The “Cushion Method”: How To Never Overdraft Your Account Again

Let’s be real. That sinking feeling when you check your bank account and see a negative balance followed by a $35 fee is one of the worst. It’s a gut punch. It feels like you’re being punished for being broke. You work hard, you hustle, you try to make every dollar count, and yet one tiny miscalculation, one unexpected bill, and BAM—you’re paying the bank for the privilege of not having enough money. It’s a rigged game.

But what if you could opt out of that game for good? What if there was a simple, no-fluff method to make overdrafts a thing of the past, without needing complicated spreadsheets or a finance degree? That’s where the Cushion Method comes in. This isn’t your typical boring budget advice. This is a street-smart financial hack that puts a permanent buffer between you and that dreaded zero balance. It’s about changing your mindset, taking back control, and keeping your money where it belongs: in your pocket. Get ready to build your financial fortress, one dollar at a time.

What The Heck is the “Cushion Method” (And Why You Need It)?

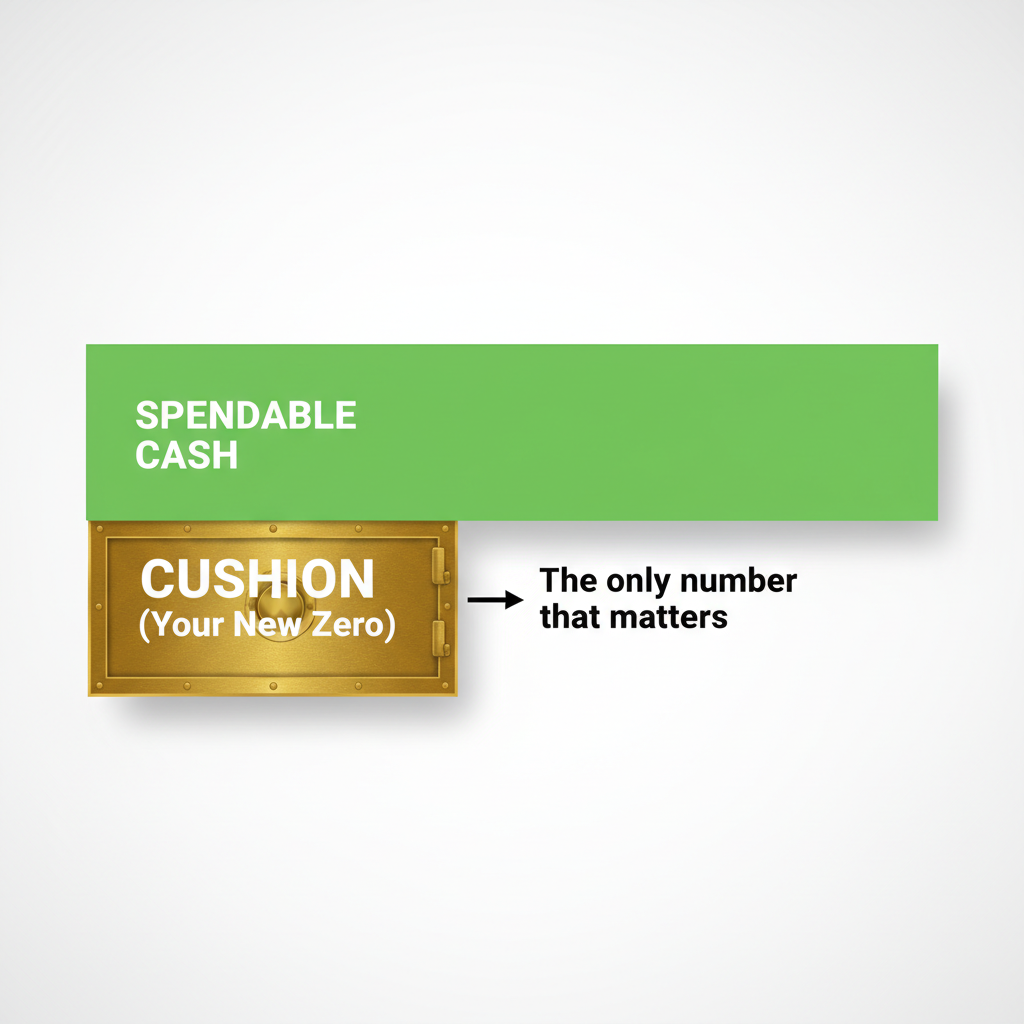

Forget everything you think you know about complicated budgeting. The Cushion Method is brutally simple: You decide on a set amount of money in your checking account that you will never, ever touch. This is your cushion. This money just lives there, acting as a permanent buffer. Your new ‘zero’ is not actually $0; it’s the top of your cushion.

For example, if you decide your cushion is $200, you mentally (and practically) treat $200 as your absolute floor. When you look at your bank balance and it says $250, your brain shouldn’t see $250. It should see $50 of spendable cash. That’s it. The other $200 might as well be invisible.

Why is this a game-changer? Because it kills the paycheck-to-paycheck-down-to-the-last-cent mindset. Most people see $15 in their account and think, ‘Great, I can afford that $12 lunch.’ With the Cushion Method, if your cushion is $100 and your balance is $15, you’re already $85 in the hole mentally. You’re not buying that lunch. You’re figuring out your next move. It’s a psychological tripwire that goes off *before* you hit zero, not after the bank has already charged you a fee.

This isn’t an emergency fund for a car repair or a medical bill. That’s a separate pile of cash you should be building. The cushion is purely an operational buffer for your daily cash flow. It’s there to absorb small timing mistakes, like a bill coming out a day before your paycheck hits, or a subscription you forgot about. It’s the shock absorber for your financial life.

The Real Cost of “Oops”: Breaking Down Overdraft Fees

Banks love to market ‘overdraft protection’ as a favor, but let’s call it what it is: one of the most expensive short-term loans on the planet. They’re charging you a premium, often $35 a pop, for their system to approve a $5 coffee purchase that you didn’t have the funds for. It’s a cycle designed to keep you down. The numbers are staggering when you actually do the math.

You might think, ‘It’s just one fee every now and then.’ But ‘now and then’ adds up to a serious amount of your hard-earned money being thrown away. Money that could have been used to pay down debt, invest in a side hustle, or just give you some breathing room. Let’s look at the cold, hard cash you’re handing over.

The Overdraft Trap: How Much Are You Really Losing?

| Number of Overdrafts Per Month | Average Fee | Total Lost Per Month | Total Lost Per Year |

|---|---|---|---|

| 1 Overdraft | $35 | $35 | $420 |

| 2 Overdrafts | $35 | $70 | $840 |

| 3 Overdrafts | $35 | $105 | $1,260 |

| 4 Overdrafts | $35 | $140 | $1,680 |

Look at that table. Just two accidental overdrafts a month costs you nearly a grand a year. Four a month? You’re losing almost $1,700. That’s a vacation. That’s a new laptop for your side hustle. That’s a significant chunk of debt paid off. The Cushion Method is your ticket out of this trap. By investing just a few hundred dollars *once* to create your buffer, you save yourself thousands in the long run. It’s the ultimate no-brainer investment in your own financial stability.

The Step-by-Step Playbook: Setting Up Your Cushion

Alright, enough talk. It’s time to take action. Setting up your cushion isn’t complicated, but it requires discipline, especially at the start. Follow this playbook to build your financial firewall and make it stick.

-

Step 1: Pick Your Number

Your cushion amount is personal. The goal is to pick a number that’s big enough to cover common timing gaps but not so big that it feels impossible to save up. A great starting point for most people is between $100 and $300. If you frequently have large auto-payments, you might aim for $500. The key is to just start. Don’t get paralyzed by picking the ‘perfect’ number. A $50 cushion is infinitely better than no cushion at all. You can always grow it later.

-

Step 2: Fund The Cushion

Where does this magic money come from? You have to find it. This is a one-time hustle to secure your financial future. Consider these options:

- Sell something: That old video game console, clothes you don’t wear, furniture collecting dust. List it on Facebook Marketplace or OfferUp and dedicate that cash directly to your cushion.

- Pick up a one-off gig: Drive for Uber for a weekend, do a few food delivery shifts, find a quick gig on TaskRabbit.

- The ‘No-Spend’ Challenge: For one or two weeks, commit to not spending a single dollar on non-essentials. No coffee, no eating out, no impulse buys. Transfer what you save into your cushion fund.

- Use your tax refund: If you get a refund, peel off a few hundred dollars to fund your cushion before you do anything else with it.

-

Step 3: The Mental Shift (This is the most important part)

Once the money is in your account, the real work begins. You must fundamentally change how you view your bank balance. Write it down, put a sticky note on your monitor, set a reminder on your phone: My new zero is [Your Cushion Amount]. If your cushion is $200, you must train your brain to subtract $200 from whatever balance you see. A balance of $201 means you have exactly $1 to spend. A balance of $199 means you are broke and need to stop spending immediately. This mental accounting is the core of the entire method.

-

Step 4: Track It and Respect It

In the beginning, you’ll need to be vigilant. Use a simple tool to help. A budgeting app like YNAB is perfect for this, as you can literally put your cushion money into a category and not touch it. If you don’t use an app, a simple note on your phone will do. Every time you check your balance, do the quick math: [Actual Balance] – [Cushion Amount] = [Your Real, Spendable Balance].

Automate It & Forget It: Making Your Cushion Bulletproof

The human brain is lazy. We forget things, we get tempted, and we make mistakes. The key to making the Cushion Method work long-term is to build a system around it that requires as little willpower as possible. You want to make it easy to succeed and hard to fail. Here’s how you make your cushion bulletproof.

Use Technology to Your Advantage

Your banking and budgeting apps are your best friends here. Let them do the heavy lifting:

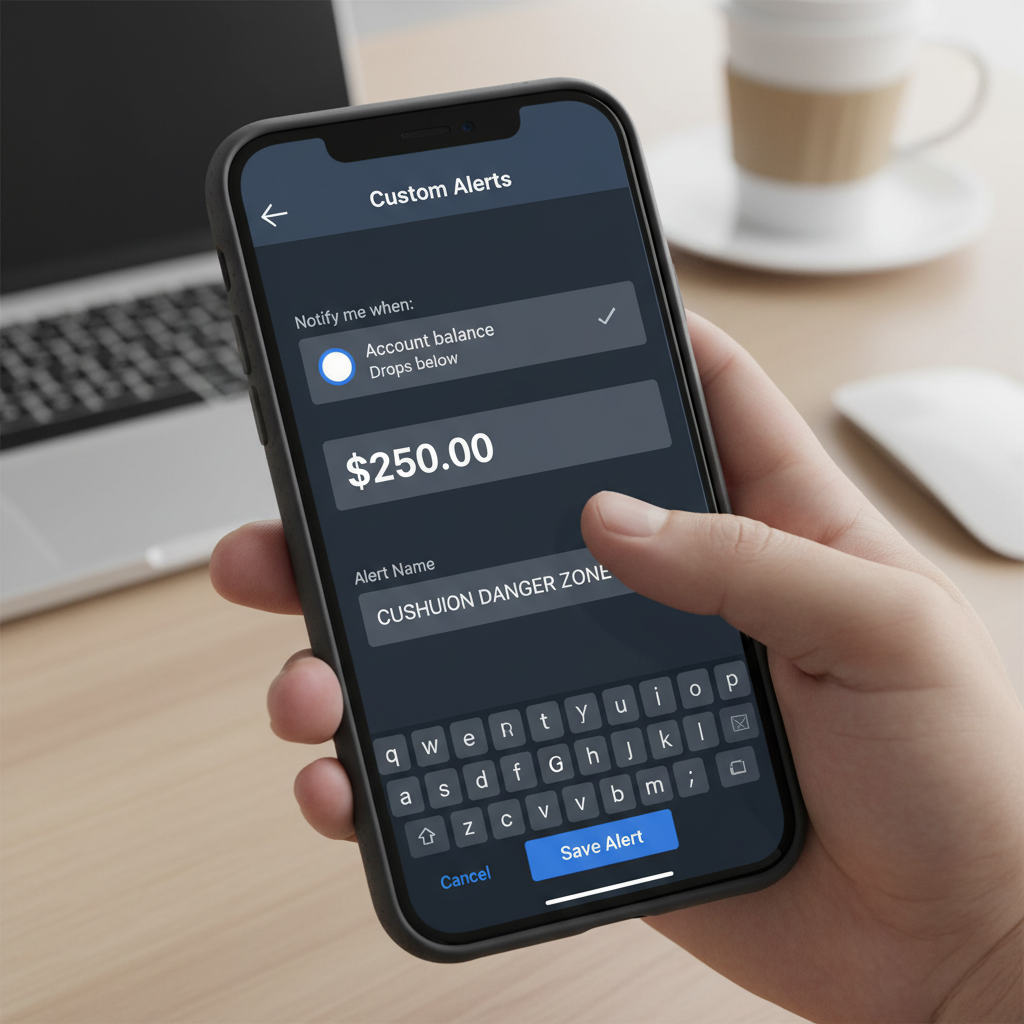

- Set Up Smart Low-Balance Alerts: Don’t set your bank’s low-balance alert to $25. That’s too late; the damage might already be done. Set your alert for your cushion amount plus a small buffer. If your cushion is $200, set your low-balance alert for $250. This way, your phone pings you *before* you enter the danger zone, giving you time to adjust your spending.

- Leverage Budgeting Apps: Apps like YNAB (You Need A Budget), EveryDollar, or even a detailed spreadsheet force you to give every dollar a job. Create a category called “Checking Account Cushion” and assign your chosen amount to it. Once it’s in that category, it’s mentally off-limits. The app’s math will be based on your remaining, available funds, automatically doing the mental calculation for you.

- Automate a ‘Top-Up’ Transfer: Let’s say you had a real emergency and had to dip into your cushion. Don’t just leave it half-full. Set up an automatic transfer from your savings or your next paycheck to immediately replenish it. For example, if you used $50 from your $200 cushion, set up a $50 transfer to get it back to full strength as soon as you get paid.

The “Two Account” Method vs. The Cushion Method

Some people link a savings account to their checking for ‘overdraft protection’. The bank will automatically pull money from your savings to cover a shortfall. While this avoids the $35 fee, it can be a crutch. It masks the underlying issue: you’re spending money you don’t have. It silently fixes the problem without forcing you to change your behavior. The Cushion Method is more powerful because it’s a behavioral tool. The pain of seeing your ‘spendable’ balance hit zero forces you to be more mindful of your cash flow. It trains you to be a better money manager, which is a skill that pays dividends for life.

Common Pitfalls & How to Dodge Them

Implementing the Cushion Method is a huge step, but the journey isn’t always smooth. You’re fighting years of old habits. Knowing the common traps ahead of time is the best way to avoid falling into them. Here’s what to watch out for.

- Pitfall #1: The Temptation to ‘Borrow’ from the Cushion. You’ll see that money sitting there and think, ‘I’ll just borrow $40 for this weekend and pay it back on Monday.’ This is a slippery slope that defeats the entire purpose. You have to treat the cushion like it’s not your money. It belongs to the ‘Bank of My Future Self,’ and the penalty for unauthorized withdrawals is stress and overdraft fees.

- Pitfall #2: Forgetting to Do the Math. In a rush, you might glance at your total balance and make a spending decision based on that number. This is how mistakes happen. In the first few months, be religious about doing the mental subtraction. Every. Single. Time. It needs to become an automatic reflex.

- Pitfall #3: Setting It and Forgetting It (The Wrong Way). Your financial life changes. You might get a raise, or your rent might go up. A $200 cushion that worked perfectly a year ago might be too small for your current expenses. Re-evaluate your cushion amount once a year to make sure it’s still providing the safety you need.

- Pitfall #4: Confusing It with an Emergency Fund. A true emergency (your car’s transmission dies, you have an unexpected medical bill) is what your separate emergency fund is for. The cushion is for cash flow timing, not life-altering events.

The Golden Rule: Your cushion is not an emergency fund. It’s not a ‘maybe’ fund. It is the new zero-dollar line. It is the floor. You don’t touch the floor. Period.

Conclusion

Let’s cut to the chase. The Cushion Method isn’t just about avoiding fees; it’s about ending financial anxiety. It’s about getting off the defensive and starting to play offense with your money. For the cost of a few pizzas or a new pair of sneakers, you can buy yourself permanent peace of mind. You can stop giving away your power—and your cash—to big banks and start building a foundation of control and confidence.

Your challenge is simple: Start today. Right now. Figure out your number, even if it’s just $20. Find that money in your budget, sell something, do whatever it takes to establish your buffer. This is one of the highest-impact financial moves you can make, and the only thing it costs you is the decision to start. Stop letting your bank account control you. It’s time to show your money who’s boss.