7 Money Skills Every Teen Needs Before Turning 18

Listen up. Most of the money ‘advice’ you hear is garbage. It’s either coming from your parents who still think a passbook is a good idea, or from a stuffy school textbook written before the internet existed. The real world doesn’t care about your algebra homework; it cares if you can read a pay stub, build a credit score, and not get scammed by a bank’s hidden fees. Getting thrown into adulthood without these skills is like being dropped into a boss-level video game with no tutorial. You’re set up to fail.

This isn’t another boring lecture. This is your cheat sheet. Your backstage pass to financial adulthood. We’re talking about seven non-negotiable money skills that will put you a decade ahead of your peers. Mastering these before you turn 18 isn’t just about saving a few bucks; it’s about seizing control, building real wealth, and designing a life on your own terms. Let’s get to it.

Skill #1: Master the 50/30/20 Budget—Your Financial Blueprint

A budget isn’t a financial prison; it’s your blueprint for freedom. It’s you telling your money where to go instead of wondering where it went. Forget complicated spreadsheets. The simplest and most powerful system is the 50/30/20 rule. It’s a game-changer because it’s flexible and realistic.

Here’s the breakdown:

- 50% for Needs: This is the stuff you absolutely have to pay for. For a teen, this might be your phone bill, gas for the car, or contributing to car insurance. It’s the boring but necessary stuff.

- 30% for Wants: This is the fun money. Video games, new sneakers, concert tickets, going out with friends. This is the part of the budget that makes life worth living. No guilt allowed.

- 20% for Savings & Future Goals: This is the most important slice. This is where you pay your future self. It’s for big goals like a car, college, or even your first investment. This 20% is your ticket to wealth.

The magic is in automating it. Use an app like Mint, YNAB (You Need A Budget), or even the features in your bank’s app. Link your account, and it’ll track your spending for you. All you have to do is check in and make sure you’re sticking to the plan.

The Math: How It Actually Works

Let’s say you’re working a part-time job and bringing home $800 a month. Here’s how the 50/30/20 rule would look in action:

| Category | Percentage | Monthly Amount | What it Covers |

|---|---|---|---|

| Needs | 50% | $400 | Phone bill, gas, car insurance payment |

| Wants | 30% | $240 | Gaming, clothes, food with friends, hobbies |

| Savings | 20% | $160 | Building an emergency fund, saving for a car, first investment |

That $160 a month doesn’t seem like a lot, right? Wrong. That’s $1,920 in a single year. That’s a solid used car, a high-end gaming PC, or a serious head start on your college fund. It’s power.

Skill #2: Ditch the Piggy Bank—Get a Real, No-Fee Bank Account

Cash stuffed under your mattress is losing money every single day because of inflation. It’s also easy to lose or spend. It’s time to graduate. Opening your first bank account is a critical rite of passage, but you have to do it right, or you’ll get bled dry by fees.

Checking vs. Savings: Know the Difference

- A Checking Account is your daily driver. It’s for direct deposits from your job and for spending money via a debit card. It’s your financial hub.

- A Savings Account is your wealth-building zone. This is where your ‘20%’ from the budget goes. You don’t touch this money unless it’s for a planned goal or a true emergency. Look for a High-Yield Savings Account (HYSA) online—they pay you more in interest just for letting your money sit there.

Your mission is to find an account with ZERO monthly maintenance fees and ZERO minimum balance requirements. Big traditional banks are notorious for hitting you with fees. Look at local credit unions or online banks like Ally or Capital One 360, which often have student accounts designed specifically for you.

Scam Warning: Phishing Scams

You will get emails and texts that look like they’re from your bank, saying your account is locked or there’s a problem. They’ll ask you to click a link and log in. NEVER click that link. This is a phishing scam to steal your login info. Your bank will never ask for your password via email or text. If you’re worried, close the message and log into your account directly through the official app or website.

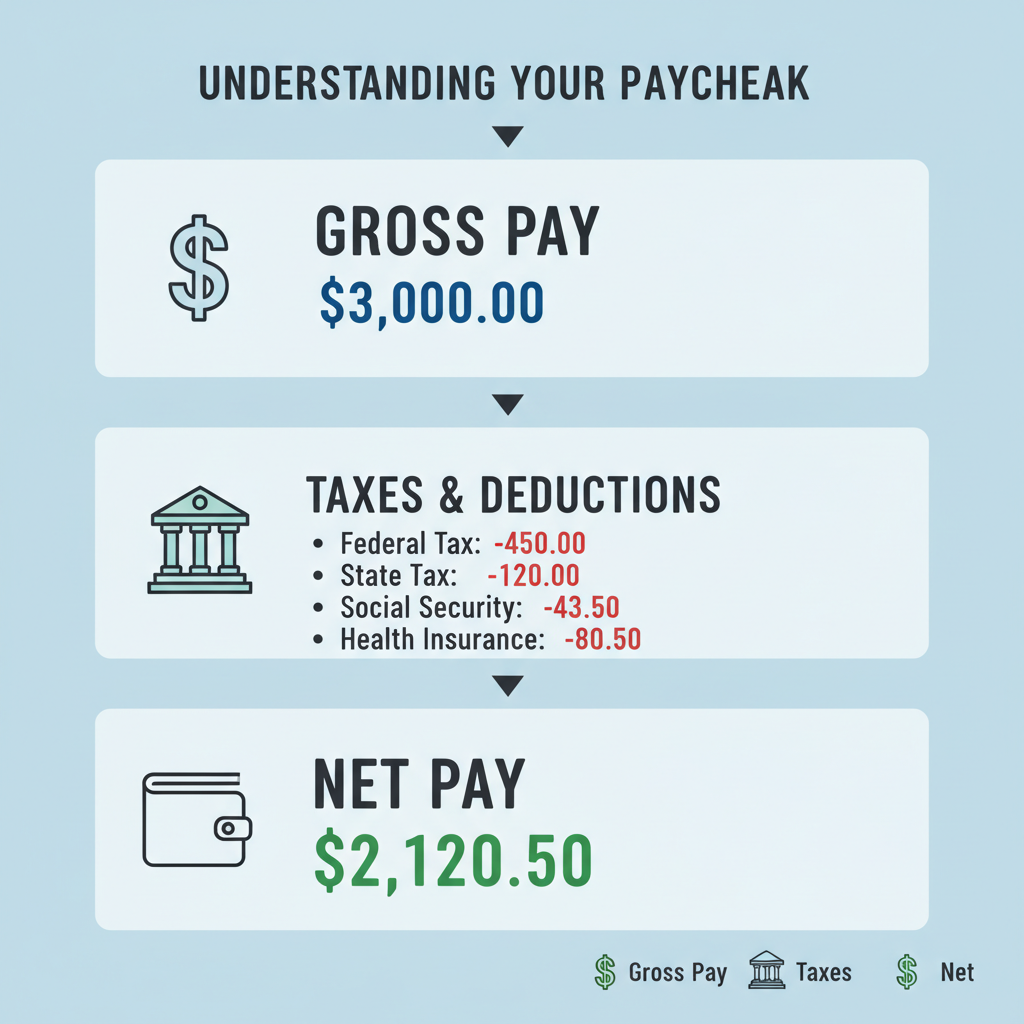

Skill #3: Decode Your Paycheck—Where Your Money Really Goes

Getting your first paycheck is awesome. Seeing how much smaller it is than you expected… not so much. Understanding why is a crucial skill. You need to know how to read a pay stub so you know you’re being paid correctly and understand where your hard-earned cash is going.

The Key Terms You Must Know:

- Gross Pay: This is the big number. It’s your hourly wage multiplied by the hours you worked before any deductions. It’s the fantasy number.

- Deductions: This is everything taken out of your gross pay. The big ones are taxes.

- Net Pay (Take-Home Pay): This is the reality. It’s the actual amount deposited into your bank account after all deductions. This is the number you use for your budget.

The main deductions you’ll see are taxes. FICA (Federal Insurance Contributions Act) pays for Social Security and Medicare. Then you have federal and state income taxes. It can feel like a rip-off, but it’s the law. The key is to know what to expect so you’re not shocked when your $400 paycheck turns into $330.

Sample Pay Stub Breakdown

Let’s say you worked 25 hours at $16/hour.

| Description | Amount | Notes |

|---|---|---|

| Gross Pay | $400.00 | 25 hours x $16/hour |

| Federal Income Tax | ($25.00) | Estimate for a single filer |

| State Income Tax | ($15.00) | Varies by state |

| FICA (Social Security & Medicare) | ($30.60) | 7.65% of your Gross Pay |

| Net Pay (Take-Home) | $329.40 | This is what hits your bank! |

Always check your pay stub. Mistakes happen. Make sure your hours and pay rate are correct. If something looks wrong, speak up immediately.

Skill #4: Build Your Own Income—The Side Hustle Grind

A job is where you trade your time for money. A side hustle is where you build something for yourself. It’s about creating your own income stream, learning valuable skills, and gaining a level of independence your peers won’t have. Forget babysitting or mowing lawns—we’re talking about real, scalable hustles.

Modern Side Hustles for Teens:

- Sneaker/Vintage Reselling: Got an eye for style? Use apps like Depop, GOAT, or StockX to flip sneakers and clothes. Start by thrifting, learn the market, and scale up.

- Social Media Manager: You already know Instagram, TikTok, and Twitter better than most adults. Local businesses (coffee shops, boutiques, mechanics) will pay you to run their social media accounts. Create a simple portfolio and start pitching.

- Digital Services: Are you good at video editing, graphic design (Canva counts!), or writing? Offer your services on platforms like Fiverr or Upwork. You can build a client base from your bedroom.

- Tutoring: If you excel in a subject like math or science, you can tutor younger kids online. Platforms like Wyzant connect you with students, or you can advertise locally.

The key is to treat it like a real business. Track your income and expenses. A simple Google Sheet is all you need. This will be invaluable when it comes to understanding profit and loss.

Realistic Earning Potential

| Side Hustle | Startup Cost | Realistic Monthly Earnings (Part-Time) |

|---|---|---|

| Social Media Manager (1-2 clients) | $0 | $200 – $500 |

| Sneaker Reselling | $100 – $300 (for initial inventory) | $150 – $600+ (highly variable) |

| Online Tutoring | $0 | $200 – $400 (at $20-25/hour) |

Skill #5: The Credit Game—How to Build an 800 Score from Scratch

This is the most misunderstood and most important skill on this list. Your credit score is a three-digit number that basically acts as your adulting GPA. A good score gets you approved for apartments, gets you better deals on car loans, and can even impact your insurance rates. A bad score is like a ball and chain, making everything more expensive and difficult. Starting to build it before 18 gives you a massive, almost unfair, advantage.

How to Start Building Credit as a Teen:

- Become an Authorized User: Ask a parent or guardian with a great credit history to add you as an authorized user to one of their credit cards. You don’t even need to use the card. Their good payment history will be ‘copied’ to your credit report, giving you an instant foundation.

- Get a Secured Credit Card: Once you’re 18, you can get your own card. A secured card is the best way to start. You make a small security deposit (e.g., $200), and that becomes your credit limit. Use it for one small, recurring purchase each month (like Spotify or Netflix), and pay the bill in full, on time, every single time. After 6-12 months, the bank will see you’re responsible, refund your deposit, and upgrade you to a regular unsecured card.

The Golden Rules of Credit:

- Always Pay On Time: This is 35% of your score. One late payment can wreck your score for years. Set up autopay. No excuses.

- Keep Your Utilization Low: Only use a small fraction of your available credit limit. If your limit is $500, try to keep your balance below $50. This shows lenders you’re not desperate for cash.

Scam Warning: Credit Repair Scams

You’ll see ads promising to ‘fix your credit fast’ or ‘erase bad credit’. These are almost always scams. There is no magic trick. The only way to build good credit is through time and responsible behavior. You can do everything they promise for free by yourself.

Skill #6: Make Your Money Work for You—Investing 101

Saving money is for defense. Investing is for offense. It’s how you truly build wealth. The secret weapon you have as a teen isn’t money—it’s time. Thanks to the magic of compound interest, even small amounts of money invested now can grow into fortunes later.

Compound interest is just interest earning interest. Think of it like a snowball rolling downhill. It starts small, but the longer it rolls, the bigger and faster it gets. Your job is to start the snowball rolling as early as possible.

How to Start Investing (The Simple, Smart Way):

Forget trying to pick hot stocks like GameStop or Tesla. That’s gambling. The smart play is to invest in low-cost index funds. An index fund is like a basket that holds tiny pieces of hundreds or thousands of the biggest companies (like Apple, Amazon, and Microsoft). You get diversification instantly, and you’re betting on the overall growth of the market, which historically goes up over time.

You can start by having a parent help you open a Custodial Account (an UGMA/UTMA account) at a brokerage like Fidelity, Schwab, or Vanguard. You can invest in an S&P 500 index fund (like VOO) or a total stock market index fund (like VTI).

The Math: Why Starting Young is a Superpower

Let’s see the power of time. Assume an average 8% annual return.

- Teen Investor (Starts at 16): Invests $100/month until age 65. Total investment: $58,800. Final portfolio value: $695,000.

- ‘Responsible’ Adult (Starts at 26): Invests the same $100/month until age 65. Total investment: $46,800. Final portfolio value: $305,000.

By starting just 10 years earlier, the Teen Investor ends up with more than double the money, despite investing only $12,000 more. That is the power of compounding. You are trading a little bit of money now for a massive amount of money later.

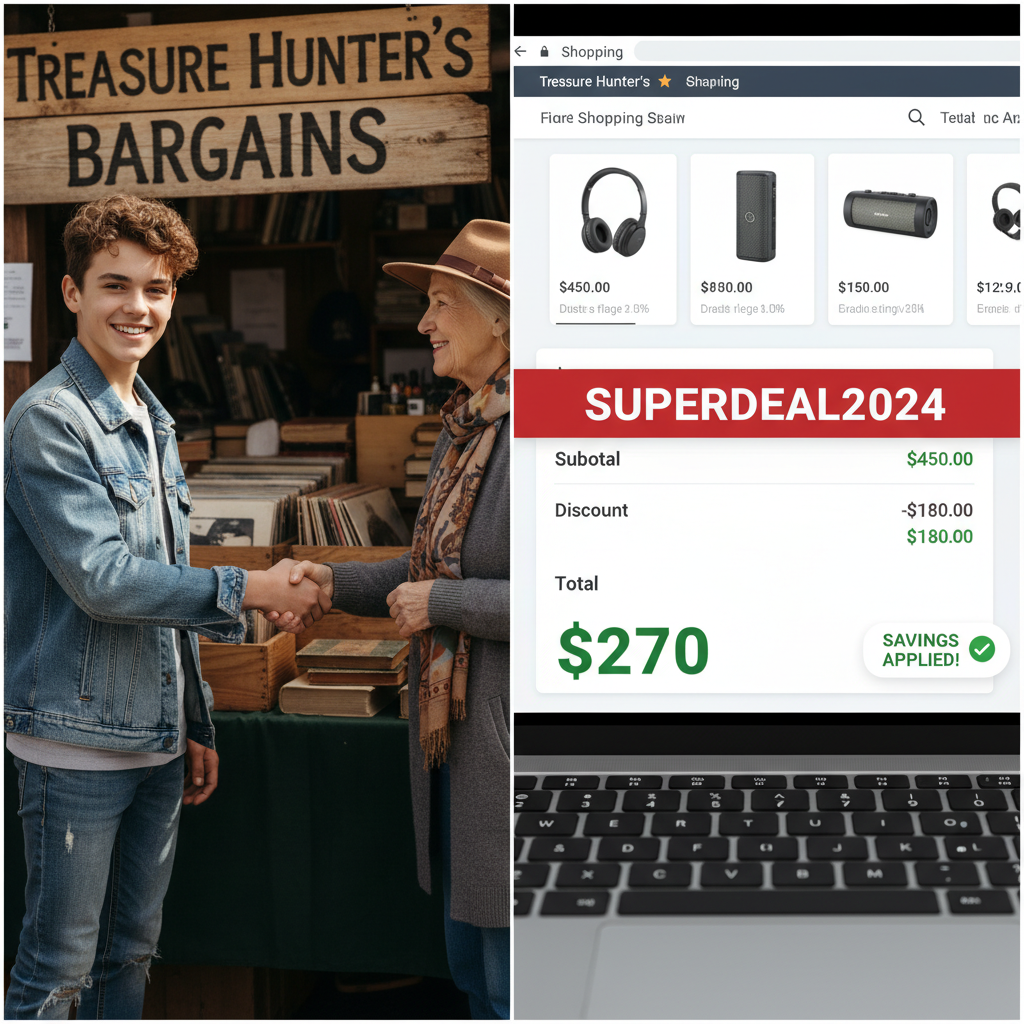

Skill #7: Never Pay Full Price—The Art of Negotiation and Smart Spending

Being good with money isn’t just about earning and saving; it’s about being a savvy consumer. The price tag is often just a suggestion. Learning to negotiate and use spending hacks can save you thousands over your lifetime.

Become a Confident Negotiator

Negotiation isn’t just for car dealerships. You can use it on Facebook Marketplace, at garage sales, or even when discussing your pay rate. The key is to be polite, confident, and prepared.

Sample Negotiation Script (for Facebook Marketplace):

You see a bike listed for $150.

You: “Hi, I’m really interested in the bike. It looks great. Would you be willing to accept $110 cash for it? I can pick it up this afternoon.”

They might say no, but they’ll often come back with a counteroffer like “I can do $130.” Just like that, you saved $20 in 30 seconds.

Master Smart Spending Hacks

- Use Browser Extensions: Install extensions like Honey, Rakuten, or Capital One Shopping. Before you buy anything online, they automatically search for coupon codes and apply them at checkout. Rakuten also gives you cash back on purchases. It’s free money.

- Thrift and Buy Used: For clothes, furniture, and electronics, always check thrift stores and second-hand marketplaces first. You can find high-quality items for a fraction of the price.

- Understand Unit Pricing: At the grocery store, look at the price per ounce/gram on the shelf tag. The bigger box isn’t always the better deal. This small habit saves you a ton on groceries over time.

Being a smart spender means you can have the things you want without derailing your budget. It’s about maximizing the power of every dollar you spend.

Conclusion

There you have it—the seven skills that separate the financially savvy from the perpetually broke. This isn’t just about numbers; it’s about a mindset. It’s about understanding that you are in control of your financial destiny. Mastering budgeting, banking, credit, earning, investing, and smart spending before you’re 18 is like getting a 10-year head start in the game of life.

Don’t get overwhelmed. Start with one. Open that bank account. Track your spending for one week. Make your first offer on Marketplace. Each small action builds momentum. You have the blueprint now. The rest is up to you. Go build your empire.

Disclaimer: The information provided in this article is for educational purposes only and is not intended as financial advice. I am not a financial advisor. You should consult with a licensed financial professional before making any investment decisions.