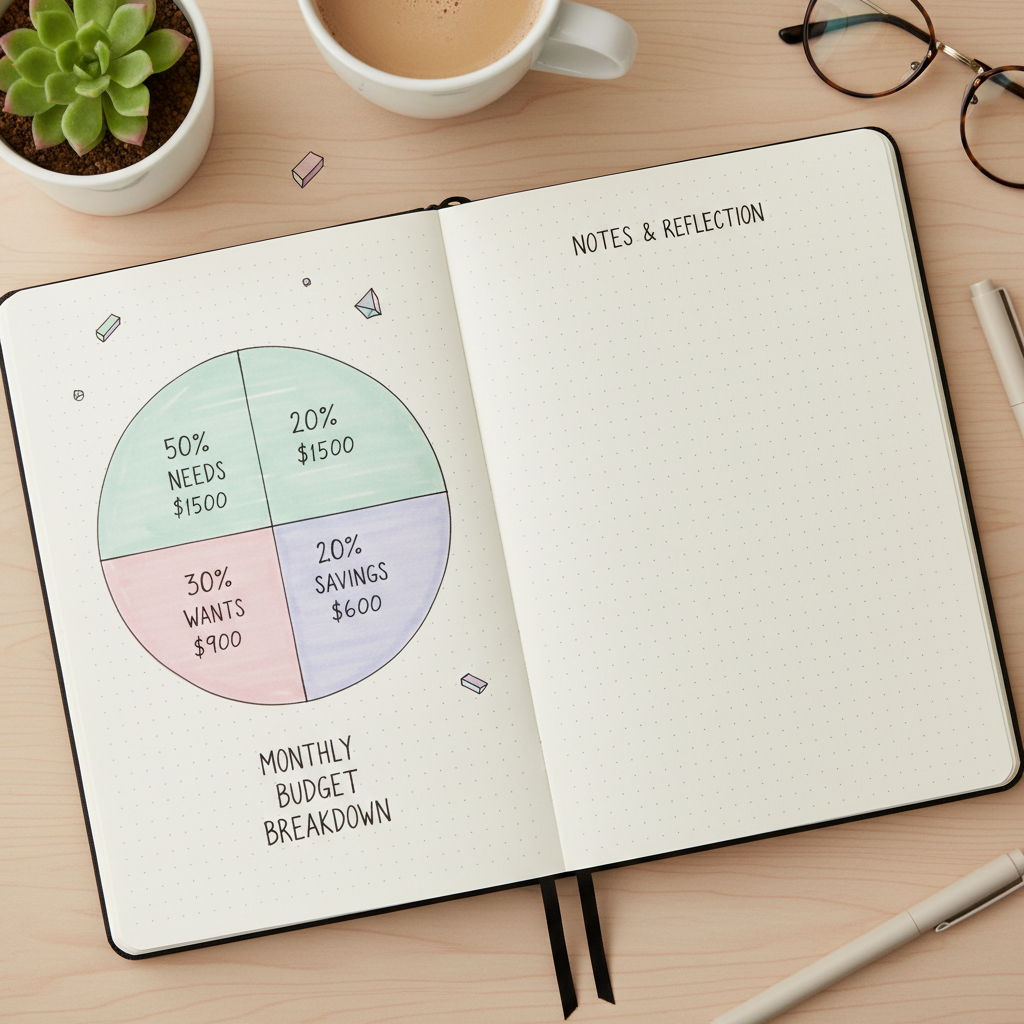

2. The 50/30/20 Pie Chart: Budgeting on Autopilot

The Hack

Once you know where your money is going, it’s time to give it a job. The 50/30/20 rule is a classic for a reason: it’s simple and it works. This spread turns that rule into a visual guide for your spending. The breakdown is easy: 50% of your after-tax income goes to Needs, 30% to Wants, and 20% to Savings & Debt Repayment.

How to Set It Up

Draw a big circle on a page and divide it up. Or use a bar graph if that’s more your style. Label the sections. Then, do the math. Calculate your total monthly take-home pay and figure out the dollar amount for each category. Write those numbers big and bold on the page. This is your monthly blueprint.

The Math Example

Let’s say your monthly take-home pay is $3,500. Here’s your mission:

- Needs (50%): $1,750 for rent/mortgage, utilities, groceries, transportation.

- Wants (30%): $1,050 for dining out, hobbies, entertainment, shopping.

- Savings & Debt (20%): $700 to crush your credit card debt, build an emergency fund, or invest.

Seeing it visually stops you from ‘borrowing’ from your savings goal to pay for another concert ticket. The boundaries are clear.

3. The No-Spend Challenge Tracker: Hit the Financial Reset Button

The Hack

Feeling like your spending is out of control? A No-Spend Challenge is a powerful reset. The goal isn’t to spend zero dollars; it’s to stop all non-essential spending for a set period—a week, a weekend, or a full month. This spread keeps you honest and motivated by making it a game.

How to Set It Up

Draw a calendar grid for the month. Define your rules upfront. For example: ‘No spending on takeout, coffee shops, clothes, or Amazon.’ Each day you succeed, you get to color in the box. Watching that chain of colored boxes grow is a massive psychological boost.

The Savings Math

This is where you see instant results. Let’s say you typically buy a $6 latte on your way to work and grab a $15 lunch. By participating in a no-spend challenge for just the 21 workdays in a month, you’ve saved: ($6 + $15) x 21 = $441. That’s real money you just found in your budget, all by breaking a couple of habits.

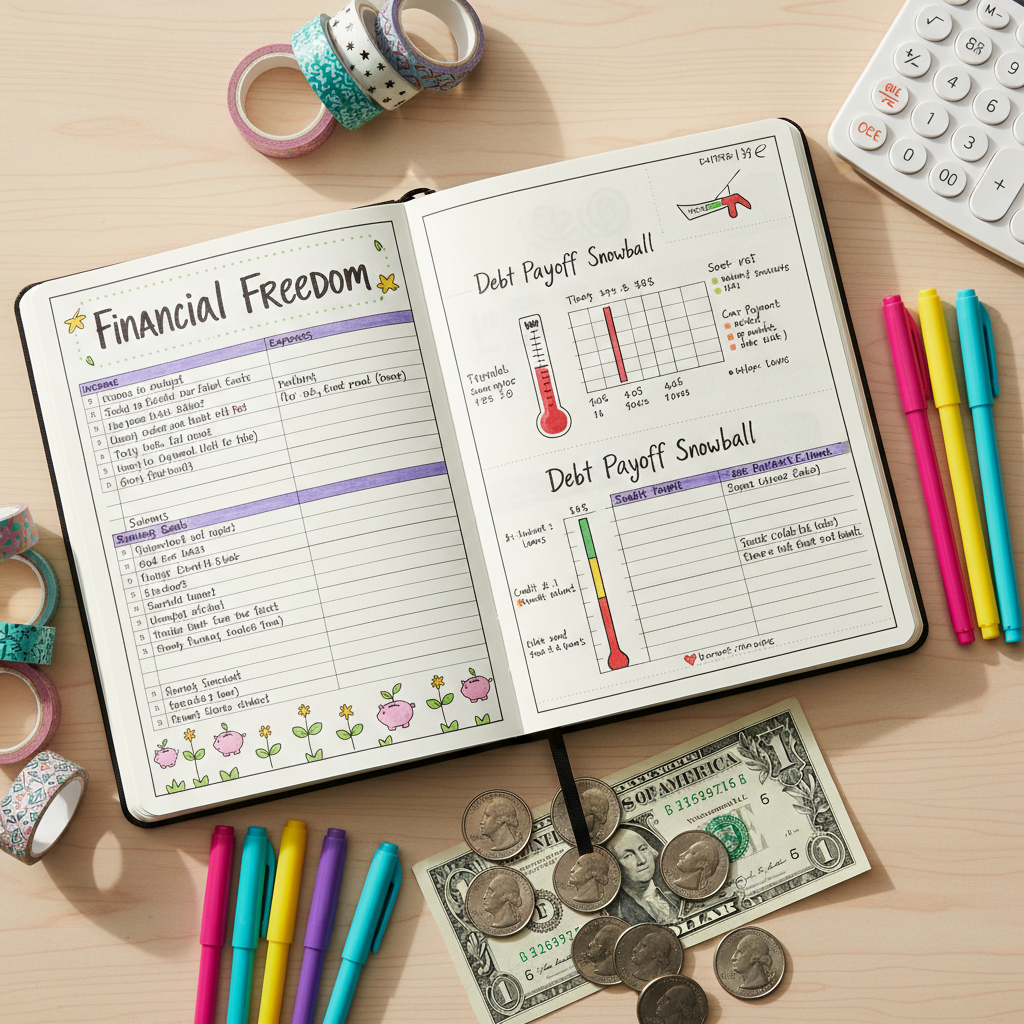

4. The Debt Thermometer: Visually Annihilate Your Debt

The Hack

A credit card statement is just a list of numbers. It’s cold, impersonal, and easy to ignore. A Debt Thermometer turns that abstract number into a monster you can visually conquer. It transforms debt repayment from a chore into a quest.

How to Set It Up

Draw a large thermometer for each major debt you have (e.g., one for your car loan, one for a credit card). At the top, write the total amount owed. Along the side, create milestones (e.g., every $500 or $1,000). Every time you make a payment, you get to color in the thermometer up to the new balance. It’s incredibly satisfying.

The Street-Smart Angle

When you’re slogging through debt repayment, it can feel like you’re getting nowhere. This visual proof of progress is a powerful motivator. It keeps you in the fight on days when you’d rather just give up and order a pizza. It shows you that your sacrifices are paying off, one colored-in stripe at a time.

5. The Savings Goals Jar: From Dream to Reality

The Hack

Saving money for a vague future is hard. Saving money for a specific, awesome thing you really want is way easier. This spread takes your abstract savings goals and makes them tangible, visual, and exciting.

How to Set It Up

Dedicate a page to your ‘Savings Goals.’ Draw a big empty jar (or a treasure chest, a piggy bank, whatever) for each goal. Label them clearly: ‘Emergency Fund ($1,000),’ ‘Vegas Trip ($800),’ ‘New Laptop ($1,500).’ Just like the debt thermometer, create increments along the side. As you transfer money into your savings account for that goal, you color in the jar. You’re literally watching your dreams fill up.

The Street-Smart Angle

This spread changes your mindset from ‘I can’t spend this money’ to ‘I’m choosing to spend this money on my future self.’ It helps you say no to a $60 impulse buy because you can physically see that it’s taking money out of your Vegas jar. It connects today’s discipline with tomorrow’s reward.

6. The Sinking Funds Grid: Stop Surprise Expenses for Good

The Hack

Ever had your budget completely wrecked by an annual insurance premium, holiday gifts, or a sudden car repair? Those aren’t emergencies; they’re predictable but irregular expenses. Sinking funds are your secret weapon against them. You save a small amount each month so the cash is waiting when the bill arrives.

How to Set It Up

Create a grid. Down the left side, list your sinking fund categories: Car Maintenance, Gifts, Annual Subscriptions, Vet Bills, etc. Across the top, list the months. In each box, you’ll write the amount you’re setting aside for that fund that month. For example, if you know you spend about $600 on holiday gifts, you’d save $50 a month all year. No more December panic.

| Fund Category | Monthly Goal | Annual Goal |

|---|---|---|

| Holiday Gifts | $50 | $600 |

| Car Maintenance | $75 | $900 |

| Annual Subscriptions | $20 | $240 |

The Street-Smart Angle

This is next-level adulting. It turns you from a reactive spender into a proactive financial planner. You’re treating your future self with respect by anticipating their needs. This single spread can eliminate a huge source of financial stress and stop the cycle of putting surprise expenses on a credit card.

7. The Subscription Audit: Slay the Silent Budget Killers

The Hack

In the age of ‘free trials’ that automatically convert to paid plans, we’re all leaking money through subscriptions we forgot we even had. This spread is a quick and dirty audit to find and plug those leaks. It’s one of the fastest ways to free up cash in your budget.

How to Set It Up

Create a simple three-column list. Column 1: ‘Subscription Name.’ Column 2: ‘Monthly Cost.’ Column 3: ‘Keep or Cancel?’ Go through your bank and credit card statements with a fine-tooth comb and list every single recurring charge. Then, be ruthless. Do you really need three different TV streaming services? Are you using that premium app? If the answer is no, circle ‘Cancel’ and take action immediately.

The Savings Math

It adds up faster than you think. Canceling one $15.99 streaming service, a $9.99 music app you don’t use, and a $25 subscription box saves you $50.98 per month. Over a year, that’s over $611 back in your pocket for doing almost nothing.

8. The Bill Tracker Matrix: Never Pay a Late Fee Again

The Hack

Late fees are just dumb taxes you pay for being disorganized. A simple bill tracker ensures you never give your money away for free again. It provides a single, at-a-glance view of what’s due, when it’s due, and whether you’ve paid it.

How to Set It Up

Another grid, because they work. List all your recurring bills down the side (Rent, Electric, Internet, Phone, Credit Card, etc.). Across the top, write the months of the year. When a bill is paid for that month, you put a big, satisfying checkmark or X in the box. You can see instantly if something has been missed.

The Street-Smart Angle

This isn’t just about avoiding the $25 late fee. Consistently paying your bills on time is one of the biggest factors in your credit score. A higher credit score saves you thousands of dollars over your lifetime in lower interest rates on loans and mortgages. This simple page is a long-term wealth-building tool in disguise.

9. The ‘Future You’ Goals Page: Your Financial North Star

The Hack

Budgeting without a ‘why’ is just deprivation. You need a North Star. This spread is where you dream big and connect your daily financial habits to your long-term life goals. It’s the motivation that will carry you through the tough months.

How to Set It Up

This is a freeform page. Use beautiful lettering, doodles, or keep it simple. Create sections for your ‘1-Year,’ ‘5-Year,’ and ’10-Year’ financial goals. Be specific. Don’t just write ‘be rich.’ Write ‘Have a $10,000 emergency fund in one year.’ ‘Save $50,000 for a house down payment in five years.’ ‘Max out my retirement accounts in 10 years.’ Make the goals real and measurable.

The Street-Smart Angle

When you’re tempted to blow your budget, you flip to this page. It reminds you that you’re not just ‘saving money’—you’re building a life. You’re choosing your 5-year goal over a short-term impulse. This page is your contract with your future self. Don’t break it.

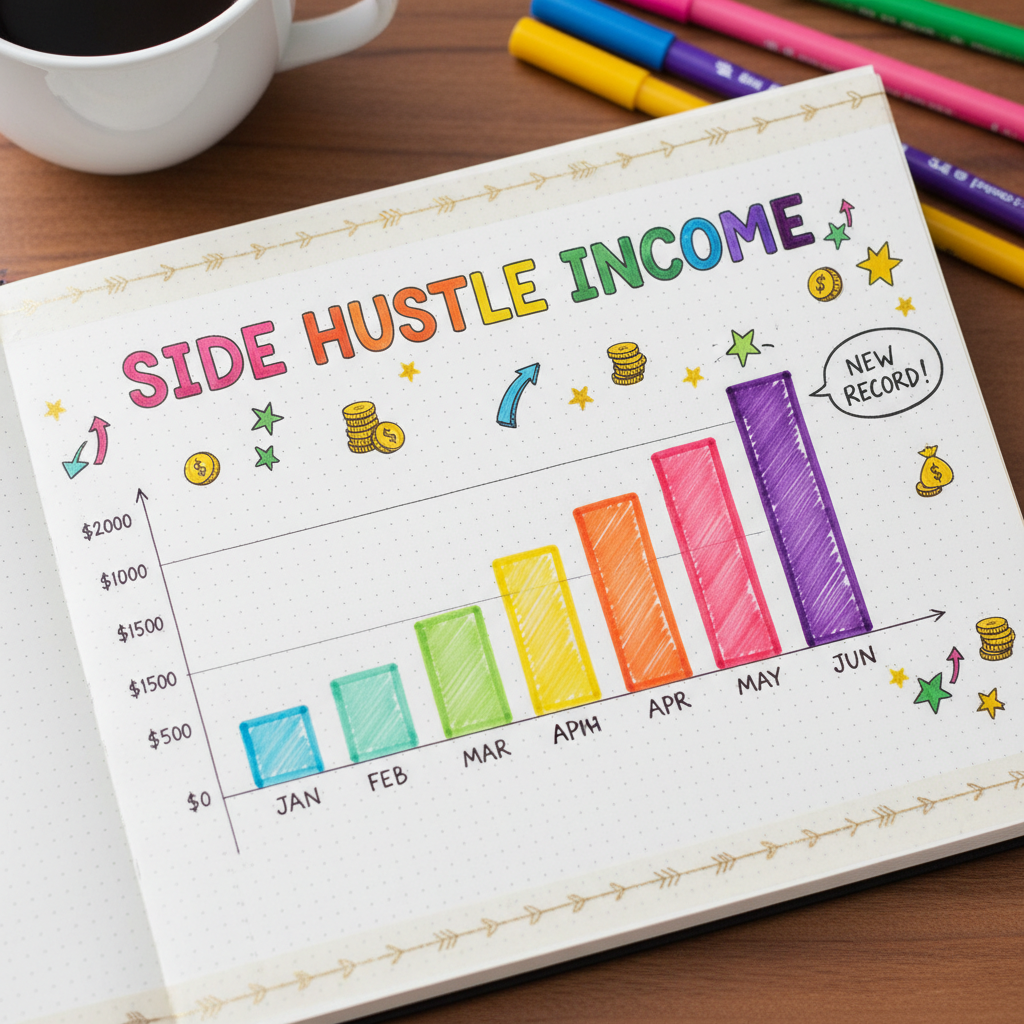

10. The Side Hustle Tracker: Watch Your Extra Income Grow

The Hack

For side hustlers, income can be variable and hard to track. This spread gives you a dedicated space to monitor your earnings from all your different gigs. It gamifies your hustle and shows you which income streams are the most lucrative, helping you decide where to focus your energy.

How to Set It Up

A simple bar graph is perfect for this. Set up the X-axis with the months and the Y-axis with dollar amounts. Each month, draw a bar representing your total side hustle income. You can even color-code the bar to show how much came from each hustle (e.g., green for freelance writing, blue for DoorDash, yellow for Etsy sales). It’s a powerful visual of your growing empire.

The Street-Smart Angle

Seeing that bar chart climb month after month is the ultimate motivation. It proves your hard work is paying off and pushes you to see how high you can get it. It also provides a clear record of your income, which is crucial when it comes time to deal with taxes for your self-employment income.

11. The ‘Wish Farm’: Mindful Spending on Your Wants

The Hack

Impulse buying is a budget’s worst enemy. The Wish Farm is a system to delay gratification and separate a fleeting want from a genuine desire. It forces you to pause before you purchase, saving you from countless regrettable buys.

How to Set It Up

Get creative! Draw a page that looks like a garden or farm. When you want to buy a non-essential item over a certain amount (say, $50), you don’t buy it. Instead, you ‘plant’ it in your Wish Farm. Draw a little sprout and label it with the item and the date. Then, you have to wait. Set a rule for yourself, like 30 days.

The 30-Day Rule: If you want it, write it down. Wait 30 days. If you still want it, and can afford it, then you can give yourself permission to buy it.

You’ll be shocked at how many ‘seeds’ you plant that you no longer care about a month later.

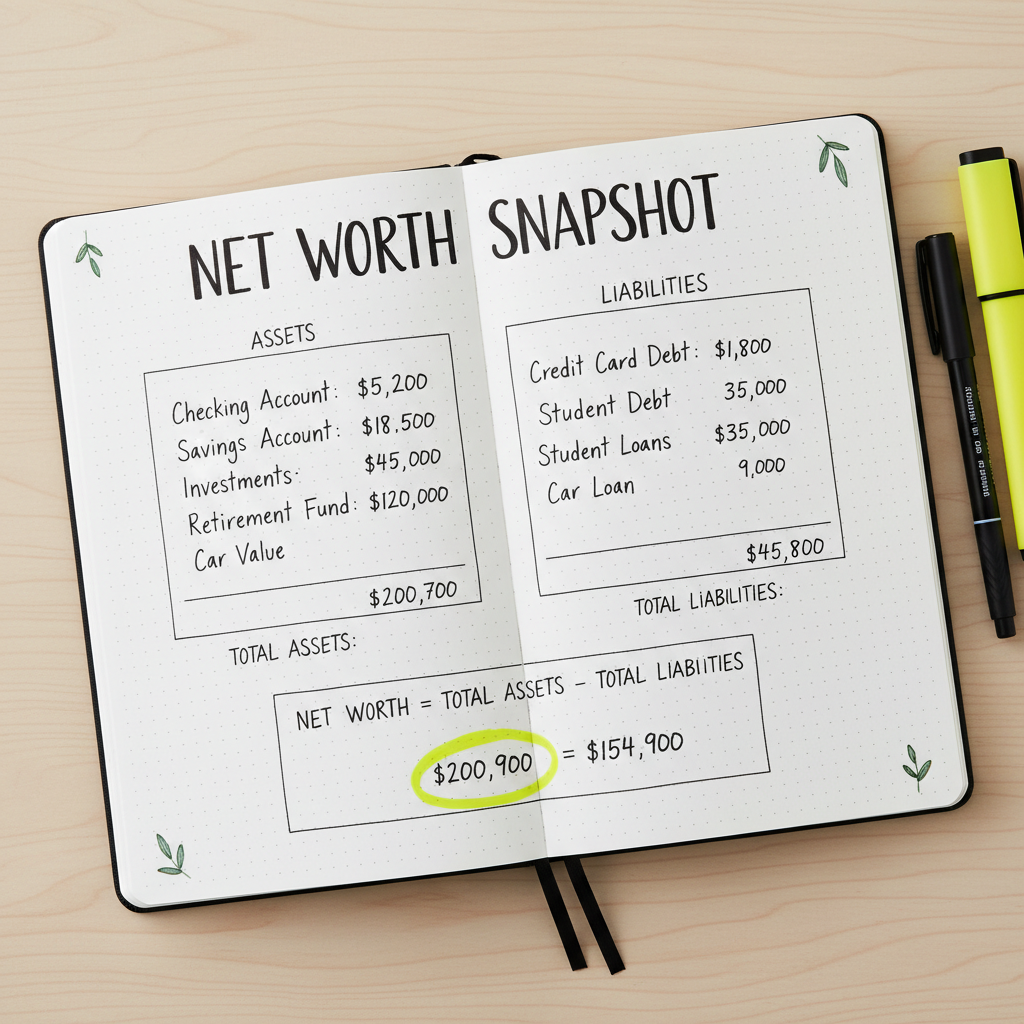

12. The Net Worth Dashboard: The Ultimate Financial Scoreboard

The Hack

Income is how much you make. Net worth is how much you own. This is the ultimate measure of your financial health. Tracking it, even just once a quarter, gives you the 30,000-foot view of your progress. It’s the final score of your financial game.

How to Set It Up

This is a simple but powerful spread. It’s best formatted as a table to keep things clean. You have two main categories: Assets (what you own that has value) and Liabilities (what you owe). Your net worth is your Assets minus your Liabilities.

| Net Worth Snapshot: Q3 | |

|---|---|

| ASSETS (What you own) | |

| Checking/Savings Account | $5,000 |

| Retirement Account (401k) | $15,000 |

| Car Value (KBB) | $8,000 |

| TOTAL ASSETS | $28,000 |

| LIABILITIES (What you owe) | |

| Student Loan | $12,000 |

| Credit Card Debt | $2,000 |

| TOTAL LIABILITIES | $14,000 |

| FINAL NET WORTH | $14,000 |

The Street-Smart Angle

Focusing on net worth shifts your perspective from just saving money to actively building wealth. You’ll start to see how paying down debt is just as powerful as increasing your savings because both actions increase your net worth. This is the spread that shows you’re not just surviving; you’re winning.

Conclusion

There you have it—12 no-nonsense, powerful spreads to turn a simple notebook into a money-making, debt-crushing machine. The beauty of the bullet journal is its flexibility. You don’t need to be an artist, and you don’t need expensive supplies. All you need is a pen, a notebook, and the will to take back control.

Start small. Pick just one of these spreads—the Monthly Log or the Subscription Audit are great places to start—and commit to it for one month. Don’t aim for perfection; aim for progress. A budget isn’t a cage; it’s the key to your financial freedom. It’s the tool that lets you tell your money what to do so you can build the life you actually want. Now stop reading, and start doing. Your future self will thank you for it.